Aberdeen Emerging Markets Investment Company – Peer group leading China exposure

Peer group leading China exposure

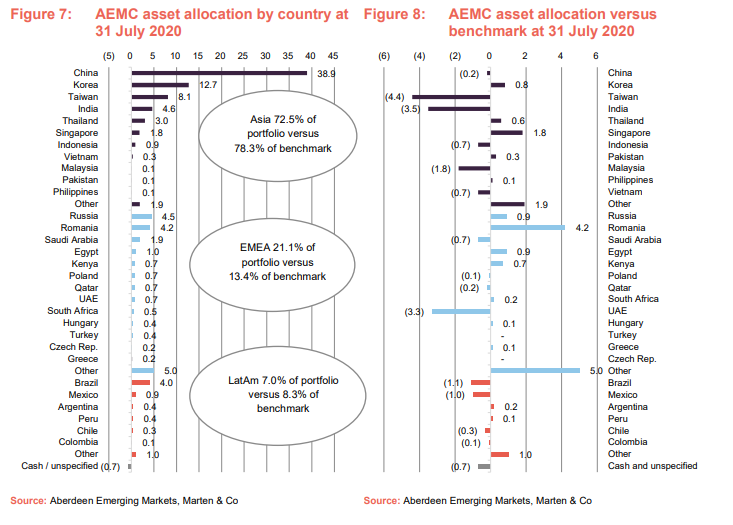

Since our most recent note, the managers of Aberdeen Emerging Markets Investment Company (AEMC) have significantly increased the fund’s exposure to China. With 38.9% of the fund now allocated to China and 72.5% to wider Asia-Pacific, extensive exposure is provided to the region that has been the quickest to return to near-normal economic activity. Asian exposure is supplemented by pockets of strength elsewhere, such as in Romanian equities and frontier market bonds. AEMC continues to trade at what seems an excessively wide discount to its peer group, particularly when also factoring in its dividend yield and low ongoing charges.

Earlier in the year, the managers took advantage of the attractive discounts provided by the initial sell-off in stocks to increase holdings in closed-end funds. They believe that emerging markets are attractively priced, with value stocks providing great scope for mean reversion.

Aims for consistent outperformance of MSCI Emerging Markets Index

AEMC invests in a carefully-selected portfolio of both closed- and open-ended funds, providing diversified exposure to emerging economies. It aims to achieve consistent returns for its shareholders above the MSCI Emerging Markets Net Total Return Index in sterling terms.

| wdt_ID | Year ended | Share price total return (%) | NAV total return (%) | MSCI EM total return (%) | MSCI World total return (%) |

|---|---|---|---|---|---|

| 1 | 31 Aug 2016 | 26.40 | 33.00 | 31.80 | 26.00 |

| 2 | 31 Aug 2017 | 29.90 | 23.40 | 27.00 | 18.80 |

| 3 | 31 Aug 2018 | -5.80 | -5.10 | -1.20 | 12.70 |

| 4 | 31 Aug 2019 | 6.80 | 7.10 | 2.50 | 7.60 |

| 5 | 31 Aug 2020 | 1.20 | 3.60 | 4.50 | 6.80 |

Emerging markets flattered by China’s resilience

For investors in emerging markets (EMs), 2020 has at times seemed like a case of China, Taiwan, South Korea, and the rest. Market returns have been heavily influenced by perceived successes and failures by governments in combating the virus’s spread. Spurred by memories of the experience of 2003’s SARS outbreak, the early all-in response efforts of a cluster of Southeast and East Asian countries, led by China, paid off, allowing economic activity to return to near-normal levels within a few months.

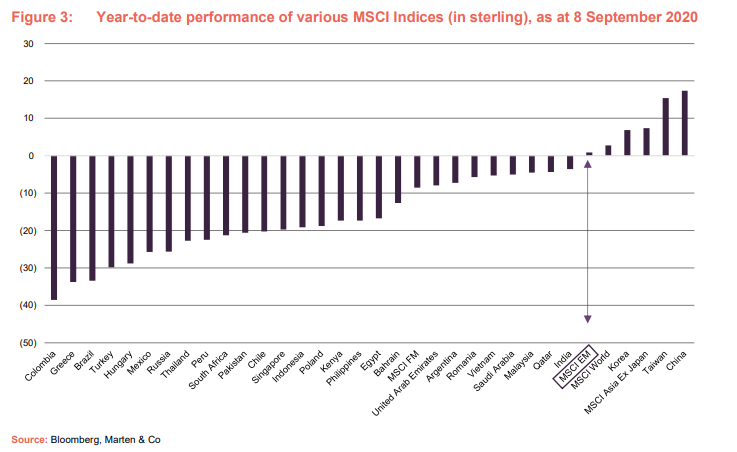

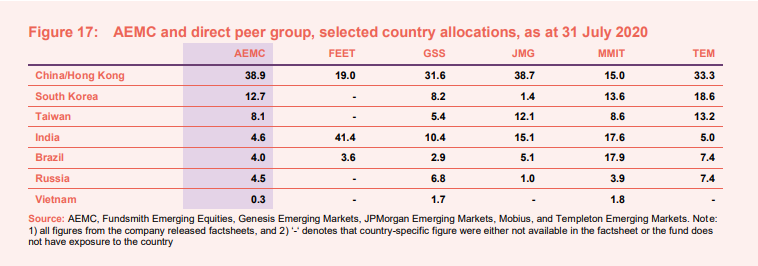

The fact that AEMC’s benchmark, the MSCI Emerging Markets Index, is in positive territory over the year-to-date is owed to China’s weight of over 40% and the market’s strong performance. Its domestic A-share market (publicly listed Chinese companies traded on the Shanghai and Shenzen stock exchanges) is having a particularly strong year, led by technology, consumer, and healthcare companies, and pushed on by the government’s encouragement of stock buying. As we discuss on page 5, AEMC’s managers have significantly increased the fund’s exposure to China, since our last note was published in February. The fund now has the highest absolute exposure to China within its peer group.

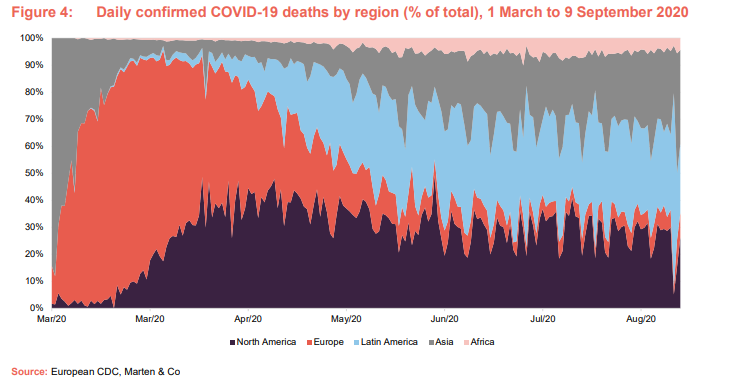

Figures 3 and 4 illustrate how challenging this period has been for Latin America, with the region accounting for the greatest loss of life over recent weeks. Brazil’s statistics agency, IBGE, announced on 1 September that the economy contracted by 9.7% over the second quarter, effectively taking the economy back to its size in 2009.

India, which represents a significant country allocation for several funds within AEMC’s peer group (see page 13), is struggling to contain the virus’s spread. Cases continue to proliferate for largely socioeconomic reasons, such as extreme population density in poorer areas. Mortality rates have remained low, given the population’s young profile. India’s economy contracted by 23.9% on a year-on-year basis, over the three months to 30 June, following Prime Minister Modi’s severe initial lockdown. Shutting down the economy was unsustainable, as debates over ‘lives versus livelihoods’ grew, while the economic spending response has underwhelmed many observers. The economic impact has been compounded by the fact that consumer demand was still in the early stages of a recovery following a banking sector liquidity squeeze, which made it difficult for many companies to access credit.

Compared to developed markets, AEMC’s managers note that whilst stimulus measures adopted in developed markets (12–25% of GDP) have dwarfed those in emerging markets (1–5% of GDP), demographics have favoured emerging and frontier markets.

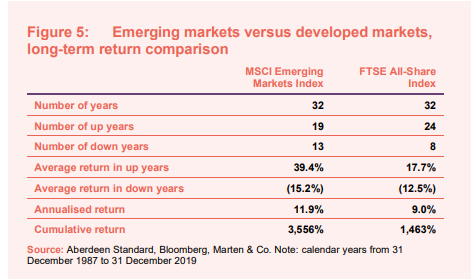

EMs significantly outperform over the long-term

The managers note that emerging markets have historically outperformed over the long term. Figure 5 illustrates that while AEMC’s benchmark has fewer ‘up’ years, the returns generated in these years tend to be substantial.

Asset allocation

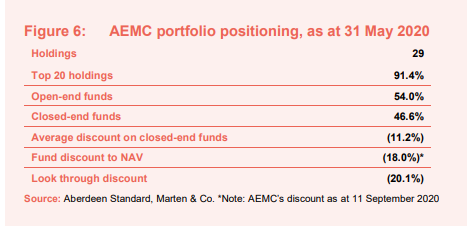

As of 31 July 2020, AEMC’s portfolio consisted of 29 fund investments, with the most recently available split between open- and closed-end structures illustrated by Figure 6.

Markets across the Asia Pacific region have largely been performing well, with effective country responses to COVID-19 shaped by the muscle memory of the SARS-CoV outbreak in 2003.

Since we last published in February, AEMC’s relative allocation to the Asia Pacific region compared to that of its benchmark has increased significantly from a (9.7%) underweight to (5.8%). In absolute terms, AEMC’s exposure to the region has increased by 8.6% to 72.5% of the portfolio. This has been driven by China, where the absolute weight increased by 10.6%.

The recent addition to the portfolio of Neuberger Berman – China Bond, discussed on page 9, has all but eradicated AEMC’s underweight exposure to China, compared to its benchmark. The managers note that China’s weight within the benchmark makes it very difficult for an emerging market fund to have an overweight allocation.

India has been less fortunate, as it continues to struggle to stem the tide of new cases. COVID-19 struck just as India was beginning to show signs of emerging from a liquidity squeeze that lasted over two years following the default by IL&FS, one of its largest infrastructure lenders.

Weakness in Latin America and the Europe, the Middle East, and Africa (EMEA) regions, where the peak of the pandemic’s first wave has been arriving later, has reduced their respective weights. Some pockets of strength have emerged, with dollar pegs (keeping the exchange rate at a fixed level to the US dollar) proving valuable to the Gulf economies, at a time when currency movements are exerting considerable influence on sterling returns. Within emerging Europe, Romanian investments performed well, with foreign fund inflows and a stable currency supporting returns delivered by the Fondul Proprietatea GDR holding.

Compared to its benchmark, AEMC provides more exposure to smaller emerging and frontier markets. The fund has comparatively lower exposure to Taiwan, India, South Africa, Malaysia, and Mexico. It has a comparatively higher exposure to Romania, Singapore, Russia, and several frontier markets through a bond fund. Frontier bond markets have performed resiliently this year, significantly outperforming equities. The allocation to frontier bonds represents an off-benchmark exposure.

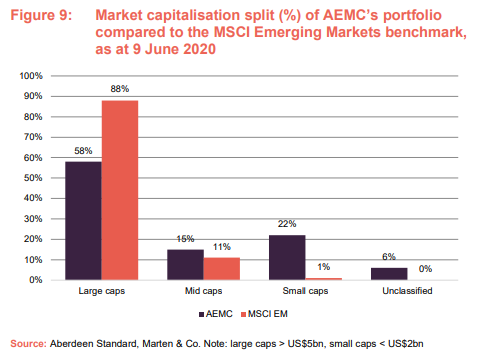

In terms of the relative market capitalisation size distribution of AEMC’s portfolio has a bias towards smaller companies with market capitalisations below $2bn. This is illustrated above by Figure 9.

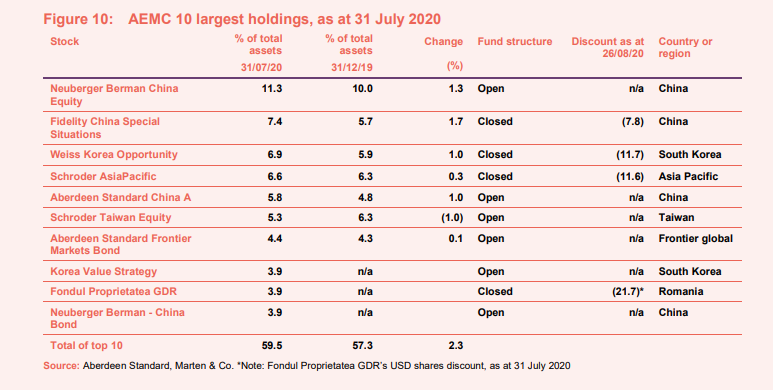

Largest holdings

Since we last published, Brown Advisory Latin America, Avaron Emerging Europe and DGC QIC Equity Fund have dropped out of the top 10. The open-ended funds, Brown Advisory Latin America and Schroder Taiwanese Equity, were sold as part of asset allocation adjustments made in the period following the pandemic’s onset. Elsewhere, Colombia moved down the list of largest Latin American exposures after the managers sold the Colombia exchange-traded fund (ETF) holding.

Fidelity China Special Situations has moved up the list, pushed on by its large allocation to Tencent and Alibaba, which between them make up around a fifth of its portfolio. Weiss Korea Opportunity’s shares are up by around 25% over the year-to-date. Though COVID-19 cases have been increasing in South Korea over recent weeks, it demonstrated an ability to respond decisively earlier in the year. Having initially performed short of expectations, the Weiss Korea holding has turned a corner since our last note. The holding in LG Chem, at about 10% of the portfolio, is having a particularly good year, with its shares more than doubling. It supplies batteries to Tesla.

Portfolio additions led by July addition of Neuberger Berman China Bond Fund

Over July, the managers increased AEMC’s exposure to China by adding the Neuberger Berman China Bond Fund (NB China Bond Fund). China is viewed favourably from a top-down perspective. The decision to use a lower-risk fixed-income instrument to increase the exposure to China was guided by the managers being mindful of the concentration risk of having nearly 39% of AEMC’s assets invested in one country. It is noted that China’s bond market is large (around $14trn), highly liquid, and significantly less volatile than the equity market. The NB China Bond Fund targets returns of 300 basis points (3%) over three-month China Government bonds from a diverse universe of corporate and sovereign bonds. The managers say that this should equate to a return of 5-7% per annum. The investment was funded partly by borrowing and the sale of part of the holding in Aberdeen Standard Frontier Markets Bond, which has proven resilient so far in 2020. Over July, the managers also topped up the holding in JPMorgan Global Emerging Markets Income, at what was considered an attractive discount level.

Earlier in 2020, the managers added to Aberdeen Asian Income and Aberdeen New India (also recently topped up), both of which are managed in-house. As of 31 May 2020, in-house funds represented 20% of AEMC’s NAV, an increase from the beginning of the year. Exposure to Schroder Oriental Income, was also increased.

Having more of the portfolio managed in-house reduces AEMC’s ongoing charges, as there is no second layer of fees on such investments. The closed-end structure also provided the managers with an opportunity to take advantage of the considerable widening in the discounts of funds over the early pandemic period particularly.

Performance

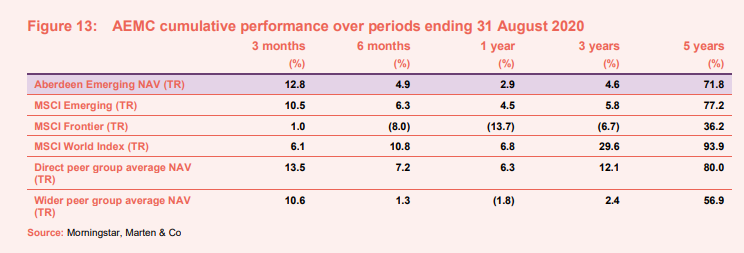

Good relative performance since May has led to AEMC slightly outperforming the MSCI Emerging Markets Index over the year-to-date, to 31 August 2020. AEMC has outperformed its wider peer group (defined below) over the long term, though it has been outperformed by the direct peer group.

The direct peer-group used in Figure 13 is comprised of the average performance of Fundsmith Emerging Equities, Genesis Emerging Markets, JPMorgan Emerging Markets, Mobius Investment Trust and Templeton Emerging Markets. These funds’ investment objectives closely resemble those of AEMC.

The wider peer group comprises all the funds in the AIC’s global emerging markets sector, excluding Africa Opportunity, Gulf Investment Fund and Qannas, which are not global funds; and Ashmore Global Opportunities, which is in the process of liquidating its portfolio.

Performance drivers

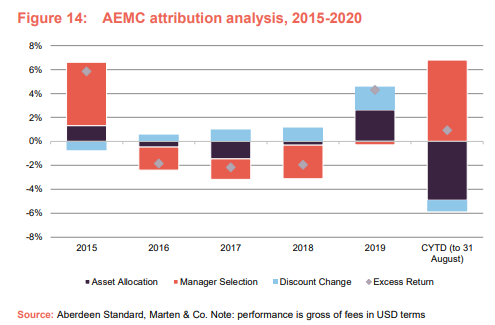

AEMC’s managers have provided a five-year performance attribution breakdown, inclusive of the year-to-date. As illustrated by Figure 14, over the year-to-date to 31 August 2020, the selection of managers has positively contributed to returns, while asset allocation and a widening in the discounts of closed-end funds held detracted.

Peer comparison

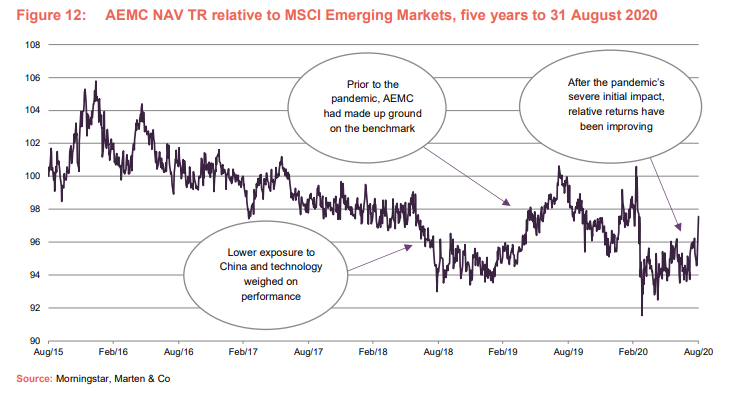

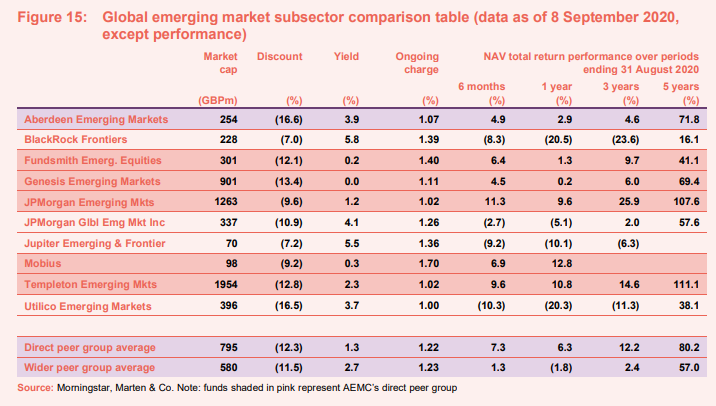

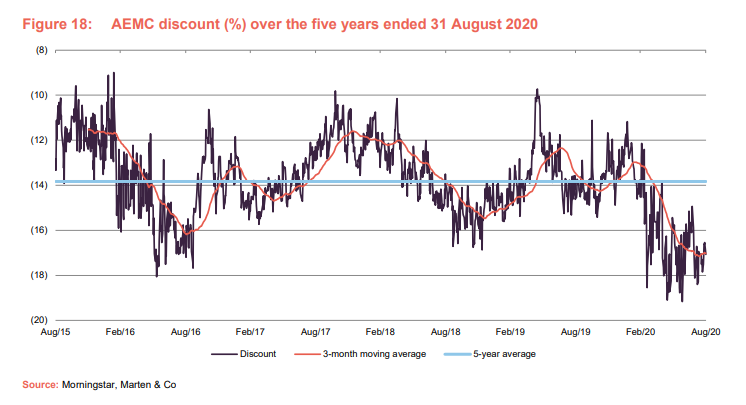

Compared to its wider and direct peer groups, AEMC’s discount appears excessively wide, particularly given its attractive dividend, a significant increase in its exposure to China over recent months, and a low ongoing charges ratio.

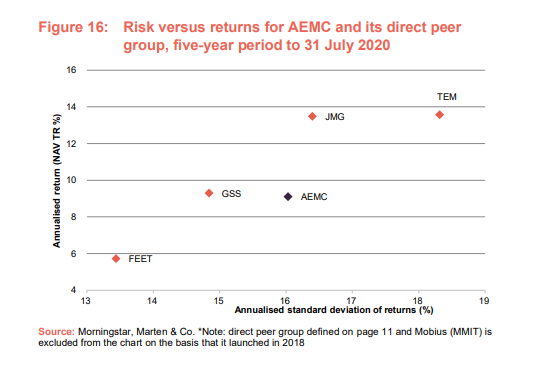

AEMC’s annualised five-year NAV returns and the volatility incurred in their generation are shown in Figure 16. Within the direct peer group, JPMorgan Emerging Markets and Templeton Emerging Markets led returns over the five years to 31 July 2020. AEMC’s underweight allocations to China, the technology sector, and corresponding overweights to smaller companies, were key detractors to returns over 2017 and 2018.

As of 31 July 2020, following portfolio additions discussed in the asset allocation section, AEMC’s allocation to China is now the highest within its direct peer group. It also has the lowest exposure to India. Between them, investments in China, South Korea, and Taiwan-focused funds amounted to 59.7% of AEMC’s portfolio weight, as at 31 July 2020 – the equivalent figure as at 31 December 2019, the date used in our most recent annual overview note, was 46.6%.

Premium/(discount)

Over the year ended 31 August 2020, AEMC’s discount moved within a range of (19.2%) and (11.1%) and, as at 11 September 2020, it was at (18.0%).

For details on AEMC’s share buyback powers, please refer to page 13 of our most recent annual overview note.

Catalysts for a narrowing in the discount could come from an improvement in sentiment towards emerging market stocks, a response to the asset allocation decisions made by AEMC’s managers to double-down on the trust’s Asia-Pacific focus, and the relative value opportunity presented by AEMC’s discount to its peer group.

Fund profile

AEMC provides investors with a one-stop-solution to a range of ‘best-of-breed’ emerging and frontier market managers, many of whom are inaccessible for most UK-based investors. These managers are investing in some of the most dynamic and fast-growing countries in the world. Investments are made through both closed- and open-ended funds, blending liquidity and access to a wider range of managers with the opportunity to add value through discount contraction.

Whilst benchmarked against the MSCI Emerging Markets Index, AEMC’s asset allocation may differ markedly from the benchmark and is one source of alpha generation. Manager selection is also key to the success of the fund. The ability to add value from narrowing discounts and corporate actions in the closed-end fund holdings is another source of alpha (excess returns over those of the benchmark index). The fund also offers a dividend yield of 3.9% (at the time of publication), which is paid quarterly from a combination of income and capital.

Management Team

AEMC’s AIFM is Aberdeen Standard Fund Managers Limited (Aberdeen Standard) and it has delegated the investment management of the company to Aberdeen Asset Managers Limited (AAML). Both companies are wholly-owned subsidiaries of Standard Life Aberdeen Plc.

Andrew Lister and Bernard Moody (the managers) have been the lead managers of the fund since 30 June 2014. They have been involved with the management of the fund since October 2000 and August 2006, respectively. They are assisted by Samir Shah and Omar Ene (collectively, the team). All of the senior members of the team have personal investments in the fund. Aberdeen Standard has considerable depth of investment management and analytical resource, in both emerging market equity and debt.

The team is now working closely with members of Aberdeen Standard’s multi-asset investing team, including Alistair Veitch, Margaret Ismond and Chris Paine. They provide inputs into the asset allocation decisions.

Previous publications

Readers interested in further information about AEMC may wish to read our earlier notes. You can read the notes by clicking on the links below:

- Access to a wealth of talent – initiation

- 10.6% a year for ten years – update

- A reversal of fortune – annual overview

- Focused on returns – annual overview

The legal bit

Marten & Co (which is authorised and regulated by the Financial Conduct Authority) was paid to produce this note on Aberdeen Emerging Markets Investment Company.

This note is for information purposes only and is not intended to encourage the reader to deal in the security or securities mentioned within it.

Marten & Co is not authorised to give advice to retail clients. The research does not have regard to the specific investment objectives financial situation and needs of any specific person who may receive it.

The analysts who prepared this note are not constrained from dealing ahead of it but, in practice, and in accordance with our internal code of good conduct, will refrain from doing so for the period from which they first obtained the information necessary to prepare the note until one month after the note’s publication. Nevertheless, they may have an interest in any of the securities mentioned within this note.

This note has been compiled from publicly available information. This note is not directed at any person in any jurisdiction where (by reason of that person’s nationality, residence or otherwise) the publication or availability of this note is prohibited.

Accuracy of Content: Whilst Marten & Co uses reasonable efforts to obtain information from sources which we believe to be reliable and to ensure that the information in this note is up to date and accurate, we make no representation or warranty that the information contained in this note is accurate, reliable or complete. The information contained in this note is provided by Marten & Co for personal use and information purposes generally. You are solely liable for any use you may make of this information. The information is inherently subject to change without notice and may become outdated. You, therefore, should verify any information obtained from this note before you use it.

No Advice: Nothing contained in this note constitutes or should be construed to constitute investment, legal, tax or other advice.

No Representation or Warranty: No representation, warranty or guarantee of any kind, express or implied is given by Marten & Co in respect of any information contained on this note.

Exclusion of Liability: To the fullest extent allowed by law, Marten & Co shall not be liable for any direct or indirect losses, damages, costs or expenses incurred or suffered by you arising out or in connection with the access to, use of or reliance on any information contained on this note. In no circumstance shall Marten & Co and its employees have any liability for consequential or special damages.

Governing Law and Jurisdiction: These terms and conditions and all matters connected with them, are governed by the laws of England and Wales and shall be subject to the exclusive jurisdiction of the English courts. If you access this note from outside the UK, you are responsible for ensuring compliance with any local laws relating to access.

No information contained in this note shall form the basis of, or be relied upon in connection with, any offer or commitment whatsoever in any jurisdiction.

Investment Performance Information: Please remember that past performance is not necessarily a guide to the future and that the value of shares and the income from them can go down as well as up. Exchange rates may also cause the value of underlying overseas investments to go down as well as up. Marten & Co may write on companies that use gearing in a number of forms that can increase volatility and, in some cases, to a complete loss of an investment.