Downing Renewables and Infrastructure Trust – Targeting attractive and sustainable income returns

IMPORTANT INFORMATION

NB: Marten & Co has been paid to prepare this note on behalf of Downing Renewables and Infrastructure Trust Plc. This is a marketing communication and not a prospectus.

The note is based upon publicly available information and information provided to us by Downing Renewables and Infrastructure Trust Plc and should be read in conjunction with the Downing Renewables and Infrastructure Trust Prospectus published on 12 November 2020. Readers should not place any reliance on the information contained within this note.

The note does not form part of any offer and is not intended to encourage the reader to subscribe for ordinary shares in Downing Renewables and Infrastructure Trust or deal in any other security or securities mentioned within the note.

Marten & Co does not seek to and is not permitted to provide investment advice to individual investors.

The note is not intended to be read and should not be redistributed in whole or in part in the United States of America, its territories and possessions; Canada; Australia; the Republic of South Africa; or Japan.

The details of the share issue, including the risk factors that investors should take into consideration, are more fully described in the prospectus published by Downing Renewables & Infrastructure Trust plc on 12 November 2020 and we urge readers to read this before making any investment decision. The approval of the prospectus by the Financial Conduct Authority should not be understood as an endorsement by the Financial Conduct Authority of the securities offered. If you have any doubts about the suitability of an investment you should seek professional advice.

Targeting attractive and sustainable income returns

Downing Renewables and Infrastructure Trust (DORE) is looking to raise up to £200m to invest in a diversified portfolio of renewable energy and infrastructure assets. The trust is targeting a NAV total return of 6.5% to 7.5% per annum over the medium to long term.

The intention is to pay dividends quarterly, targeting a dividend of 3p (3% of the 100p per share initial issue price) for the calendar year ended 31 December 2021, rising to 5p for 2022 and adopting a progressive dividend policy thereafter.

The investment manager, Downing LLP, has identified a pipeline of potential investments worth about £1.5bn. DORE already has an option over around £40m of this and a further £70m worth of assets are under exclusivity with the investment manager. Downing LLP has a track record of managing 116 investments into solar parks, wind farms and hydroelectric plants since 2010 and these investments had delivered a 9% weighted average gross annualised rate of return (without the benefit of amplifying returns through gearing) as at 30 June 2020.

Diversified renewable energy and infrastructure

Downing Renewables and Infrastructure Trust aims to provide investors with an attractive and sustainable level of income returns, with an element of capital growth, by investing in a diversified portfolio of renewable energy and infrastructure assets located in the UK, Ireland and Northern Europe.

The details of the share issue, including the risk factors that investors should take into consideration, are more fully described in the prospectus published on 12 November 2020 and we urge readers to read this before making any investment decision.

Links to intermediaries:

Investment summary

Downing Renewables and Infrastructure Trust’s (DORE’s) investment objective is to provide investors with an attractive and sustainable level of income returns, with an element of capital growth, by investing in a diversified portfolio of renewable energy and infrastructure assets located in the UK, Ireland and Northern Europe.

The investment manager believes that by investing in a range of renewable energy sources, DORE can reduce the seasonal volatility of revenues and reduce dependency on any single technology to provide more consistent income. There may also be some investments in other infrastructure, whose principle revenues are not derived from energy generation. In addition, diversifying the portfolio geographically should help reduce the portfolio’s regulatory and political risk.

The portfolio will also blend operational projects with projects under construction. The manager says that investment in construction-phase projects offers the potential for higher returns. The amount invested in construction-ready assets or assets under construction will be limited to 35% of gross asset value, as construction projects tend to have more risk associated with them.

The investment manager is Downing LLP, which had AUM of £1.1bn at 30 June 2020. It has a team of 27 investment and asset management specialists focused exclusively on energy and infrastructure transactions. The investment manager has managed 116 investments into solar parks, wind farms and hydroelectric plants since 2010 and these investments had delivered a 9% weighted average gross annualised rate of return (without the benefit of amplifying returns through gearing) as at 30 June 2020.

DORE is targeting a NAV total return of 6.5% to 7.5% per annum over the medium to long term. The intention is to pay dividends quarterly, targeting a dividend of 3p (3% of the 100p per share initial issue price) for the calendar year ended 31 December 2021, rising to 5p for 2022 and adopting a progressive dividend policy thereafter.

The ambition is to raise up to £200m at this stage. DORE already has secured up to £30m, with funds that are managed by Downing on a discretionary basis committing to invest up to £20m and existing Downing clients committing to invest a further £10m.

DORE already owns an option over a portfolio of operational solar PV projects valued at £41.4m. These could be acquired soon after launch. In addition, the investment manager has identified a pipeline of assets valued in excess of £1.5bn, £70m of which is already under exclusivity to the investment manager. The investment manager and the board believe that the net proceeds from the IPO will be substantially invested or committed within 12 months of DORE’s admission to trading (targeted to be 10 December 2020).

The investment opportunity

DORE’s prospectus cites a number of reports that point to a requirement for considerable investment in renewable energy infrastructure. These range from about $1trn of investment over the next decade (based on a 2020 report from the UN Environment Programme) to $13.3trn or 12TW of new generation capacity through to 2050, three-quarters of which is in renewables (based on a forecast by Bloomberg New Energy Finance).

Nearer-term, The International Energy Agency (IEA) forecast in 2019 that global renewable electricity supply would increase by 50% over the five years to 2024, predominantly led by solar PV (60% of overall growth), followed by onshore wind and hydropower. Disruption from COVID-19 may have affected that in the very short-term, but the IEA expects new capacity in 2021 will rebound and match 2019’s record, including an additional 31.9GW expected to be installed in Europe.

There appears to be broad political support for renewable energy deployment and more generation capacity may be needed as heating and transport networks shift to electric power. The UK’s plan to phase out the sale of new cars powered wholly by petrol and diesel by 2030, and ban new homes heated by gas by 2023 is evidence of this.

A changing energy market in Europe

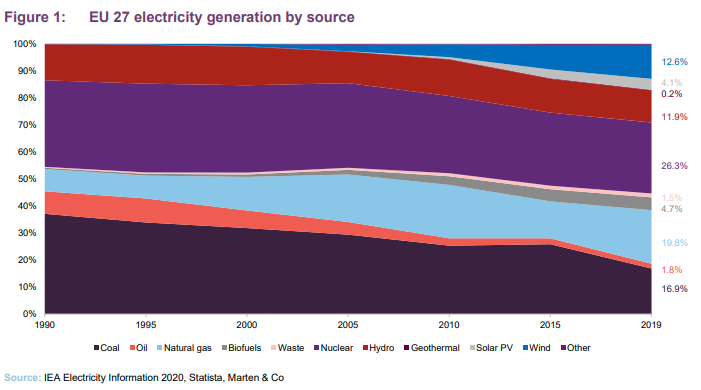

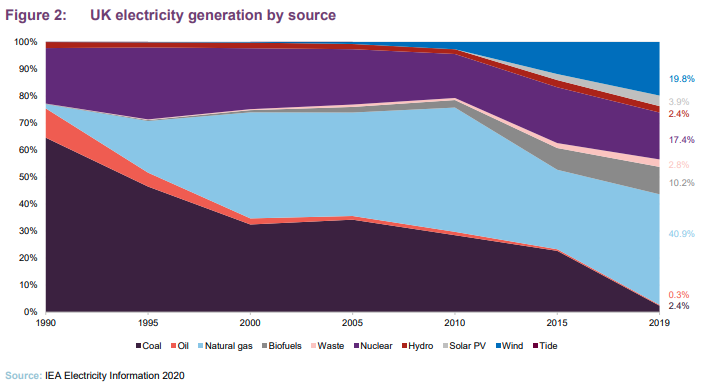

Pages 62 to 71 of DORE’s prospectus published on 12 November 2020 have information on the global electricity generation market and the individual markets that it is focusing on.

The charts in Figures 1 and 2 show how the generation mix has changed since 1990 for both the EU 27 (which excludes the UK) and the UK. Both the EU and the UK are targeting carbon neutrality by 2050.

The EU’s overall target for 2020 was for 20% of gross final energy consumption to derive from renewable sources for all energy uses (including electricity, heat and transport).

Each member state has produced 10-year draft National Energy & Climate Plans, and in some cases set national renewable energy capacity targets. The EC is reviewing these plans, with a view to new ambitions and policies being proposed in 2021; each member state can adopt these as they see fit to meet the EU target.

In 2019, the UK government amended the 2008 Climate Change Act to set a legally binding target to bring 100% of greenhouse gas emissions to net-zero by 2050. Its independent Committee on Climate Change (CCC) emphasised the significant changes required to the economy and major infrastructure to meet this target, including extensive electrification of heat and transport and increased use of clean energy.

The CCC has also noted that the UK is currently not on track to meet its previous target of an 80% emissions reduction by 2050 and that acceleration is needed.

The government has indicated that the next round of CFD auctions scheduled for 2021 will allow new onshore wind and solar PV projects to participate. A fuller explanation of the various types of subsidy is given in the appendix.

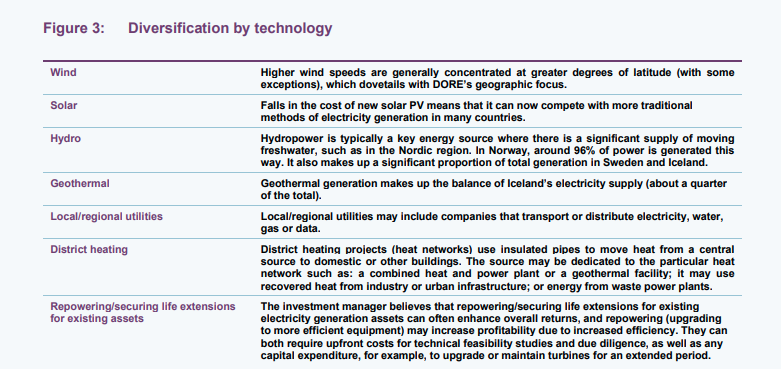

Diversification by technology and geography

The intention is that DORE’s portfolio will be diversified by technology and geography. The prospectus makes reference to wind, solar (photovoltaic – PV – and concentrated solar power), hydroelectric and geothermal. It says that the company may also invest in local/regional utilities, district heating and repowering/securing life extensions for existing electricity generation assets.

DORE will be focused on Northern Europe (UK, Ireland, Norway, Sweden, Finland, Denmark, Iceland, Latvia, Lithuania and Estonia).

The investment manager believes that diversification by technology reduces dependency on a given renewable energy resource and reduces seasonal variability of revenues. In addition, diversification by geography further increases consistency and stability of revenues because:

• different renewable energy resources and thus technologies, are more readily accessible in different geographies;

• the nature and intensity of the same renewable energy resources can differ between geographies; and

• differing geographies can diversify regulatory and policy risk.

Ensuring that the portfolio is diversified by project stage allows DORE to target higher NAV growth by investing in higher returning assets that are in construction or are construction-ready.

The investment manager also believes that investment into other infrastructure assets will reduce DORE’s exposure to merchant power prices.

Green Economy Mark

DORE is expected to qualify for the London Stock Exchange’s Green Economy Mark at admission, which recognises companies that derive 50% or more of their total annual revenues from products and services that contribute to the global green economy. The underlying methodology incorporates the Green Revenues data model developed by FTSE Russell, which helps investors understand the global industrial transition to a green and low carbon economy with consistent, transparent data and indexes.

Investment process

The investment manager will source investment opportunities from its established global network in the renewable energy market. In addition, prospective investments may also be sourced from other funds managed by the Downing group.

DORE will predominantly invest in special purpose vehicles (SPVs) which will individually own the underlying assets. Each SPV will enter into an asset management agreement with Downing’s asset management business (the asset manager), a wholly-owned subsidiary of Downing LLP.

Deal screening

Each prospective investment will first be assessed against DORE’s investment objectives and policy, and also DORE’s ESG policy. If a prospective investment passes that assessment, a high-level financial and economic analysis and review of the investment will be undertaken by the investment manager.

Sighting paper

Downing’s energy and infrastructure investment team will perform an initial review of an investment opportunity and prepare a short summary (a sighting paper) which is shared with the senior management of the investment manager and members of the investment committee.

The sighting paper will include an overview of the opportunity, key characteristics, investment rationale, summary returns, key risks and next steps. Consideration will be given to matters such as suitability (from a portfolio, investment objectives and ESG perspective), high level returns, capital structure, likely transaction structure and process. Other matters highlighted at this stage will include key risks and items to focus on in due diligence.

Following discussion and approval of the sighting paper, the investment team will proceed to submit a non-binding offer in relation to the opportunity. A de minimis initial budget for due diligence may also be approved at this stage.

First stage investment committee approval

Should a transaction proceed to a stage where significant third-party due diligence costs are required to be incurred, the investment team will prepare a deal memorandum with the aim of obtaining first stage approval from the investment committee.

The deal memorandum will include a detailed review of the opportunity. It sets out the investment technology and stage of development, suitability, key risks, returns, jurisdiction and the regulatory and policy background. Detail is also included on the transaction process and timetable and approval is sought for a due diligence budget. The memorandum then continues to outline the key value drivers underpinning the projected returns, principal contractual arrangements, counterparties and stakeholders (including their experience and track record in the sector), an overview of prior performance (where the asset is operational), initial identified risks and proposed due diligence process, advisors and their proposed scopes of work. Any debt or hedging requirements will also be considered at this stage.

The potential impact on DORE’s portfolio of the proposed investment is also outlined. Portfolio composition, concentration, revenue mix and wholesale electricity price exposure are each highlighted before and after inclusion of the proposed investment in an asset.

Due diligence and negotiation

If the investment committee approves, the investment team will be authorised to carry out detailed due diligence within the approved budget and negotiate commercial terms and transaction documentation. This approval will be reported to the board by the investment manager.

Where any potential transactions involve unusual tax implications, low tax jurisdictions, unusual structuring or have significant complexity, potential financial exposure or risk, new technologies or geographical jurisdictions or deviation from approved policies, the investment team will consult the board before the investment manager starts detailed due diligence and negotiation of the commercial terms of the proposed investment.

External advisers may be appointed. Generally, the approach will be to undertake a tender process amongst the panel of preferred advisers for which the Investment Manager has secured preferential rates, to ensure DORE can get the best price and quality for the work required.

The investment team and technical, commercial and energy market specialists from the energy and infrastructure asset management team will work together to conduct detailed due diligence, utilising external professional advisers (including technical, legal, insurance, financial and tax advisers) where needed.

Technical due diligence will typically include a physical site visit and a review of the designs, the construction and maintenance contracts, the planning permissions, accreditations, the grid connection agreements, health and safety assessments and energy yield assessments. In addition to this, where an asset is operational, an analysis of prior performance data and operations and maintenance reports will be undertaken.

Legal due diligence will typically involve external legal advisers reviewing and advising on the contractual structure, the property documents (such as leases, easements, wayleaves and origins of title to land), the planning permissions, the grid connection agreements, construction and maintenance contracts and offtake arrangements.

Financial and tax due diligence will typically include a review of the project budgets, the project financial models, historical financial statements and tax returns. Where a site is operational, the energy yield assessment will take into account prior operational performance and the financial and tax due diligence will include a review of prior financial performance.

The investment manager will also conduct appropriate due diligence on the corporate entities (typically SPVs) that hold the assets and their counterparties to ensure that they are competent, stable and appropriate. In addition, where the investment is in an asset held in shared ownership or co-investment arrangements, the investment manager will negotiate shareholder arrangements and constitutional documents to ensure the interests of the company are appropriately protected.

The investment and asset management teams will direct, review and assess the due diligence findings in order to arrive at an informed view on the risks involved and possible mitigants. The external professional advisers will also work with the investment manager’s teams to establish the optimum financial and tax structures for the prospective investment.

At the same time as carrying out the due diligence, the investment team will enter into negotiations for the commercial terms with the vendor crystallising whether the deal represents an investable proposition. The team will also engage with ESG related risks and opportunities via additional due diligence as needed and via engagement with the seller and related counterparties.

If key aspects of the prospective deal change during this stage, such as key changes in returns, or material risks are encountered during due diligence, then the investment team may revert back to the investment committee to ensure that it is satisfied that the transaction parameters remain with the existing approvals.

Final investment committee approval

Once due diligence and negotiations have substantially completed, a comprehensive investment paper will be prepared for the investment committee and, if approved, shared with the board and the AIFM.

This paper will include a summary of the due diligence findings, detailed forecasts of operational and financial performance, returns and sensitivity analysis and a comparison of the transaction against prior transactions by the company and comparable transactions in the wider market.

The paper will also include details of the ESG evaluation, measures to ensure effective stewardship of these principles on an ongoing basis, reporting protocols and how periodic reviews will be conducted. The board will have the opportunity to make such observations and comments, communicating such observations and comments to the investment committee. The committee will consider and take account of the observations and comments received from the board and, if necessary, re-evaluate the proposal.

Save as set out below, any decision to proceed with a transaction shall be the sole responsibility of the investment manager. The acquisition of assets from, disposal of assets to, or co-investment by DORE with other Downing managed funds will be subject to approval from the board (all of whom are independent of the investment manager) prior to the acquisition, disposal or co-investment proceeding.

Pre-completion

The investment team will facilitate completion of the transaction through provision of the following services:

• negotiating the final forms of all transaction documents;

• ensuring appropriate insurance is put in place; and

• establishing the relevant company structure and necessary bank accounts.

The investment committee will review a final note outlining any material changes since the final deal memorandum was signed off. Following that note’s approval, the investment team will inform the board of any such changes and the board will again be given the opportunity to make such observations and comments as it thinks fit.

Post completion

During the transaction process the asset management team will start on-boarding the asset to its systems. After the completion and execution of the transaction, the investment team will finalise handover by completing a checklist documenting matters, including:

• registration of documentation with the relevant authorities and filing of company secretarial documents;

• filing of insurance policies, legal bible, completion statements, loan notes, share certificates etc.;

• clearance of any conditions subsequent;

• confirmation of cash receipts/payments by solicitors;

• balance sheet opening position;

• scheduling of SPV board meetings, accounting timelines etc.;

• scheduling of debt service payments and reporting requirements;

• setup and reporting on KPIs:

– operational;

– financial;

– commercial; and

– ESG.

Asset management

The investment manager’s proactive approach to asset management allows direct control of key decision making, risk management and performance optimisation. The investment manager considers asset management as a fundamental pillar to ensuring proper performance and governance and thereby protecting, and creating, value for the company.

The asset management team has dedicated engineering, commercial, data, financial and operations functions with each function being responsible for providing the relevant scope of services to the assets. The management team sits above the specialist functions and provides oversight as to asset and service performance.

The asset management team is responsible for directing the activity of third-party contractors, managing key commercial contracts (construction, maintenance and leases), bookkeeping and accounting, portfolio performance and reporting thereon to the board. In doing so, the key areas of focus are:

• portfolio performance against key metrics;

• asset level performance including operational and financial performance;

• contractor performance including compliance with contractual obligations and identifying opportunities for optimisation;

• supporting the investment manager in the valuation process;

• ESG compliance, governance, health, safety and environmental and regulatory compliance; and

• stakeholder and counterparty management, including offtakers, communities, finance providers and investment partners.

The asset management team oversees the sale of the power, leveraging the asset manager’s scale to try to achieve attractive risk adjusted prices. The team will seek to structure deals that drive competitive tension whilst allowing flexibility to facilitate further price hedging during the contract term.

ESG

Downing LLP is a signatory to the UN Principles of Investment, which means that it:

• incorporates ESG issues into its investment analysis and decision-making processes;

• partakes in ‘active’ ownership policies and practices;

• seeks appropriate disclosures on ESG issues;

• works to promote the principles and enhance their implementation; and

• reports on such activities and progress.

The investment manager has developed a carbon lifecycle assessment methodology to provide a detailed understanding of the CO2eq emissions of different types of investments. By performing carbon lifecycle assessments, the investment manager intends to use this information to inform its decision making on its choice of suppliers for goods and services relating to its portfolio of investments.

As a signatory to HM Treasury’s Investing in Women Code, the investment manager is also committed to improving female entrepreneurs’ access to tools, resources and finance.

Borrowing policy

Long-term limited recourse debt at the SPV level may be used to facilitate the acquisition, refinancing or construction of assets. Where utilised, the company will seek to adopt a prudent approach to financial leverage with the aim that each asset will be financed appropriately for the nature of the underlying cashflows and their expected volatility. Total long-term structural debt will not exceed 50% of the prevailing gross asset value at the time of drawing down (or acquiring) such debt.

In addition, the company and/or its subsidiaries may make use of short-term debt, such as a revolving credit facility, to assist with the acquisition of suitable opportunities as and when they become available. Such short-term debt will be subject to a separate gearing limit so as not to exceed 10% of the prevailing gross asset value at the time of drawing down (or acquiring) any such short-term debt.

Currency and hedging policy

The company will adopt a structured risk management approach in seeking to deliver stable cash flows and dividend yield.

This may include entering into hedging transactions for the purpose of efficient portfolio management. This could include:

• foreign currency hedging on a portion of equity distributions;

• foreign currency hedging on construction budgets;

• interest and/or inflation rate hedging through swaps or other market instruments and/or derivative transactions; and

• power and commodity price hedging through power purchase arrangements or other market instruments and/or derivative transactions.

Any such transactions will not be undertaken for speculative purposes.

Holding and exit strategy

It is intended that assets will be held for the long-term. However, if an attractive offer is received or is likely to be available, consideration will be given to the sale of the relevant asset and reinvestment of the proceeds.

Investment restrictions

The company will observe the following investment restrictions when making investments:

• the company may invest no more than 60% of gross asset value (GAV) in assets located in the UK;

• the company may invest no more than 60% of GAV in assets located in Ireland and Northern Europe (Denmark, Sweden, Norway, Finland, Iceland, the Baltic States, Germany and France) combined;

• no more than 25% of GAV will be invested in assets where the company does not have a controlling interest;

• no investments will be made in companies which generate electricity through the combustion of fossil fuels or derive a significant portion of their revenues from the use or sale of fossil fuels unless the purpose of the investment is to transition those companies away from the use of fossil fuels and toward sustainable sources; and

• the company will not invest in other UK listed closed-ended investment companies.

The Company will observe the following investment restrictions when making investments, with the relevant limits being calculated on the assumed basis that the company has gearing in place of 50% of GAV:

• the Company may invest no more than 50% of GAV in any single technology;

• the Company may invest no more than 25% of GAV in other infrastructure;

• the Company may invest no more than 35% of GAV in assets that are in construction or construction-ready;

• the Company may invest no more than 30% of GAV in any one single asset, and the Company’s investment in any other single asset shall not exceed 25% of GAV; and

• at the time of an investment or entry into an agreement with an offtaker, the aggregate value of assets under contract to any single offtaker will not exceed 40% of GAV.

Following full investment of the IPO proceeds and the company becoming substantially geared (meaning for this purpose long-term debt of 50% of GAV), the portfolio will comprise no fewer than six assets.

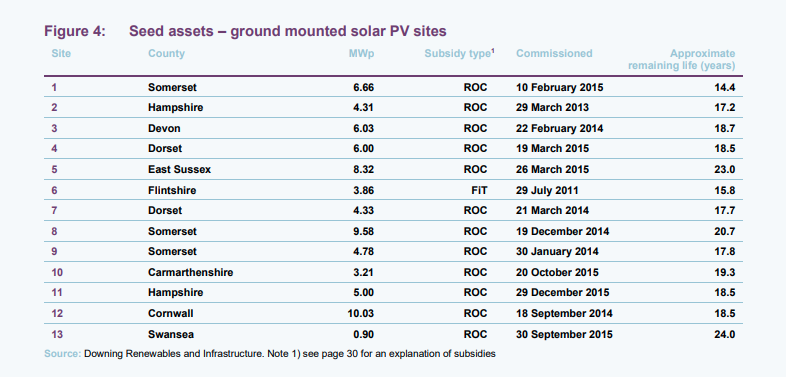

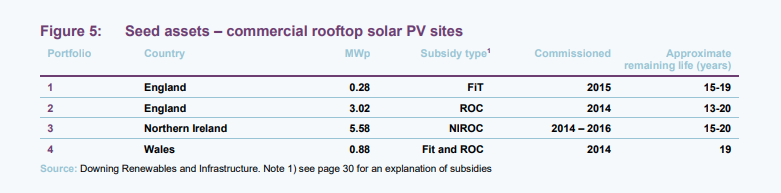

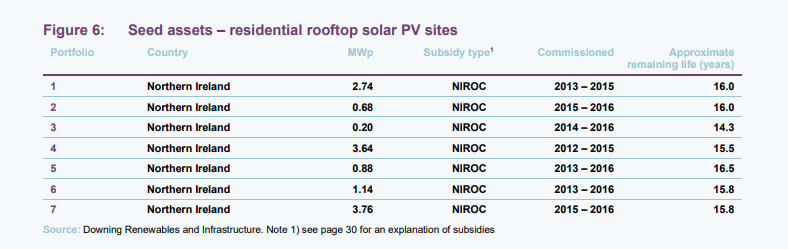

Seed assets

DORE has an option to acquire a portfolio of about 96 MWp of operational solar PV projects located in the UK for £41.4m (plus the assumption of the associated debt – see below). The projects in the portfolio have an average operating track record of around six years and have generated revenue of £12.5m and EBITDA of £9.9m in the year to 31 March 2020. The projects are currently managed by Downing’s asset management team and the recent technical performance of the assets has been strong.

The portfolio is comprised of:

• 13 ground-mounted sites located across mainland Great Britain totalling about 73 MWp;

• 28 commercial rooftop installations totalling about 10 MWp; and

• 7 residential rooftop portfolios in Northern Ireland totalling about 13MWp.

Historically, the ground mounted sites have accounted for approximately 80% of annual generation across the portfolio and around 70% of total revenues.

The 28 commercial rooftop sites are held across 4 portfolios and total 9.8MWp. The portfolios include a 3.6MWp installation at a large commercial facility in Belfast. Historically, the commercial sites have accounted for approximately 8% of annual generation across the portfolio and around 10% of total revenues.

The seven residential rooftop portfolios are spread across Northern Ireland. Around 3,200 systems are included within the seven portfolios. Historically they have contributed the balance of approximately 12% of annual generation across the portfolio and around 20% of total revenues. NIROCs represent approximately 90% of the residential rooftop portfolios’ income with a weighted average accreditation of 3.7 NIROCs.

The average annual subsidy revenues represent close to 65% of total annual revenue projected for the next 10 years. This reduces to around 55% of total revenue across the entire remaining project life.

To mitigate the exposure to wholesale power price risk, Downing LLP has put in place a series of measures, including private wire sales, fixed price power purchase agreements (PPAs) and PPA floor prices. Fixed price arrangements can be entered into with the PPA provider on a rolling basis, typically up to four seasons ahead. In relation to all 73MWp of ground-mounted sites, a long-term PPA, which runs until March 2032, was entered into with Statkraft Markets GmbH in March 2017, with such sites on a fixed wholesale power price arrangement for winter 2020/21.

Financing of the seed assets

The assets are owned by a group of SPVs with a single holding company which is the borrower under a loan agreement with a senior debt lender. Subject to the option being exercised, the seed assets will be acquired subject to the current financing arrangements. The key terms of the senior debt are as follows:

• debt outstanding (as of 31 March 2020):

– approximately £58.9m in an RPI-linked facility (split roughly between £55.3m of initial principal and £3.6m of accreted inflation);

– approximately in a £10.4m fixed rate facility;

• interest rate:

– for the RPI-linked facility: 0.5% real

– for the fixed rate facility: 3.37% all-in (1.17% fixed rate plus a 2.2% margin);

• remaining term: about 14.5 years (final repayment September 2034); and

• fully amortising with semi-annual payments.

In addition, there is a short-term fixed rate 5.60% debt facility with £10.9m outstanding (as of 31 July 2020) which can be repaid without penalty from September 2022.

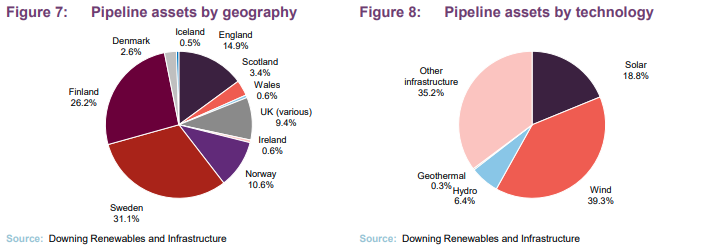

The pipeline

The investment manager has identified a significant pipeline of assets with a value in excess of £1.5bn, of which assets with a total equity value of approximately £70 million are under exclusivity to the investment manager.

The pipeline assets break down into:

Wind:

• ten construction projects for an average purchase price of about £60m each

– (including two construction-ready wind farms in Sweden with a target of securing 10-year PPAs)

• and four operational projects for about £20m each

– (including a Finnish wind farm with the potential to expand the project by up to 50%. The project was awarded a 12-year subsidy through the national auction system run by the Finnish Energy Authority); and

– (an operational portfolio of more than 100 discrete wind turbines totalling 12.5MW across Great Britain and Northern Ireland. The projects qualify for either FITs or NIROCs under various PPAs, and utilise a range of different turbine models and manufacturers).

Solar:

• fifteen construction projects

– (including a series of 6 new-build solar projects in the UK totalling c.8MWp, each with an anticipated 100% take or pay arrangement for 30 years with a UK regulated utility. Construction of these assets is expected to commence in the first half of 2021. In addition to these initial 6 projects, the developer has a wider pipeline including 10 projects totalling 35MWp);

• and two operational projects at about £20m each.

Hydro:

• five operational projects at about £20m each

– (including a diversified portfolio of operational small-scale hydropower plants located in central and southern Sweden with the capacity to produce c.108GWh of electricity per annum. The portfolio has been operating for over 50 years and is located across three rivers. Several power plants benefit from upstream dams, allowing for both short-term and seasonal production optimisation. The anticipated strategy in relation to this opportunity is to secure a 7-10-year fixed PPA); and

– (a portfolio of 5 run-of-river hydropower facilities in Norway – 4 operational and 1 in construction – the oldest of which has been operating for 10 years. The facilities have the capacity to produce 22.5GWh of electricity per annum. The developer has a further pipeline of opportunities and is seeking to enter into an agreement with the acquirer of the portfolio to acquire those projects once constructed. The anticipated strategy in relation to this opportunity is to secure a 7-10 year fixed PPA.)

Geothermal:

• one operational project for about £5m; and

Other Infrastructure:

• three construction projects at about £15m each and three operational projects at about £180m each.

– (including A regulated heat supply business in Denmark. The company is targeting converting its current heat customers from fossil fuels to renewable energy heat solutions. The company also invests in renewable energy generation and, in 2019, entered into an agreement with the local government to fund the construction of a c.20MW wind farm).

Valuation

NAVs will be published quarterly based on valuations of assets as at the end of each calendar quarter.

The valuation principles used to calculate the fair value of assets will follow International Private Equity and Venture Capital Valuation Guidelines (last edition December 2018). Fair value for operational assets will typically be derived from a discounted cash flow (DCF) methodology and the results will be benchmarked against appropriate multiples and key performance indicators, where available for the relevant sector/industry. For assets that are not yet operational at the time of valuation, the price of recent investment may be used as an appropriate estimate of fair value initially, but it is likely that a DCF will provide a better estimate of fair value as the asset moves closer to operation.

The investment manager will use its judgement in arriving at appropriate discount rates.

A range of sources will be reviewed in determining the underlying assumptions used in calculating the fair market valuation of each asset, including but not limited to:

• macroeconomic projections adopted by the market as disclosed in publicly available resources;

• macroeconomic forecasts provided by expert third party economic advisers;

• discount rates publicly disclosed by the company’s peers;

• discount rates applicable to comparable infrastructure asset classes, which may be procured from public sources or independent third party expert advisers;

• discount rates publicly disclosed for comparable market transactions of similar assets; and

• capital asset pricing model outputs and implied risk premia over relevant risk free rates.

Where available, assumptions will be based on observable market and technical data. For other assumptions, the AIFM and the investment manager may engage independent technical experts such as electricity price consultants to provide long-term forecasts for use in its valuations.

The NAV will be subject to a review by the board.

Dividend policy

DORE intends to pay dividends on a quarterly basis with dividends typically declared in respect of the quarterly periods ending March, June, September and December and paid in June, September, December and March respectively. The first interim dividend is expected to be declared in respect of the period from admission to 30 June 2021 and paid in September 2021.

Distributions may take either the form of dividend income, or of “qualifying interest income” which may be designated as interest distributions for UK tax purposes.

DORE will target an initial dividend yield of 3% by reference to the 100p issue price in respect of the calendar year to 31 December 2021, rising to a target dividend yield of 5% by reference to the issue price in respect of the calendar year to 31 December 2022. Thereafter, the company intends to adopt a progressive dividend policy.

Premium/discount management

The board has said that it intends to seek to limit, as far as practicable, the extent to which the market price of the ordinary shares diverges from the NAV.

Premium management

In the period from admission until the first annual general meeting of the company, the directors have authority, which they can use at their discretion, to issue such number of ordinary shares and/or C shares in aggregate as is equal to 20% of the number of ordinary shares in issue immediately following admission.

No ordinary shares will be issued at a price less than NAV at the time of their issue.

Discount management

The directors will consider repurchasing ordinary shares in the market if they believe it to be in shareholders’ interests and as a means of correcting any imbalance between the supply of and demand for the ordinary shares.

A special resolution has been passed granting the directors authority, at their discretion, to repurchase up to 14.99% of the issued ordinary share capital immediately following admission. This authority expires on the conclusion of the earlier of the company’s first annual general meeting or 25 April 2022. Renewal of this buy-back authority will be sought at each annual general meeting or more frequently if required. Ordinary shares repurchased may be held in treasury or cancelled.

Treasury shares

Companies can hold repurchased shares as treasury shares, rather than having to cancel them. These shares may be subsequently cancelled or sold for cash. This would give the company the ability to reissue ordinary shares quickly and cost effectively, thereby improving liquidity and providing the company with additional flexibility in the management of its capital base.

No ordinary shares will be sold from treasury at a price less than NAV unless they are first offered pro rata to existing shareholders.

Fees and costs

The costs and expenses of, and incidental to, the formation of the company and the issue are expected to be 2% of the gross proceeds, equivalent to £4m and the starting NAV per share will be 98p (in both cases assuming gross proceeds of £200m). The investment manager has agreed to contribute to the costs of the issue such that the NAV at admission will not be less than 98p.

The company’s ongoing charges are estimated at 1.40% per annum (based on a fund size of £200m). These include fees payable to the investment manager, the company secretary, depositary, registrar and auditor, as well as directors’ fees.

Investment manager fee

The investment manager is entitled to a management fee of 0.95% per annum of NAV up to £500m and 0.85% per annum on amounts in excess of £500m. The fee is payable quarterly in arrears. There is no performance fee.

The asset manager, a wholly owned subsidiary of the investment manager, will also charge separate asset level fees.

The investment management agreement is for an initial term of five years from the date of admission and thereafter is subject to termination on not less than 12 months’ written notice by any party.

Other ongoing charges

Company secretarial and administration fees

Company secretarial services will be provided by Link Company Matters Limited in exchange for a fee of £59,100 per annum. In addition, a fee of £15,000 is payable to Link Company Matters Limited for services undertaken as part of the admission process.

Depositary

The Depositary is entitled to an annual fee of £45,000 (exclusive of VAT) per annum.

Registrar

Link Market Services Limited will act as registrar and is entitled to a fee calculated on the basis of the number of shareholders, the number of transfers processed and any common reporting standard on-boarding, filings or changes. The annual minimum fee is £2,500 (exclusive of VAT). In addition, the Registrar is entitled to certain other fees for ad hoc services rendered from time to time.

Auditor

BDO LLP provides audit services to the company. The fees charged by the auditor will depend on the services provided and on the time spent by the auditor on the affairs of the company.

Capital structure and life

Following admission to trading, DORE will have just ordinary shares in issue and no other classes of share capital.

DORE will have an unlimited life. However, the company’s articles, require the directors to propose a continuation resolution (as an ordinary resolution) at a general meeting to be held in December 2025 and then again at the annual general meeting to be held in 2031 and at each fifth annual general meeting thereafter.

If a majority of shareholders vote against continuation, the directors will put forward proposals for the reconstruction or reorganisation of the company.

The company’s financial year end will be 31 December and the first set of full accounts will cover the period from launch to 31 December 2021. The first AGM will be held by 7 April 2022.

Investment adviser

Downing LLP was founded in 1986 and is led by Tony McGing (chief executive officer) and Nick Lewis (chairman). As at 30 June 2020, Downing LLP had approximately 160 employees in the UK, located across two main offices in London and Cardiff, and approximately £1.1bn of assets under management.

Energy and infrastructure (E&I)

The dedicated E&I team is split across two sub-teams: investment and asset management, and is supported by a wider business operations team. The E&I team has over a decade of experience in the E&I sector.

Areas of activity include:

• core renewables such as wind, solar photovoltaic and hydro-electric projects;

• biomass and anaerobic digestion projects;

• flexible energy generation;

• energy storage; and

• electric vehicle infrastructure.

The E&I team has extensive experience in managing complex contractual, technical and legal issues. It has supported projects at all stages of development, from pipelines of shovel-ready projects through to mature operational assets.

Investment team

The investment team is responsible for originating, negotiating and executing renewable energy and infrastructure investments. It is responsible for all aspects of the capital and acquisition structure, including raising debt finance.

The 12-strong investment team has an average experience of more than 12 years of working in the sector. The key individuals responsible for executing the DORE’s investment strategy are:

Tom Williams – partner, head of energy and infrastructure

Tom heads up the team, which he joined in July 2018. He has 20 years of experience as principal and adviser across the private equity and private debt infrastructure sectors. Tom has carried out successful transactions totalling in excess of £13bn in the energy, utilities, transportation, accommodation and defence sectors.

He started his career working as a project finance lawyer in 1999 before moving into private equity with Macquarie Group in London and the Middle East. Tom holds a Postgraduate Diploma in Legal Practice from the Royal College of Law and a BA in law from Cambridge University.

Henrik Dählstrom – investment director

Henrik joined as investment director in June 2020 to expand the team’s European presence and lead transactions in the Nordic regions. Henrik spent 17 years with Macquarie Infrastructure and Real Assets (MIRA). When leaving MIRA, Henrik was a director responsible for covering the Nordic region. This role included the origination and execution of transactions in the renewable energy and infrastructure sectors as well as holding asset management and board responsibilities.

Henrik has worked across renewable energy and infrastructure sectors as a principal for investments in the UK and in Europe. He holds a bachelor’s degree in Business and Finance from Bond University and a master’s degree in finance from the University of Gothenburg.

Sean Moore – investment director

Sean joined the team in August 2017. He focusses on the origination and execution of investments in a wide range of energy and infrastructure sectors, noticeably in the core renewables, flexible generation and energy storage sectors.

Before joining Downing LLP, Sean held the role of vice president at the Green Investment Bank, where he worked on energy and infrastructure deals, including onshore renewable, energy efficiency and energy storage projects. Prior to this, Sean was an associate for the leverage finance team at ING Bank. Sean holds a BA in economics from Cambridge University.

Asset management team

A 15-strong team is dedicated to effective asset management, being responsible for the operational and financial performance of the renewable and energy infrastructure assets. The team focusses on performance management and asset optimisation to protect and enhance returns to investors. This includes managing outsourced services from third party providers who provide services to the renewable and energy infrastructure assets. The team manages over 400MWp of energy generating assets across five separate technologies.

ESG monitoring and reporting also sits within the asset management team.

The key individuals responsible for technical and commercial asset management of DORE’s portfolio are:

Tom Moore – head of asset management

Tom joined as head of asset management in May 2019. Prior to joining the investment manager, Tom was a director at Foresight Group, where he had oversight of a significant portfolio of renewable energy investments. Whilst at Foresight, Tom was actively involved in the ongoing management of its first investment trust, overseeing administration, valuation and audit obligations as well as asset and portfolio performance. He has a wealth of experience in monitoring the type of target assets the company will invest in as well as institutional-standard reporting.

Danielle Strothers – associate director, asset management

Danielle joined the team in September 2019. She is responsible for business operations and processes across the infrastructure asset management team, focussing on contractor performance, compliance and reporting. Prior to joining the investment manager, Danielle was a senior portfolio manager within the infrastructure team at Foresight Group. She is a chartered accountant and holds a BSc in Accounting & Finance from the University of Birmingham.

Coos Battjes – energy market specialist

Coos joined the investment manager in November 2018 as a specialist energy market’s adviser. He is responsible for structuring route-to-market contracts and enhancing the value of an energy and infrastructure’s portfolio. Coos has an extensive record in the energy and carbon markets having worked for energy utilities, financial institutions, consultancy and research foundations over a career spanning 20 years. Coos holds a PhD in Math and Natural Science from the University of Groningen in the Netherlands.

Pedro Perejon – associate director, technical lead

Pedro joined the investment manager in October 2018 as technical asset manager. He provides oversight of Downing LLP’s infrastructure asset portfolio to protect and enhance returns for its investors. He currently manages a diverse portfolio including solar, storage, wind, bioenergy and reserve power assets. Pedro has over 10 years of experience in the renewable energy sector and has been involved in many projects from development to final exit across the EMEA (Europe, Middle East and Africa) region.

Business operations team

The around 90-strong business operations team is responsible for controls, governance, processes, administrative support, systems and leading business improvement initiatives to set the investment manager’s business up for scale.

The business operations team provides comprehensive support for its day-to-day operations. This includes internal controls (governance, legal, compliance and risk), processes, administrative support and human resource functions, finance, accounting and IT systems and support.

The team includes James Weaver (partner and chief operating officer), ex-general counsel and partner of a London based hedge fund and the chief operating officer of a national specialist lender; Peter Naylor (partner and legal counsel); and Danielle Jones (compliance director), with over 20 years of compliance experience.

Investment committee

The investment committee consists of:

• Chris Allner – partner and chairman of investment committee.

• Nick Lewis – founding partner and chairman

• Tony McGing – partner and chief executive officer

• Kostas Manolis – partner and head of unquoted investments

• Colin Corbally – partner and head of investment strategy

• Jonathan Boss – partner

• Andrew Jameson – non-executive chairman

Board

The board is comprised of three non-executive directors each of whom is independent of the manager and does not sit together on other boards. The chairman’s fee will be £50,000 per annum and the fees for the other directors £35,000 per annum, with an additional £5,000 per annum payable to the chair of the audit and risk committee. Joanna de Montgros has asked for her first year’s fees to be paid in shares. Hugh Little and Ashley Paxton have indicated that they will subscribe for 50,000 and 40,000 shares respectively.

Hugh Little (non-executive chairman)

Hugh qualified as a chartered accountant in 1982. In 1987, he joined Aberdeen Asset Management (AAM) and, from 1990 to 2006, oversaw the growth of the private equity business before moving into the corporate team as Head of Acquisitions. Hugh retired from AAM in 2015, since then he has become chair of both Drum Income Plus REIT Plc and CLAN Cancer Support, a director of Dark Matter Distillers Limited, and a governor of Robert Gordon’s College. Hugh won the ‘Non-Executive Director of the Year’ award at the Institute of Directors, Scotland awards ceremony held in May 2019.

Joanna de Montgros (non-executive director)

Joanna is a specialist in the technical and commercial elements of energy projects, with 20 years’ experience in renewable energy and flexibility investments, building on her academic engineering background. In 2015, Joanna co-founded international consultancy company Everoze. Everoze provides a broad range of engineering and strategic consulting services, plus development of other start-ups in this space. Prior to co-founding Everoze, Joanna led the global Project Engineering group within DNV GL Renewables and was a member of the DNV GL Renewable Advisory Board.

Jo’s early career included management consultancy (PWC) and project finance (Fortis Bank).

Ashley Paxton (non-executive director)

Ashley has 25 years’ experience serving the funds and financial services industry in London and Guernsey. Throughout that period, he has served a large number of London listed fund boards on IPOs & other capital market transactions, audit and other corporate governance matters. Ashley has been a partner with KPMG in the Channel Islands since 2002 and transitioned from audit to become its C.I. head of advisory in 2008, a position he held through to his retirement from the firm in 2019.

Ashley is a Fellow of the Institute of Chartered Accountants in England and Wales and a resident of Guernsey. Amongst other appointments he serves on the board of JZ Capital Partners Limited and is chairman of the Youth Commission for Guernsey & Alderney, a locally based charity delivering high quality targeted services to children and young people to support the development of their social, physical and emotional wellbeing.

Appendix

Sources of revenue

A number of sources of revenues are available to renewable energy generators depending on various factors, including the type of technology used, the project location, and its commissioning date.

Power Purchase Agreements (PPAs) are contracts between an electricity generator and a buyer to sell electricity produced by the generator for a given period of time. Pricing can be variable, typically determined by reference to an index, or can be fixed for a given period, or a combination of the two. They often incorporate the sale of green certificates (see below).

The following revenue sources are of most significance in appraising renewable energy generators:

Wholesale electricity

Electricity cannot (currently) be easily stored at scale, therefore demand must be quickly balanced against supply through the wholesale markets, which enable trade of electricity between suppliers, generators, traders and customers. A generator selling power on a wholesale market receives the available market price at the time, which will fluctuate. Wholesale electricity revenues are therefore not guaranteed until the point of trade, unless a generator enters into a forward-looking fixed price arrangement.

Fixed price arrangements

There are a variety of different fixed price arrangements. A PPA could be for a fixed price for its entire term, with such price either remaining constant or increasing with inflation over the relevant period. Certain PPAs have the ability to progressively fix pricing for a defined number of periods ahead. It is possible to enter into longer fixed price arrangements on a bilateral basis with commercial counterparties, which can extend to 10 years or longer.

Floor price arrangements

PPA providers may offer a floor price arrangement, which sets a minimum price for wholesale electricity below which the generator will receive the floor price rather than the lower wholesale electricity price. Floor prices can thus provide a level of certainty over the minimum price achieved per unit of electricity sold into the wholesale market.

Onsite consumption

Renewable energy projects are often installed at or near the location of their final electricity consumption, thereby avoiding the transmission system and distribution network. This is common in the rooftop solar sector where panels are typically installed on the roof of a building and some or all of the energy is consumed by the occupier.

Subsidy-backed

There are various subsidy support schemes used by governments to encourage the deployment of renewable energy generation. The principal mechanisms are described below along with several specific country examples:

Green/renewable electricity certificates

Some countries require electricity retailers (utilities) to source a certain quantity from eligible renewable energy generators. Retailers must evidence this by presenting certificates to regulators (often called renewable energy or green certificates), which show how much renewable energy was produced/consumed. The sale of these certificates can be an important revenue stream for renewable energy generators, as they are bought and traded by retailers to meet their quota.

In the UK, a PPA often incorporates the sale of Renewables Obligation Certificates (ROCs), which verify that suppliers have fulfilled their Renewables Obligation (RO). ROCs are issued to renewable generating stations based on generated renewable electricity and can be traded; if a supplier cannot meet its annual RO, it must otherwise pay a fixed penalty into the “buy-out fund”.

After administration costs, the surplus in the buy-out fund goes back to suppliers that met their RO according to their ROCs submitted.

The Northern Ireland Renewables Obligation (NIRO) follows the same RO system as Great Britain, offering up to four Northern Ireland ROCs (NIROCS) per MWh for small-scale onshore wind (less than or equal to 250kWp). Both the RO and the NIRO schemes closed to new generators in March 2017.

Since 2012, Norway and Sweden have supported the buildout of renewables by participating in their own electricity certificate scheme (Elcerts or Elcertificates) which provide generators with a revenue stream of up to 15 years from commissioning of the relevant asset to supplement their income from electricity generation. The Elcerts market is supported by obligatory purchasing by utilities to meet their clean energy supply quota to customers. Whilst similar to ROCs, the price of Elcerts fluctuates as it does not have a ‘headroom’ mechanism to ensure demand exceeds supply, nor a fixed penalty to set prices. In 2016 Norway announced its exit from the Elcerts framework for projects commissioned after 2020, whilst Sweden has proposed a 2021 end date with qualifying projects receiving Elcerts up until 2035.

Auction schemes and contracts for difference (CFD)

In the UK, government-backed CFDs incentivise investment in renewable energy by providing electricity generators, who have high upfront costs and long asset lifetimes, with direct protection from downward wholesale price movements.

Typically, eligible electricity generators enter a public auction to bid a ‘strike price’ for CFD contracts, which are then awarded to the lowest strike prices. In contrast to a PPA which sells physical power from the electricity generator, a CFD is a financial instrument. Successful CFD bidders (electricity generators) are paid the difference between the strike price and a ‘reference price’ (a measure of the average market price for electricity in the given market) for the electricity they produce over a fixed term, for example 15 years in the case of the UK CFD regime.

If the reference price is below the strike price, the generator receives a top-up payment. Conversely, if the reference price is above the strike price, the generator pays the difference. The net result is that the generator receives a fixed price over the term of the CFD.

A corporate-backed CFD is similar to a government–backed CFD, except the contract counterparty is a (typically creditworthy) corporate entity.

Feed-in tariffs or premiums

Feed-in Tariffs (FiTs) are government subsidies paid to renewable generators for the amount of renewable electricity generated, regardless of the wholesale price, whilst Feed-in Premiums (FiPs) make a top-up payment over and above the wholesale price. Originally set up to promote renewable energy installation, FiT / FiP rates have gradually regressed or the schemes closed entirely across many countries, as technology costs have continued to fall.

Embedded benefits

‘Embedded benefits’ is a broad term that categorises various revenue streams available to embedded generators for the reduction or avoidance of certain supply costs, due to such generators being located on the distribution network, rather than the national transmission system. Such a distribution connection saves suppliers certain costs, which can be shared with the generators. In the UK, additional value can be obtained from, for example, Generation Distribution Use of System (GDUoS) credits, whereby generators negate the need for certain distribution network upgrades.

In the UK, the combination of benefits available to embedded generators has provided an increasingly significant revenue stream, through a combination of rising distribution network upgrade costs being spread across a reducing demand base to which they can be charged back, as overall energy consumption has fallen. As such, the regulator has sought to align such benefits with their real financial value to the network and balancing arrangements.

For example, Ofgem’s Targeted Charging Review in the UK impacts those embedded benefits, primarily ‘triad’ payments for generating at points of peak annual demand. This has resulted in a significant revenue reduction depending on the generator’s location (in some locations having reduced to £nil) under the new ‘Embedded Export Tariffs’.

In the Nordic region and continental Europe, there is generally no specific concept of embedded benefits, i.e. no charges or benefits for being a distribution-connected generator.

Regulated revenue

Other Infrastructure could include privatised utilities which are regulated to ensure owners do not achieve “super normal” profits from their natural monopoly position as, for example, the local electricity supply company. The regulatory asset base model (RAB) is used in many countries. This provides a cap on the price that customers can be charged, ensuring sufficient profits to cover operations and maintenance of the assets, and a reasonable return on capital. Contractual efficiency incentives are typically included to encourage gains in production and operations.

The nature of such regulated revenues means that, subject to reasonable performance of the owner, there is a predictable level of return, which reduces the risk on investment for capital intensive projects.

Potential impact of Covid-19 on renewable electricity generator revenues

In 2020, the global coronavirus pandemic has significantly reduced global economic activity, causing very significant reductions in near-term demand for electricity. For acquisitions of projects going forward a “best estimate” of the effect of the pandemic has been factored into power price forecasts produced by market consultants that the Company uses. However, it remains unclear what the effect will be on wholesale electricity prices and therefore how accurate these forecasts are, given the various possible national trajectories out of the pandemic and any possible resurgence of the virus in the future.

Electricity demand in Europe has shown some recovery, from 10% below 2019 levels at June 2020 to 5% lower by July 2020, across all EU countries except Italy. Due to its low marginal operating cost and priority grid access, demand for renewable electricity actually increased during the same period.

IMPORTANT INFORMATION

Marten & Co (which is authorised and regulated by the Financial Conduct Authority) was paid to produce this note on Downing Renewables and Infrastructure Trust Plc.

This note is for information purposes only and is not intended to encourage the reader to deal in the security or securities mentioned within it and readers should place no reliance on the information contained therein.

Marten & Co is not authorised to give advice to retail clients. The research does not have regard to the specific investment objectives, financial situation and needs of any specific person who may receive it.

This note has been compiled from publicly available information and information and should be read in conjunction with the Downing Renewables and Infrastructure Trust prospectus published on 12 November 2020. This note is not directed at any person in any jurisdiction where (by reason of that person’s nationality, residence or otherwise) the publication or availability of this note is prohibited.

Accuracy of Content: Whilst Marten & Co uses reasonable efforts to obtain information from sources which we believe to be reliable and to ensure that the information in this note is up to date and accurate, we make no representation or warranty that the information contained in this note is accurate, reliable or complete. The information contained in this note is provided by Marten & Co for personal use and information purposes generally. You are solely liable for any use you may make of this information. The information is inherently subject to change without notice and may become outdated. You, therefore, should verify any information obtained from this note before you use it.

No Advice: Nothing contained in this note constitutes or should be construed to constitute investment, legal, tax or other advice.

No Representation or Warranty: No representation, warranty or guarantee of any kind, express or implied is given by Marten & Co in respect of any information contained on this note.

Exclusion of Liability: To the fullest extent allowed by law, Marten & Co shall not be liable for any direct or indirect losses, damages, costs or expenses incurred or suffered by you arising out or in connection with the access to, use of or reliance on any information contained on this note. In no circumstance shall Marten & Co and its employees have any liability for consequential or special damages.

Governing Law and Jurisdiction: These terms and conditions and all matters connected with them, are governed by the laws of England and Wales and shall be subject to the exclusive jurisdiction of the English courts. If you access this note from outside the UK, you are responsible for ensuring compliance with any local laws relating to access.

No information contained in this note shall form the basis of, or be relied upon in connection with, any offer or commitment whatsoever in any jurisdiction.

Investment Performance Information: Please remember that past performance is not necessarily a guide to the future and that the value of shares and the income from them can go down as well as up. Exchange rates may also cause the value of underlying overseas investments to go down as well as up. Marten & Co may write on companies that use gearing in a number of forms that can increase volatility and, in some cases, to a complete loss of an investment.

QuotedData is a trading name of Marten & Co, which is authorised and regulated by the Financial Conduct Authority.