JLEN Environmental Assets – Increasingly diversified as green-led recovery looms

Increasingly diversified as green-led recovery looms

JLEN Environmental Assets (JLEN) holds the most diversified portfolio within its peer group. Today, it is asking shareholders to approve a broader definition of environmental assets as well as increased exposure to construction-stage investments. We think that JLEN’s premium, which is one of the highest within its group of competing funds, reflects the breadth of its asset mix and the accompanying high proportions of income from government-backed subsidies, which makes its income more predictable.

The pace of decarbonisation (reducing the production of greenhouse gases including CO2 from the economy) in the UK and wider continental Europe, where JLEN is exploring opportunities, is set to ramp up, particularly with many governments looking to the ‘green economy’ to play a significant role in the post-COVID recovery. JLEN is well-positioned to take advantage of this.

Progressive dividend from investment in environmental infrastructure assets

JLEN aims to provide its shareholders with a sustainable, progressive dividend, paid quarterly. It also aims to preserve the capital value of its portfolio on a real basis over the long term. It invests in environmental infrastructure assets with predictable, wholly or partially index-linked cash flows, supported by long-term contracts or stable regulatory frameworks.

Premiums across the sector have risen through much of 2020. While equity income funds have been strained by dividend cuts, the renewable energy sector’s high degree of government-backed revenue provides a compelling alternative.

JLEN’s premium/(discount) largely moved in lockstep with the average of the AIC’s renewable energy infrastructure sector until mid-2019. However, JLEN’s shares have built up a significant premium to the peer group since.

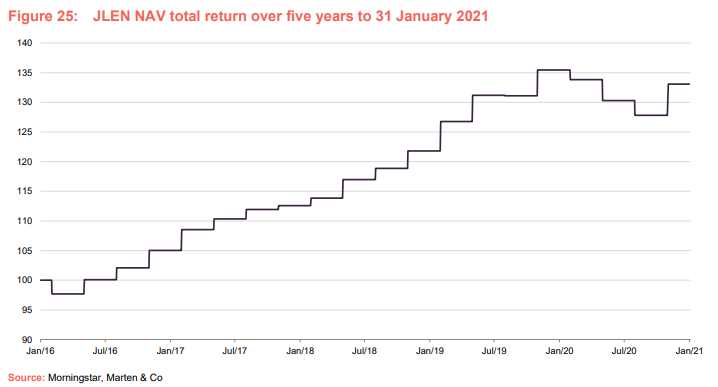

JLEN’s NAV performance has been fairly consistent, with no significant decline in the value of the portfolio over the past five years until the pandemic-inflicted impact on valuation last year.

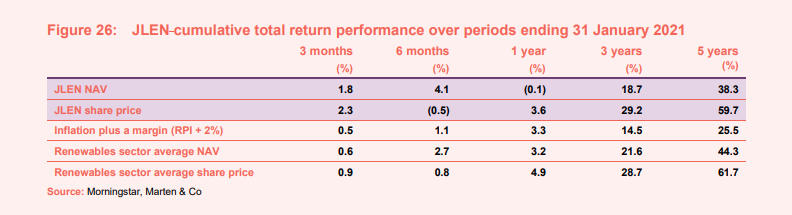

Over the five years to 31 January 2021, JLEN delivered total NAV and share price returns of 38.3% and 59.7%, equivalent to annualised total returns of 6.7% and 9.8%. NAV and price returns have been well ahead of inflation.

|

|

Broader definition of environmental infrastructure

On 16 February 2021, JLEN announced that it hopes to broaden the definition of what it is allowed to invest in. Shareholders will need to approve the change.

Under the planned revised investment policy, the company will continue to seek to achieve its investment objective by investing in a diversified portfolio of environmental infrastructure. However, the definition of environmental infrastructure for these purposes would be expanded to include a wider pool of prospective investments, including infrastructure assets, projects and asset-backed businesses that utilise natural or waste resources or support more environmentally friendly approaches to economic activity, support the transition to a low carbon economy or which mitigate the effects of climate change.

Sectors that fit within the revised definition of environmental infrastructure include, but are not limited to:

- Battery storage projects;

- Businesses which provide support services to core environmental

infrastructure projects; - Low carbon agriculture, including vertical farming assets (where plants are grown in vertically-stacked layers);

- Connecting infrastructure such as district heating (where heat from a central facility is distributed across a neighbourhood), and other core infrastructure used by environmental assets;

- Agriculture/bioenergy supply chain businesses serving anaerobic digestion plants and other bioenergy technologies which rely heavily on the upstream feedstock supply chain (which we take to mean biofuels); and

- Low carbon transport infrastructure such as electric vehicle charging

infrastructure.

Investment in member states of the European Union which are not members of the OECD

The company’s existing investment policy expressly prohibits it from investing in projects which are located in countries other than those which are members of the OECD. The revised investment policy would, if approved by shareholders, allow the company to invest in member states of the European Union which are not members of the OECD.

By our reckoning, this means: Albania, Armenia, Azerbaijan, Belarus, Bosnia & Herzegovina, Bulgaria, Croatia, Czech Republic, Estonia, Georgia, Hungary, Latvia, Lithuania, Moldova, Montenegro, Kosovo, North Macedonia, Poland, Romania, Russia, Serbia and, Slovak Republic, Turkey and Ukraine.

The company still expects to continue to have a significant majority invested in the UK and OECD countries, with at least half of the portfolio (by value) being based in the UK.

More in construction projects

Currently, there is a limit of 15% of NAV attributable to projects which are in

construction and are not yet fully operational (at the time of investment).

Shareholders are being asked to increase this limit to 25%. An increased exposure to construction-stage projects could offer opportunities to enhance returns for shareholders.

Accelerated decarbonisation

The UK’s commitment to net zero carbon emissions by 2050 is enshrined in law. Over the months and years to follow, the government will increase its support for decarbonisation, as a cornerstone of wider efforts to stimulate an economy facing its deepest recession in more than a generation. Prime Minister Boris Johnson’s ‘green recovery’ plan, unveiled in November 2020, will mobilise £12bn of state investment to incentivise asset growth within renewables.

Foresight notes that within the UK, a recent Government announcement to support up to double the capacity of renewable energy in the next contracts for difference auction, opening in late 2021, demonstrates the commitment to this sector. Whilst offshore wind is at the heart of this near-term strategy, an important contribution will come from other sectors. Renewed subsidy support will provide the revenue generation visibility needed to attract the required levels of capital to finance the buildout of capacity across technologies, new and old.

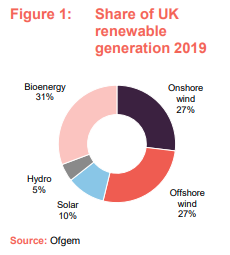

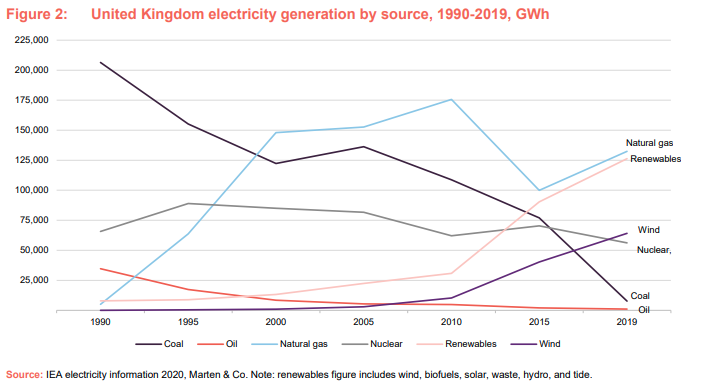

The 2020s will define the pathways towards decarbonisation, with the core generation technologies of wind and solar augmented by important contributions from other clean energy sources such as those produced by hydro and anaerobic digestion processes. The evolution of fossil fuel-led and renewable generation in the UK is illustrated by Figures 1 and 2.

JLEN is unique within its peer group in holding environmental assets such as anaerobic digestion, water, and waste projects. Anaerobic digestion has been the main focus of growth over recent times (see the asset allocation section), with Foresight believing it provides a better risk-adjusted return proposition than the crowded wind and solar spaces.

Support for anaerobic digestion is set to increase with increased biomethane (or renewable natural gas) production a target for the UK government. A Green Gas Support Scheme will launch in autumn 2021, with a four-year lifespan. It will support the deployment of additional anaerobic digestion plants, suggesting that the amount of biomethane in the gas grid could treble between 2018 and 2030. Furthermore, a decision has also been made to extend the existing Domestic Renewable Heat Incentive (RHI) support for domestic heat projects to March 2022. The non-domestic scheme will close to new applications from April 2021.

Foresight is not targeting a specific technology mix in continuing to expand into the more niche areas of renewables and environmental assets. The focus, rather, is to pursue further diversification.

Assessing further eco-friendly opportunities and Europe growth

Though the UK accounts for 98% of JLEN’s portfolio, its investment mandate allows up to 50% to be invested in other OECD countries. JLEN is expected to make greater use of this through increased investment into continental Europe, where Foresight has a strong in-country presence across the region. Over the past year, JLEN has partnered with Foresight to invest in a construction-stage Swedish wind farm and an operational Spanish wind farm. Construction-stage assets are not an area JLEN has engaged much with historically.

The investment adviser notes that 55% of the EU’s energy consumption will need to come from renewable sources by 2030, requiring some €400bn of investment. Increasing electrification of end-users will drive increased power demand to be met from renewable sources.

Whilst renewable energy generation remains JLEN’s primary focus, its most recent interim results report to 30 September 2020 noted that it was exploring eco-friendly opportunities in areas such as transport and low-carbon heat that have the revenue characteristics of infrastructure investments such as inflation-linked cash flows and stable revenues, reinforced by long-term contracts or regulatory support.

In December 2020, JLEN made its first investment into low-carbon transport by acquiring a minority stake in a portfolio of five compressed natural gas (CNG) refuelling stations for heavy goods vehicles (HGVs). The investment was made into CNG Foresight alongside other Foresight funds and CNG Fuels, the developer and operator of the project.

JLEN will also participate in a funding line to be deployed towards the build-out of a further pipeline of CNG refuelling stations. The fund’s total outlay, including the initial acquisition cost, is expected to be up to about £20m over the next two-to-five years.

JLEN diversifies further with CNG biomethane refuelling investment

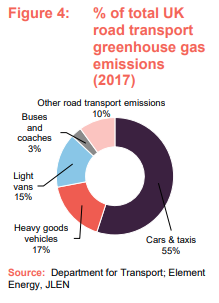

The UK emits 500 metric tonnes (Mt) of carbon dioxide per annum, of which the transport sector was responsible for 34% of CO2 emissions in 2019. Successfully re-shaping fuelling across transport will go some way towards clearing a path to net-zero emissions by 2050.

Whilst the adoption of electric passenger vehicles is accelerating, decarbonising HGVs poses particular challenges due to their long driving range, high payload, and low production volume. Within the transport sector, Foresight notes that HGVs account for 1.3% of vehicles on the road yet are responsible for 17% of road transport emissions and, 4.5% of total emissions. A breakdown of the relative emissions profile of UK road transport is displayed in Figure 4.

Biomethane (as generated by anaerobic digestion plants) provides the only currently proven, commercially viable solution, in the shape of CNG or liquefied natural gas (LNG), to address the UK’s HGV emissions problem. Biomethane is injected for transportation into the UK and EU gas grid network, where it is subsequently compressed and distributed at stations as 100% Bio-CNG offers some advantage over LNG, as we explain in the next section.

While biomethane is blended with fossil gas in the UK’s gas transmission network, an audit trail exists that allows HGV users to claim they are using biogas for fuel. This allows them to save on fuel duty (which, over time, offsets the cost of conversion to Bio-CNG). The opportunity is considerable.

According to Foresight, Bio-CNG’s financial and emissions benefits over diesel include:

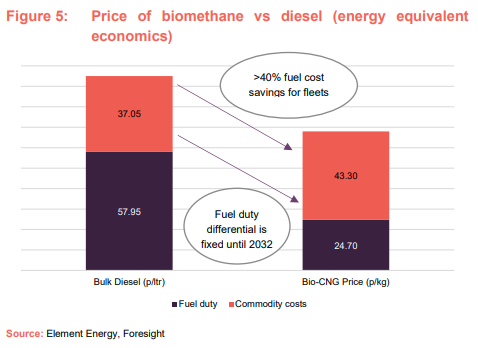

- Bio-CNG users have strong incentives locked in until 2032, natural gas fuel duty differential to diesel’s level is fixed at 1/3, meaning Bio-CNG vehicles have fuel costs that are more than 40% lower (illustrated by Figure 5);

- Lower lifetime costs and a 1-2 year payback for HGVs despite a £25,000 upfront premium today;

- Up to 85% emissions reduction using Bio-CNG; and

- 50% quieter vehicles.

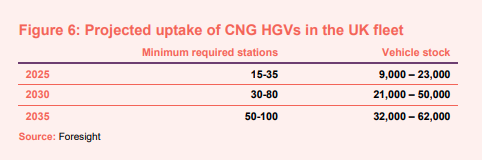

The forecast uptake of CNG-powered HGVs and the fuelling station requirement is shown in Figure 6. Foresight anticipates uptake of CNG vehicles will be material by 2025 and will continue to grow steadily to 2030. In their view, it will take at least another 10 years for the early adoption of zero-emission hydrogen-powered HGVs. Hydrogen is expected to provide a solution for HGVs in the long-term but the technological readiness is low.

By 2025, the early adopters of biomethane-fuelled fleets are projected to complete their first full replacement cycle. Improved and reliable gas-powered HGVs are being mass-manufactured by Scania, Iveco & Volvo.

CNG Fuels is the largest operator of public access CNG stations in the UK, with Foresight noting that it was responsible for 46% of all CNG & LNG volumes in the UK in 2019, with a customer base covering around 80% of the UK’s CNG fleets. CNG Foresight will be building out its station network substantially over the next two years with the target of more than doubling the current number of sites by 2023, to meet the forecast growth in the UK CNG vehicle fleet.

Advantages of CNG over LNG

It was thought that LNG would be favourable to CNG due to a longer HGV driving range for LNG. However, significant advances in CNG HGV models now allow for truck ranges in excess of 600km, which is considered appropriate for most fleets. CNG-powered HGVs now dominate the dedicated gas truck fleet market.

Some of the other advantages of CNG over LNG, discussed by Foresight, include:

- CNG is dispensed at ambient temperature while LNG requires temperatures of -160C;

- CNG stations provide a higher refuelling capacity;

- Operating costs for CNG are significantly lower as there is no need for road delivery to site. LNG is distributed to refuelling stations via road delivery while CNG is typically distributed through the pipeline by the gas grid network and compressed onsite;

- While the two have similar emissions savings based on recent tests, there is a greater risk of methane emissions from LNG due to boil-off from storage or fuel tanks; and

- There are established and proven markets for CNG for transport in the USA, which has 1,680 CNG stations and only 144 LNG stations, and similarly in Europe, which has 3,782 CNG stations compared to 270 LNG stations.

Investment process

Foresight has served as JLEN’s investment adviser since 1 July 2019 (see fund profile section). Projects are selected for the portfolio based on the advisers’ assessment of each project’s risk and reward profile. They operate within a limited set of investment restrictions. Asset expansion predominantly comes from investments in the secondary market from third parties.

The adviser aims to maintain the balanced and diverse nature of the portfolio. Their approach is a cautious one. Although JLEN can invest across all OECD countries, to date investments have focused predominantly on the UK. The advisers say that they prefer to concentrate on countries and regulatory/subsidy regimes that they know well or where they have relationships with established partners.

Investment restrictions

- No more than 15% of the portfolio is to be invested in assets under construction or that are not yet operational. The board does expect to see an increase in the allocation to construction-ready assets, within the 15% limit, following the commitment to Foresight Energy Infrastructure Partners (FEIP).

- At least 50% invested in the UK and the balance invested in other OECD countries.

- No new investment to exceed 30% of NAV (or 25% of NAV based on the acquisition price, taking the value of existing assets into consideration).

Purchases from third parties in the secondary market

The advisers have built up good working relationships with project developers. Some opportunities are brought to the adviser for appraisal by specialist consultancy firms operating in the area. Deals may also be introduced by the wider Foresight team.

Prices are negotiated at arms-length and reflect the advisers’ assessment of the potential risks and rewards from each project. This includes a review of the project’s capital structure.

Environmental, social and governance (ESG) assessment

Potential acquisitions are assessed on a range of metrics. These vary according to the sector and include aims to:

- avoid greenhouse gas emissions, where possible;

- substitute fossil fuel consumption with renewable energy and biofuels;

- minimise the disposal of waste to landfill; and

- maintain good relations with local stakeholders.

As part of this process, the advisers:

- review each project’s permits and compliance with operating licence requirements;

- review each project’s environmental management systems and the capabilities of the site’s managers; and

- commission an independent study to verify the positive environmental impact.

Ongoing management

The day-to-day facilities management, operations and maintenance of the projects is contracted to third parties and part of the adviser’s role is overseeing these arrangements, including approving payments.

The advisers seek to identify opportunities for efficiency enhancements and capacity increases.

The advisers also aim to optimise the company’s financial structure.

Disposals

JLEN will usually hold its assets for the long term, and no disposals have been made to date. It may, however, sell assets when the advisers feel the sale price justifies it or when there are other valid reasons for doing so. The directors may choose to return the proceeds of disposals to investors but may reinvest them.

Hedging

When they invest in assets in currencies other than sterling, the advisers may choose to hedge the currency exposure back to sterling. The advisers may also hedge interest rate risk, inflation risk, power, and commodity prices. All hedging is at the board’s discretion. The proportion of the portfolio assets with cash flows denominated in euros accounted for less than 1% of the portfolio value at 31 March 2020, the most recent year-end.

Sustainability

Climate change and issues of sustainability are pressing long-term challenges. The UK Government’s commitment to net-zero emissions by 2050 will require considerable investment in renewable energy and energy storage, as it seeks to cut carbon dioxide output associated with power generation.

JLEN’s investments sit at the heart of the solution to these problems. This has been recognised by the London Stock Exchange (LSE), which awarded JLEN its Green Economy Mark (recognising companies that derive more than half of their revenues from products and services that contribute to the green economy).

In our view, JLEN’s clear appeal to ESG focused investors is amongst the key factors behind the degree to which its shares trade at a premium to NAV (see the premium/(discount) section).

JLEN’s adviser, Foresight, is a signatory of the United Nations’ Principles for Responsible Investment (UNPRI) and ESG analysis is built into JLEN’s investment process, as described in the preceding section. It is also incorporated into the ongoing monitoring programme for JLEN’s portfolio.

Environmental performance 2019/2020

JLEN publishes ESG reports regularly, with the most recent annual report published in June 2020.

Over the six months to the end of September 2020, JLEN’s portfolio generated more than 450,000 megawatt hours (MWh) of clean energy, recycled more than 70,000 tonnes of waste, diverted around 240,000 tonnes of waste from landfill and treated more than 15bn litres of water.

Highlights from the financial year-end period to 31 March 2020 include:

- 900,000 MWh energy generated;

- 445,000 tonnes of waste diverted from landfill;

- >115,000 tonnes of waste recycled;

- 39bn litres of wastewater treated; and

- 245,000 tonnes of organic fertiliser produced

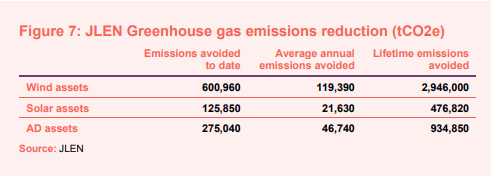

Aardvark Certification Ltd carries out an independent assessment of the environmental impact of JLEN’s assets. A summary of the most recent findings, published in JLEN’s June 2020 ESG report, are displayed in Figure 7.

Asset allocation

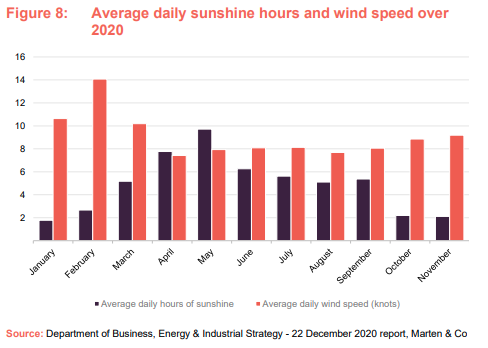

By having a wide spread of technologies, JLEN aims to reduce the portfolio’s volatility of returns. For example, as illustrated by Figure 8, wind has a complementary generation profile to solar, with peak electricity generation taking place at different times of the year.

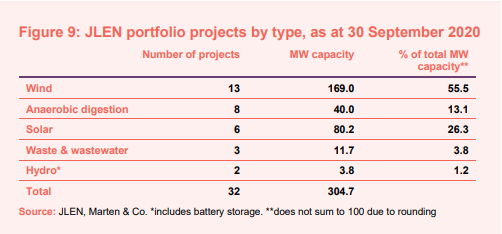

Figure 9 displays JLEN’s portfolio by project type, as at 30 September 2020. In aggregate, there were 32 projects spread across the wind, anaerobic digestion, solar, waste & wastewater, and hydro technologies.

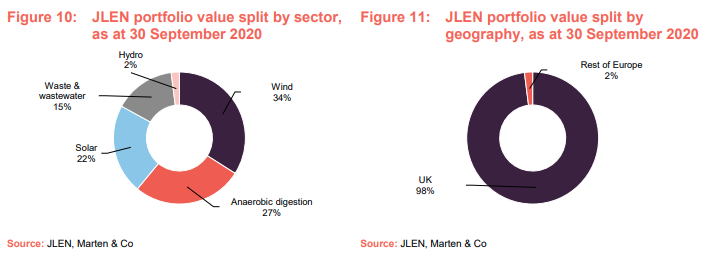

Changes in the asset split by value over 2020 reflect a natural widening in JLEN’s exposure to the anaerobic digestion and waste and wastewater technologies, in particular. Compared to portfolio figures from June 2019, used in our most recent annual note, wind and solar’s proportional contributions to portfolio value declined from 43% and 25%, to the 34% and 22% illustrated by Figure 10.

With respect to portfolio growth, on top of the December 2020 investment into compressed natural gas refuelling stations for HGVs, a further three projects having been added to the portfolio since our last note in May 2020. The additions of Peacehill Farm (anaerobic digestion) and Northern Hydropower (hydro and storage) pushed total capacity to 304.7MW, as at 30 September 2020. This was increased to 308.5MW, in February 2021, with the acquisition of Codford Biogas. Codford Biogas holds the rights and operational assets behind the Codford anaerobic digestion plant, a 100,000 tonnes per annum food waste plant, based in Wiltshire.

As with many of JLEN’s assets, Peacehill Farm and Northern Hydropower possess operational track records and revenue generation frameworks that are supported by a high proportion of inflation-linked cash flows that are backed by government subsidy programmes.

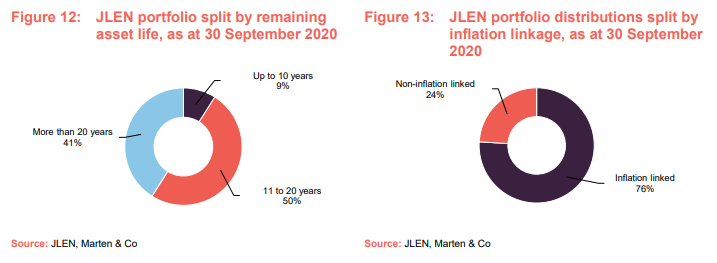

The weighted average remaining asset life of the portfolio is 18.9 years, with 91% of the portfolio having an asset life above 10 years, as represented by Figure 12. More than three-quarters of portfolio distributions were inflation-linked, as at 30 September 2020.

Wind

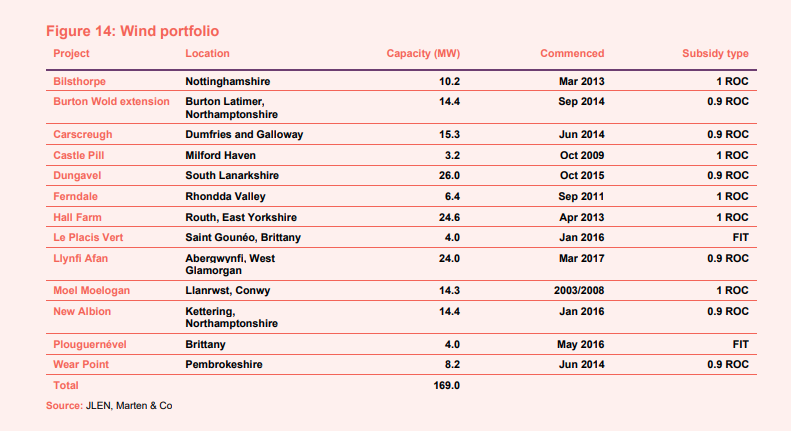

The composition of JLEN’s portfolio of UK onshore windfarms has remained unchanged since our last annual overview note. Each asset shown in Figure 14 is 100% owned by JLEN. The portfolio is located predominantly in the UK, with two small wind farms in Brittany, France.

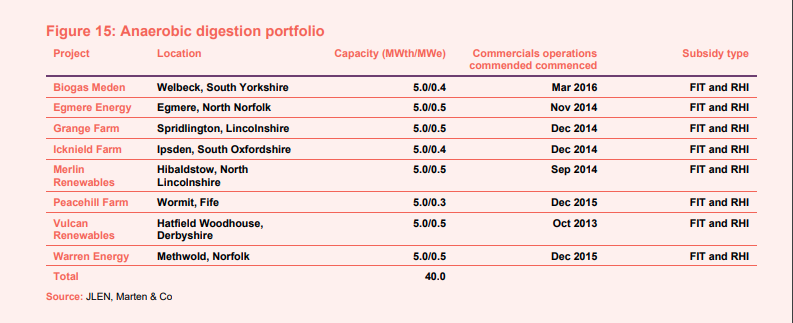

Anaerobic digestion

Anaerobic digestion has been the fastest-growing part of JLEN’s portfolio in recent years. The deal behind the recent acquisition of the Codford anaerobic digestion plant represented an initial outlay of £19.8m. The plant has been operational since 2014 and has a current capacity of 3.8MWe. JLEN notes that as a result of its electricity generation, the plant can supply up to 4,000 homes through the UK power grid. This acquisition is JLEN’s second in food waste fuelled anaerobic digestion.

Earlier in April 2020, Scotland-based Peacehill Farm was added to the portfolio. It is located on a poultry farm and fuelled, in part, by the manure generated by the farm. It predominantly produces biomethane to be injected into the national gas grid. Peacehill represented a c.£11m outlay and the plant is accredited under the RHI and FIT subsidy schemes. Unusually for JLEN, the investment includes a subscription for a minority equity stake – the vast majority of assets are 100% owned.

Several of JLEN’s anaerobic digestion plants are located in the Midlands. The proximity supports efficiencies around sourcing feedstock and servicing. Feedstock is responsible for around half of the operating costs of operating an anaerobic digestion facility.

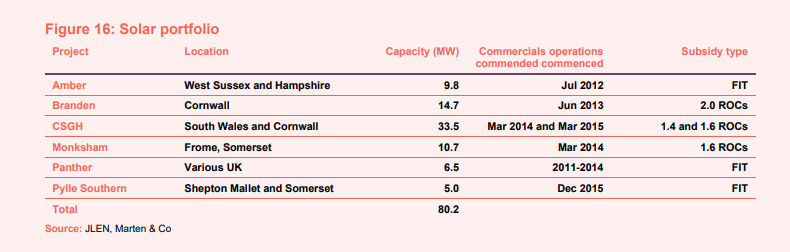

Solar

As with wind, there has been no change to the makeup of JLEN’s solar portfolio since we last published. Growth in aggregate UK solar capacity across the UK has slowed since 2017, as newly-commissioned solar projects were no longer eligible for government subsidies. In the secondary market, a finite supply of subsidy-qualifying projects commissioned before 2017 commanded a significant premium, reinforced by the arrival of considerable private capital attracted by government-backed revenues and the relatively low variance associated with solar irradiation.

Within JLEN’s solar portfolio, Amber operates across two locations, Branden operates across three locations and CSGH operates across four locations. Panther is a portfolio of smaller rooftop and ground-mounted schemes scattered across the UK mainland. All are 100% owned by JLEN. Over the financial year to 30 March 2020, life extensions were secured on five of the solar projects, and the investment adviser is exploring extensions on the remaining three.

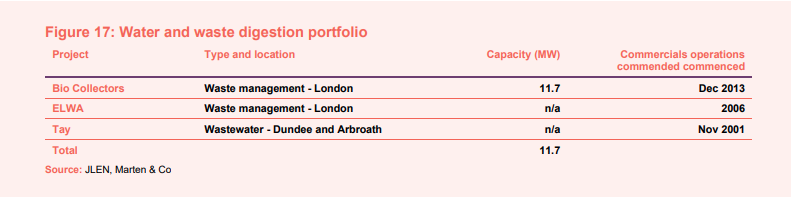

Waste & wastewater

Bio Collectors, JLEN’s first food waste collection and treatment plant project, processes around 100,000 tonnes of food waste each year, collected from around Greater London. The impact of COVID-19 has resulted in a reduction in food waste tonnages, with part of the asset’s food waste sourced from London’s hospitality and retail sector. This has resulted in a material impact on gas production.

Waste tonnage levels at the East London Waste Authority (ELWA) waste project remained above target over the most recent interim results period. The ELWA project processes around 440,000 tonnes of household waste each year from four London boroughs. Waste processing is performed through a combination of facilities constructed and developed as part of the project, the largest of which are two mechanical biological treatment facilities which produce recyclable material and solid recoverable fuel (delivered to waste facilities, primarily in the Netherlands, and burnt to produce heat, for district heating schemes, and energy, for export to the grid).

The Tay treatment plant benefitted from greater rainfall towards the end of the summer period, following a dry spring. Rainfall is a key driver of wastewater flows through the treatment plant.

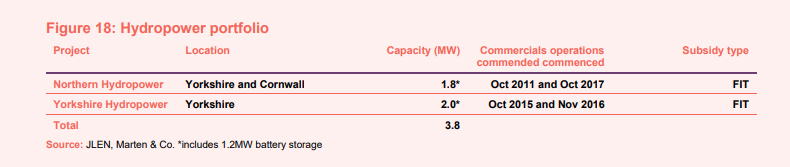

Hydro and battery storage

The addition of the Northern Hydropower project in September 2020, brought in two further hydropower assets for £4.7m, situated in Cornwall and Yorkshire. Run of the river hydro assets are relatively scarce and their limited availability means that these are unlikely to be a huge component of JLEN’s portfolio. They do, however, provide diversification benefits.

The Northern Hydropower’s Yorkshire asset includes a battery storage system (as does the Yorkshire Hydropower plant). Storage, which is undergoing rapid technological advancement, will form a vital part of the energy transformation away from fossil fuels, providing a solution to the challenge of intermittent generation, and ultimately further facilitating the ability of renewable energy to replace baseload capacity.

Foresight development fund providing European exposure

JLEN is permitted to have some exposure to construction-stage assets but has historically approached this cautiously. Foresight has greater experience of greenfield renewable energy investments and more resource dedicated to this area than JLEN’s previous investment adviser had. At the end of January 2020, JLEN’s board approved a €25m commitment to FEIP, a Luxembourg limited partnership investment vehicle.

The majority of the partnership’s investments will be in construction-stage European renewable energy generation infrastructure such as wind farms

and solar parks, and associated energy storage, transmission and distribution assets. The attraction for JLEN is the higher returns that construction stage assets can offer and the ability to further diversify its revenue. Investing through a fund allows JLEN to spread its construction risk over a wider range of assets than making direct investments would.

As at 30 September 2020, FEIP had invested into a construction-stage Swedish wind farm – Skaftåsen Vindkraft AB – and Torozos, an operational 94MW Spanish wind farm.

Portfolio valuation

JLEN publishes NAVs on a quarterly basis based on valuations prepared by the investment adviser. These are approved by the board prior to publication. There is no publicly quoted comparable price for the projects that JLEN invests in, and so the individual projects are valued on the basis of discounting the forecast cash flows over the life of each project at a rate that reflects market benchmarks and Foresight’s experience of bidding for assets.

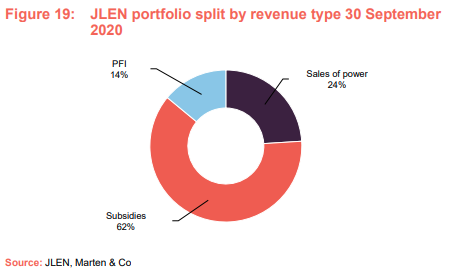

JLEN’s cash flows are fairly predictable, with close to two-thirds of revenue generation attributable to subsidies or contractual payments under public finance initiative (PFI) type contracts. The most recent split between regulated and non-regulated revenue is captured in Figure 19.

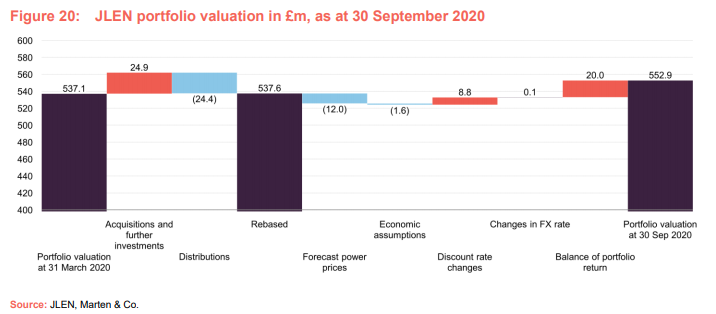

JLEN’s portfolio declined in value by 2.5% to £523.6m, over the six months to 30 September 2020. This was largely the result of the (£12m) impact from changes in the forecast power prices. A larger hit took place over the 31 March 2020 year-end, where the negative impact from lower power price forecasts had a (£56.9m) impact on valuation. Movements in the value of the portfolio over the most recent six-month period are displayed below in Figure 20.

Foresight says that it is not certain that power prices will recover to previously forecast levels. Moreover, as renewables assume a greater share of baseload capacity, the balance between supply and demand in energy markets will evolve.

We refer readers interested in a detailed discussion on the many moving parts involved in valuing the portfolio to our update note, published in May 2020, where valuation was a central theme. Beginning on page 5 of that note, the NAV’s relative sensitivity to key inputs, such as the discount rate employed to arrive at the present value of the portfolio cash flows and the relative impact of movements in electricity prices, were explored.

Performance

Operational performance – generation +2.5% above budget

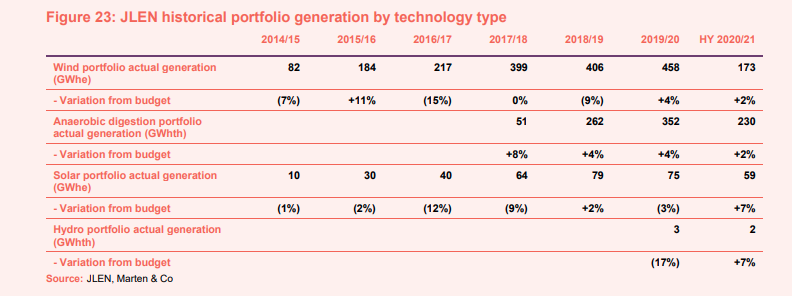

Over JLEN’s interim period to 30 September 2020, total energy generation (excluding the Bio Collectors food waste plant) was 463 gigawatt hours (GWh), +2.5% above budget. Generation from wind, solar and anaerobic digestion was above budget, as illustrated by Figure 23.

The anaerobic digestion portfolio, where generation was 1.8% ahead of budget, produced the most energy on a GWh basis, following the completion of the upgrade to double capacity at the Vulcan Renewables plant. Expansion activity is underway to increase capacity at the plant by a further 25–30%. Elsewhere, strong performance was delivered by Grange, Icknield, and the recently acquired, Peacehill.

The interim period saw wholesale gas prices drop close to their lowest levels in several years. JLEN attributes this to a mild winter, healthy stocks, and a further reduction in prices during the early months of COVID-19. The anaerobic digestion portfolio hedged gas prices with volume ranges from 50% to 80% going into winter 2020, next summer, and for some assets the hedges extend to the winter of 2021.

The wind portfolio took advantage of good wind availability, with a total production of 172GWh coming in at 2.1% above budget. Following a tender over the period, costs attributed to the technical wind asset management service have been reduced, while the breadth of the asset management contract has increased, which could lead to potential efficiency gains going forward.

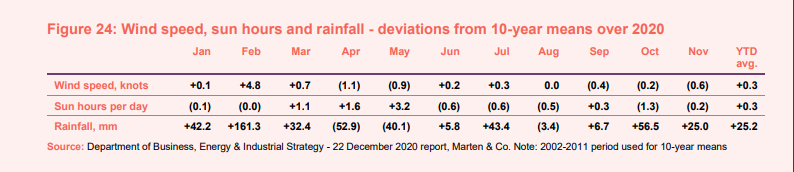

Generation from the solar portfolio was 6.7% above budget, benefitting from considerably higher than average irradiation over the spring months, as shown by Figure 24. Generation would have been 9.0% above budget were it not for a planned grid constraint in Shoals Hook from August to September.

The hydro portfolio generated 1.9GWh, coming in 7.4% ahead of budget. Availability throughout the period exceeded expectations. Output steadily increased from the end of May as rainfall increased, following what the investment adviser notes was the driest April-June period in recorded history.

Financial performance

Over the half-year period to 30 September 2020, JLEN’s NAV decreased by 1.4%, principally as a result of the lowering in long-term power and gas price forecasts.

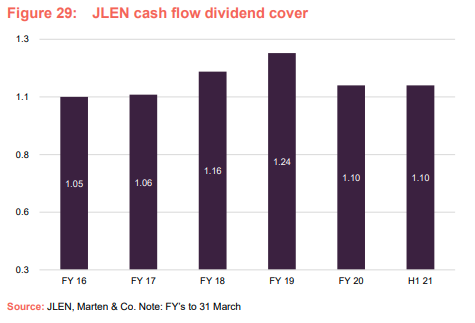

JLEN’s profit before tax over the interim period to 30 September 2020 was £10.7m, compared to £16.2m in 2019. Cash inflows from distributions increased to £24.4m, from £22.8m last year. The dividend continues to be well covered by cash flows, as we show in Figure 29.

Over the five years to 31 January 2021, JLEN delivered total NAV and share price returns of 38.3% and 59.7%, equivalent to annualised total returns of 6.7% and 9.8%. NAV and price returns have been well ahead of inflation (for comparison purposes we have used the retail prices index (RPI) +2% in Figure 26).

JLEN’s NAV performance has been consistent, with no significant decline in the value of the portfolio over the five years up until the pandemic-inflicted impact on valuation (see the valuation section).

Peer group comparison

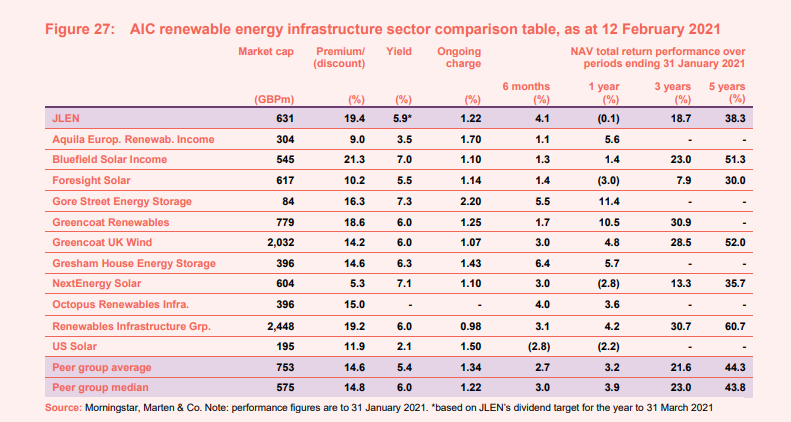

JLEN has the broadest remit amongst the 12 companies, displayed in Figure 27 below, that comprise the AIC’s renewable energy sector, excluding those funds focused on energy efficiency and two recent initial public offering (IPOs): Downing Renewables and Infrastructure and Ecofin US Renewables. It remains the only fund in the peer group to incorporate environmental infrastructure assets such as anaerobic digestion and water and waste projects within its portfolio. The peer group includes Foresight, NextEnergy, and US Solar, which are all pure solar funds, as is Bluefield for now – its mandate was expanded in 2020.

Greencoat Renewables and Greencoat UK Wind are focused on wind generation; Octopus Renewables Infrastructure has a particular focus on onshore wind and solar, and Aquila European Renewables Income also has a diverse portfolio that includes solar. The Renewables Infrastructure Group holds both wind and solar farms. Gore Street Energy Storage and Gresham House Energy Storage generate revenue from battery storage facilities.

Figure 27 compares the performance of the funds, as well as some structural differences. JLEN is one of six funds that were in existence five years ago. Each fund was trading on a premium to NAV, as at 12 February 2021, with JLEN’s being the second widest. JLEN’s ongoing charges ratio has been trending lower, and in absolute terms, appears competitive compared to similarly-sized funds, especially when factoring in the extra diversification provided by the broad remit.

Variations in performance across the peer group tend to reflect differences in asset composition. Wind-focused funds performed best over the past five years. In addition to the aforementioned Greencoat Renewables and Greencoat UK Wind, Renewables Infrastructure has a heavy wind focus, with a combination of onshore and offshore assets making up close to 90% of its portfolio mix. Solar has benefitted from a significant uptick in irradiation (the amount of energy received from the sun) over the peak months since 2018.

JLEN’s unique incorporation of environmental infrastructure assets means it is less vulnerable to a poor year of irradiation or weak wind generation than most of its peers. Technologies in which JLEN is actively expanding, such as anaerobic digestion and hydro, continue to benefit from a high proportion of inflation-linked cash flows that are backed by subsidies.

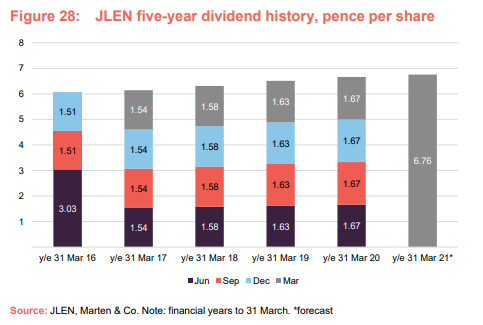

Dividend – moving away from inflation link

In June 2020, JLEN amended its dividend policy by breaking the explicit link with inflation. This will come into effect after the 31 March 2021 year-end. Going forward, JLEN will look to increase the dividend each year, without being tied to a formal inflation link. While JLEN has a relatively higher proportion of fixed revenues compared to many of its peers, it is not immune to the effects of lower power prices on portfolio revenue generation.

A dividend of 3.38 pence per share was declared for the six months to 30 September 2020 (six months to 30 September 2019: 3.33 pence). JLEN is targeting a full-year dividend of 6.76p, which would represent a 1.5% year-on-year increase. Based on a share price of 114.5p as at 12 February 2021, the shares were offering an attractive dividend yield of 5.9%.

In our view, cash flow dividend cover is a more valid measure than earnings cover for a fund such as JLEN, as it is less subjective. Figure 29 shows that dividend distributions have been covered by cash generated by the portfolio, net of running costs, over the past five years. For the most recent interim period to 30 September 2020, cash dividend cover was an impressive 1.1x. Whilst portfolio value declined over 2020 (see the portfolio valuation section), as a result of lower power price forecasts, the most recent cash flow dividend cover figures underline the defence provided by the protected revenues.

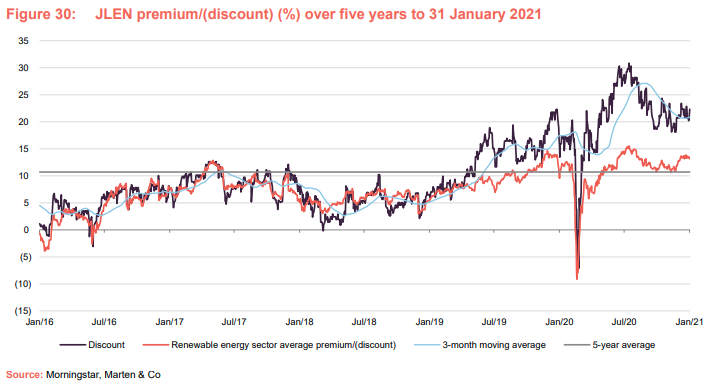

Premium/(discount) – scarcity of income

JLEN’s attractive yield, supported by a high proportion of protected revenues and the broadest remit of any fund within its peer group, has been especially appealing to investors in this environment. Premiums across the sector have risen through much of 2020, with the sector’s government-backed income sources providing a compelling yield alternative to traditional equity income investments that have come under strain as companies were forced to cut or suspend their dividends in the aftermath of the pandemic. JLEN’s conservative valuation inputs are also thought to have played a role in supporting the premium.

The continued growth of ESG investing, and a view that the government will likely look to renewables to play a key role in a post-COVID economic recovery, have also shaped sentiment.

Over the year to 31 January 2021, JLEN’s shares moved within a range of a 7.1% discount to a 30.9% premium. The swing to a discount was the result of early COVID-led volatility as investors liquidated equity investments. The average premium over the year was 20.7%.

As at 12 February 2021, JLEN was trading at a premium to NAV of 19.4%. JLEN’s premium/(discount) over the five years to 31 January 2021 largely moved in lockstep with the average of the AIC’s renewable energy infrastructure sector until mid-2019. JLEN’s shares have since built up a significant premium to the peer group.

Fees and costs

JLEN’s ongoing charges ratio for the year ended 31 March 2020 was 1.22%, down from 1.26% for the prior year. JLEN expects the full-year ratio to continue to decrease for the year to 31 March 2021.

The advisers are entitled to a base fee of 1% on the first £500m of adjusted portfolio value and 0.8% on the balance. The total adviser fee for the March 2020 year-end amounted to £5.50m. That sliding scale took effect during the year as the assets surpassed £500m for the first time. In addition, the growth of the company helps spread fixed costs over a wider base.

The adviser’s contract can be terminated on one year’s notice. There is no performance fee.

Directors’ fees and expenses totalled £253,000 for the last financial year. Other notable expenses were for administration services, provided by Praxis Fund Services Limited (£122,000), and for the auditors, Deloitte LLP (£112,000).

Capital structure

JLEN is domiciled in Guernsey and is listed on the main market of the London Stock Exchange. Investments are carried out through JLEN Environmental Assets Group (UK) Limited (UK Holdco), a subsidiary in which JLEN may own both equity and loan notes (a form of debt). As at 30 September 2020, JLEN had 546.7m ordinary shares in issue.

On 27 February 2020, JLEN raised £57.2m through the issue of 49.7m shares at 115p, in a significantly oversubscribed fundraise. The capital raised was mainly used to pay down amounts drawn with the revolving credit facility – effectively a bank overdraft – discussed in the following section. JLEN elected not to raise further capital from its shareholders over the rest of the year, as it is conscious of the performance effect cash held by the fund can have in the absence of immediate use for the capital.

JLEN has an indefinite life, but a discontinuation vote may be triggered if its shares trade at a discount for a prolonged period. The company’s financial year-end is 31 March and AGMs are typically held in August.

Gearing

Gearing (borrowing) is intrinsic to the investment models applied by JLEN and all its listed peers. Borrowing through the revolving credit facility is permitted at the fund level up to a maximum of 30% of net assets. As at 30 September 2020, drawings under this were £42.4m. As at 30 September 2020, £127.6m was undrawn. The facility, which matures in June 2022, is provided by HSBC, NIBC, ING and Santander.

The facility margin is 2.00–2.25% over LIBOR, depending on the fund’s loan-to-value ratio. Interest rate risk is hedged out using swaps. The facility has been extended to June 2022.

In addition to the revolving credit facility, the stable, predictable cash flows generated by the underlying projects make it easier to borrow money secured against them. At the project level, JLEN is constrained to a maximum of 65% gearing on gross project value for renewable energy generation projects and a maximum of 85% gearing on gross project value for PFI/PPP type projects. Actual project gearing is much lower than this. Across the portfolio, gearing was 29.6% at the end of September 2020, compared to 31.9% six months earlier. The 29.6% figure reflected a 25.5% level for the renewable energy assets and 51.8% for the PFI processing plants. Including the outstanding balance on the revolving credit facility, total gearing was 33.6% at 30 September 2020. Adding in the outstanding balance on the revolving credit facility results in an overall gearing level of 36%.

This project-level debt is non-recourse to the fund, meaning that it is secured by collateral, ensuring that shareholders are not exposed to the repayment risk that would be inherent to gearing at the fund-level.

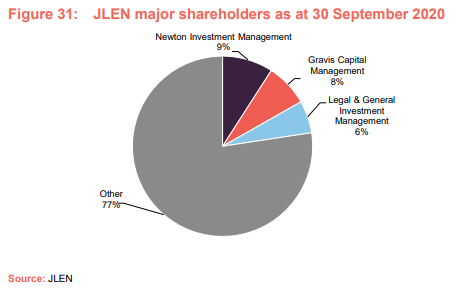

Major shareholders

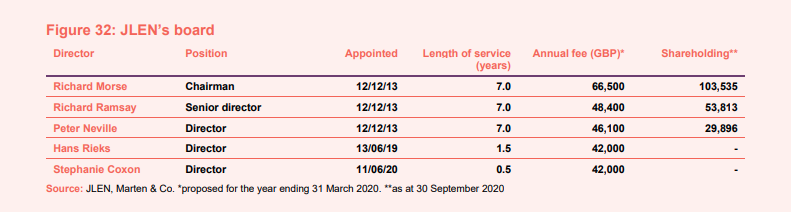

Board

The five directors are all non-executive and independent of the adviser. Denise Mileham, who served on the board from JLEN’s launch in 2014, stood down on 3 September 2020. Stephanie Coxon was appointed as Denise’s replacement, bringing with her 15 years of experience specialising in reporting accountant and audit services with PwC.

JLEN has been working through the process of board succession, with Stephanie’s appointment following on from that of Hans Joern Rieks in 2019. It is expected that more of the original directors are likely to be replaced by the ninth anniversary of the fund’s listing in 2023.

The bill for the total remuneration and benefits in kind payable to the directors is capped (within the Articles of the company) at £300,000 per annum.

Proposed changes to the company’s articles of association

Alongside the broader definition of what constitutes environmental assets, the circular convening the meeting to approve those changes also proposes some changes to the company’s articles of association.

Measures include:

An increase in the cap on directors’ pay from £300,000 to £400,000 per annum. The thinking is that this will make it easier to manage succession plans within the board, allowing a temporary increase in the overall number of directors, for example.

Remove the restrictions on:

- the majority of Directors being resident in the United Kingdom for tax

purposes; - board and committee meetings being held in the United Kingdom; and

- directors who are physically located in the United Kingdom participating in board and committee meetings.

The changes to the restrictions reflect a change in tax laws.

Fund profile

JLEN invests in infrastructure projects that use natural or waste resources or support more environmentally-friendly approaches to economic activity. This could involve the generation of renewable energy (including solar, wind, hydropower and biomass technologies), the supply and treatment of water, the treatment and processing of waste, and projects that promote energy efficiency. It aims to build a portfolio that is diversified both geographically and by type of environmental asset. This emphasis on diversification helps differentiate JLEN from its peers, which tend to specialise in solar or wind.

Reflecting its objective of delivering sustainable, inflation-linked dividends and preserving its capital, JLEN does not invest in new or experimental technology. A substantial proportion of its revenues is derived from long-term government subsidies.

Investment adviser

JLEN is advised by Foresight Group LLP. Foresight is one of the best-resourced investors in renewable infrastructure assets, with £6.5bn of assets under management. This includes Foresight Solar Fund, which sits in JLEN’s listed peer group. Foresight has a highly experienced global infrastructure team with 99 people. The co-lead advisers to JLEN are Chris Tanner and Chris Holmes.

Previous publications

Readers interested in further information about JLEN may wish to read our earlier notes. You can read the notes by clicking on the links.

Diverse renewables exposure, initiation note, September 2017

Anaerobic diversification, update, March 2018

Diversification benefits shine through, annual overview, September 2018

Life extensions to boost NAV?, update, March 2019

Battery storage potential, annual overview, September 2019

Reliable source of income, update, May 2020

The legal bit

Marten & Co (which is authorised and regulated by the Financial Conduct Authority) was paid to produce this note on JLEN Environmental Assets Group.

This note is for information purposes only and is not intended to encourage the reader to deal in the security or securities mentioned within it.

Marten & Co is not authorised to give advice to retail clients. The research does not have regard to the specific investment objectives financial situation and needs of any specific person who may receive it.

The analysts who prepared this note are not constrained from dealing ahead of it but, in practice, and in accordance with our internal code of good conduct, will refrain from doing so for the period from which they first obtained the information necessary to prepare the note until one month after the note’s publication. Nevertheless, they may have an interest in any of the securities mentioned within this note.

This note has been compiled from publicly available information. This note is not directed at any person in any jurisdiction where (by reason of that person’s nationality, residence or otherwise) the publication or availability of this note is prohibited.

Accuracy of Content: Whilst Marten & Co uses reasonable efforts to obtain information from sources which we believe to be reliable and to ensure that the information in this note is up to date and accurate, we make no representation or warranty that the information contained in this note is accurate, reliable or complete. The information contained in this note is provided by Marten & Co for personal use and information purposes generally. You are solely liable for any use you may make of this information. The information is inherently subject to change without notice and may become outdated. You, therefore, should verify any information obtained from this note before you use it.

No Advice: Nothing contained in this note constitutes or should be construed to constitute investment, legal, tax or other advice.

No Representation or Warranty: No representation, warranty or guarantee of any kind, express or implied is given by Marten & Co in respect of any information contained on this note.

Exclusion of Liability: To the fullest extent allowed by law, Marten & Co shall not be liable for any direct or indirect losses, damages, costs or expenses incurred or suffered by you arising out or in connection with the access to, use of or reliance on any information contained on this note. In no circumstance shall Marten & Co and its employees have any liability for consequential or special damages.

Governing Law and Jurisdiction: These terms and conditions and all matters connected with them, are governed by the laws of England and Wales and shall be subject to the exclusive jurisdiction of the English courts. If you access this note from outside the UK, you are responsible for ensuring compliance with any local laws relating to access.

No information contained in this note shall form the basis of, or be relied upon in connection with, any offer or commitment whatsoever in any jurisdiction.

Investment Performance Information: Please remember that past performance is not necessarily a guide to the future and that the value of shares and the income from them can go down as well as up. Exchange rates may also cause the value of underlying overseas investments to go down as well as up. Marten & Co may write on companies that use gearing in a number of forms that can increase volatility and, in some cases, to a complete loss of an investment.