Montanaro European Smaller Companies Trust – Impressive returns in difficult market

Impressive returns in difficult market

Montanaro European Smaller Companies (MTE) has generated impressive returns for investors over the past year and has outperformed its benchmark in four of the past five 12-month periods. The trust is ahead of both its benchmark and its peer group average by more than 80 percentage points over the five years ended 30 September 2020. The manager’s focus on high-quality and growing companies positioned MTE well when COVID-19 hit markets. The portfolio includes many innovative and promising businesses, some of which are beneficiaries of the shift to home working and investment in healthcare that the pandemic has fostered.

The trust’s impressive returns have attracted new investors, helping to eliminate its discount. It seems anomalous that MTE is the smallest of the European small-cap trusts. We believe the next step for MTE should be for it to expand by reissuing those shares that it holds in treasury where possible.

Continental European smaller companies

MTE aims to achieve capital growth by investing principally in Continental European quoted smaller companies. The benchmark index is the MSCI Europe ex UK Small Cap Index (in sterling terms).

Fund profile

Montanaro European Smaller Companies Trust (MTE) aims to achieve capital growth by investing principally in smaller, quoted, Continental European companies (those within the European Union, Norway and Switzerland) but is not restricted from investing in smaller companies quoted on other European stock exchanges. The benchmark index is the MSCI Europe ex UK Small Cap Index (in sterling terms).

The original company dates back to 1981, but Montanaro Asset Management Limited (MAML) took on the management of the trust in September 2006 and the European small-cap investment approach dates from then. MAML had £3.1bn of assets under management at the end of September 2020.

The manager

MAML was established in 1991 and is chaired and owned (100%) by Charles Montanaro. However, the wider team has options over about half of the equity. The CEO is Cédric Durant des Aulnois. Mark Rogers is head of investments, the lead manager on MTE is George Cooke, and Stefan Fischerfeier acts as George’s back-up. These five are all members of the investment committee, which also includes Alex Magni.

They are supported by what MAML believes is the largest and most experienced team in Europe, specialising in researching and investing in quoted small and mid-cap companies. The team is 33-strong altogether – including an investment team of 13 – having expanded again recently (hiring a new healthcare analyst in May) despite the setback in markets. The team is multi-lingual and multi-national (10 countries in all). All but one of the fund managers also have research responsibilities.

In addition to MTE, the team manages a range of funds focused on UK and European equities and, most recently, the Montanaro Better World Fund, an open-ended fund investing in small and mid-cap companies supporting the UN Sustainable Development Goals.

Surviving COVID

The past few months have proved a testing time for many of us. It took some time for the pandemic to make itself felt in markets but, as it became apparent that the virus was hard to contain and lockdowns started, panic set in. The considerable economic stimulus injected by governments and central banks has helped to calm nerves since.

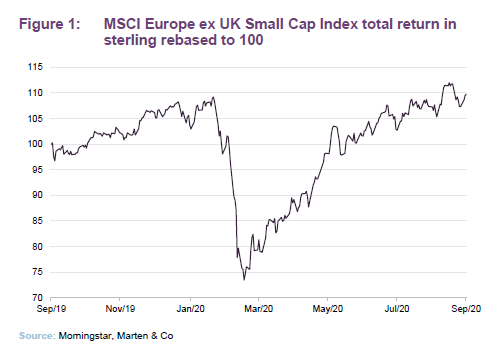

By the end of September 2020, a sterling investor had seen a 12-month gain on an investment in European smaller companies, as represented by the MSCI Europe ex UK Small Cap Index of almost 10% (aided by a weak pound). However, within the index there has been considerable dispersion of returns.

MTE’s investment approach has helped position it well for the current crisis. A focus on quality and growth is exactly what investors have been looking for amid the uncertainty created by COVID. As we explain on pages 10 and 11, MTE has beaten both its benchmark and its peer group by a considerable margin since the pandemic struck, further extending its run of outperformance.

MAML is a long-term investor and is prepared to look through the current crisis and stick by companies that it believes have viable business models. George feels that it is unclear whether or not there will be an immediate swathe of business bankruptcies. The considerable support that governments and central bankers have injected into economies – furlough schemes, guaranteed loans, interest rate suppression and the like – has had a positive overall effect and has staved off the worst. However, George cautions that for companies without a viable long-term business model, this support merely delays the inevitable.

As we note on page 6, the investment process emphasises meeting management and ‘kicking the tyres’. COVID-19 interrupted that process, but it came after a record year for meetings in 2019 and the analysts have been focusing on virtual meetings over the past few months.

Investment process

MAML wants to invest in:

- simple businesses that it can understand;

- niche businesses in growth markets (non-cyclical companies, growing organically);

- market leaders (strong, defensible market positions and pricing power);

- companies with high operating margins and high returns on capital (barriers to entry/a sustainable competitive advantage);

- profitable companies trading at sensible valuations; and

- good management that it trusts (aligned to shareholders and demonstrating sound ESG practices).

This could be summed up as investing in high-quality businesses at sensible prices. Furthermore, MAML believes it is important to:

- do the work yourself (rather than relying on brokers);

- be passionate; and

- learn from mistakes (humility goes a long way).

In addition, MAML believes that it is easier to add value through stock selection for a small and mid-cap portfolio, especially given the relative paucity of research available on these companies.

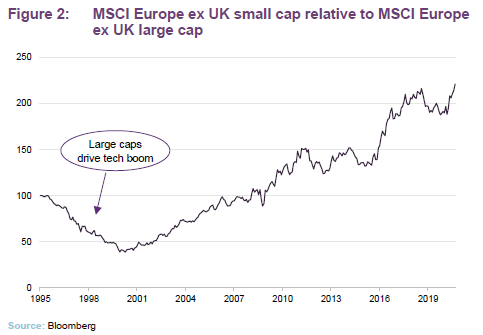

Figure 2 might suggest that this approach works. From end January 1995 (as far back as the data is available) to the end of September 2020, European smaller companies (as represented by the MSCI Europe ex UK Small Cap index) have outperformed larger companies (as represented by the MSCI Europe ex UK large Cap index) by 3.1% per annum (source: Bloomberg).

Sifting through the universe

The constituents for MTE’s portfolio are drawn from a universe of about 4,000 companies listed in Europe. The focus is on those with a market cap between €100m and €5bn (about 2,300) and, as described below, unprofitable companies are excluded which reduces the pool to about 1,700 stocks. The benchmark index currently includes stocks with market caps of up to €7bn.

MTE is a true stock-picking portfolio; index-weightings play no part in forming its portfolio construction. MAML has always generated its own investment ideas rather than relying on external analysts. There are many good reasons for this but it is also fortunate as the availability and quality of external analysis – which MAML believes has been on a declining trend for some time – has been exacerbated by MiFID II. The upshot is that there are many stocks within MTE’s universe that have no research coverage at all. This gives MAML a competitive edge, which is sharpened by the strength and depth of its research team (see page 18).

The size of the team allows for some theoretical research, and lateral creative thought is encouraged. MAML is an entrepreneurial boutique with a flat structure that allows for quick decision-making and avoids the politics that bog down more bureaucratic large asset managers. MAML does not encourage the development of ‘star’ fund managers, but is focused on staff retention, including the granting of staff options over MAML equity. The 13 members of the investment team have been with MAML for 9.7 years on average. MAML’s ‘back office’ functions are carried out in-house rather than being outsourced (as they are in many smaller investment management boutiques).

Research responsibilities are distributed amongst the team on a sector, global basis. Emphasis is placed on being well-prepared for meetings, which is possible as the research team is well-resourced. MAML’s analysts can then set the agenda, challenge management and get the information that they need. Site visits are encouraged (another perk of having a large team is that it is not desk-bound).

On average, each analyst will seek to identify 20 stocks within their sector coverage worthy of closer scrutiny. These will form the pool from which portfolio constituents are drawn. The first part of the process is to eliminate poor-quality companies. These stocks are identified by applying a quantitative screen to the wider universe. Loss-making companies, those with poor cash flow and highly indebted businesses are rejected. Stocks that fit structural growth themes that the team has identified may be prioritised. Each company within the universe is assigned a quality rating (D to AAA).

The analysts then build a financial model and conduct a proprietary checklist for each stock. They also check whether a stock meets MAML’s ESG criteria (see below). Then the idea is put before MAML’s investment committee, who challenge assumptions and ask for more information if they feel this is warranted. Stocks that pass these quality thresholds may then go on to an approved list of approximately 200 companies. No fund manager can buy a company that is not on the approved list.

Various valuation tools are considered (primarily discounted cash flows) but include P/E, free cash flow yield, dividend yield and relative to peers and the team operates with a time horizon of five to 10 years. The ideal investment should provide a margin of safety in excess of 25% over its intrinsic value. Analysts will also look at risk factors. Analysts will then assign a recommendation to each stock. These will be presented to the whole team at weekly meetings and the fund managers will then decide which stocks make it into portfolios. Once a stock makes it into a portfolio, it will usually remain there for many years.

Portfolio construction

MTE’s investment policy is more fully described in its Annual Report. It only invests in listed securities and MAML says that unquoted companies are not eligible for consideration.

Some other rules apply:

- MTE does not hedge its currency exposure;

- MAML will hold no more than 10% of the voting rights in any company (across all funds managed by MAML); and

- no more than 10%, in aggregate, of the value of its total assets at the time of investment, will be invested in other investment trusts or investment companies admitted to the Official List of the UK Listing Authority. Currently, MTE has no holdings in other investment trusts nor does it expect to ever do so.

Typically, the target weighting for a new position will be between 1% and 3.5%, depending on both the strength of conviction that the manager has in the stock, and its liquidity. The total number of holdings is typically around 50. There is no obligation to sell a company if its market cap exceeds €5bn, but these will be gradually recycled into lower market cap companies. The manager will ensure that a single position does exceed 7.5% of the portfolio.

ESG analysis

MAML’s focus on quality is supported by its commitment to ESG principles. It has an internal Sustainability committee that meets quarterly and oversees MAML’s efforts in this area. MAML also has its own handbook, policies and checklists. It votes the shares it controls, and it engages with companies. MAML expects the companies that it invests in to improve their ESG awareness and it monitors their progress.

Some sectors are excluded from portfolios on ESG or ethical grounds. MAML portfolios will not contain tobacco companies; companies manufacturing weapons, facilitating gambling or manufacturing alcohol; companies engaged in oil-, coal- and gas-related E&P; companies involved with pornography; and those making high interest-rate loans. Corporate governance checks include an assessment of a company’s remuneration policy.

MAML’s attention to ESG issues extends to its own business. Following an extensive evaluation process, it was made a B Corp Certified company in June 2019. More information is available at bcorporation.net) where it explains that “Certified B Corporations are businesses that meet the highest standards of verified social and environmental performance, public transparency, and legal accountability to balance profit and purpose. B Corps are accelerating a global culture shift to redefine success in business and build a more inclusive and sustainable economy”.

Sell discipline

Stocks exit the portfolio for a variety of reasons – for example, when they become significantly overvalued, if they become too big, or due to takeovers.

Furthermore, stocks may leave the portfolio if the analysts identify unfavourable changes in the fundamentals of the business or an unfavourable management change.

Stocks will also be sold if they no longer pass MAML’s quality threshold, or if a new opportunity comes along that offers better prospects.

Asset allocation

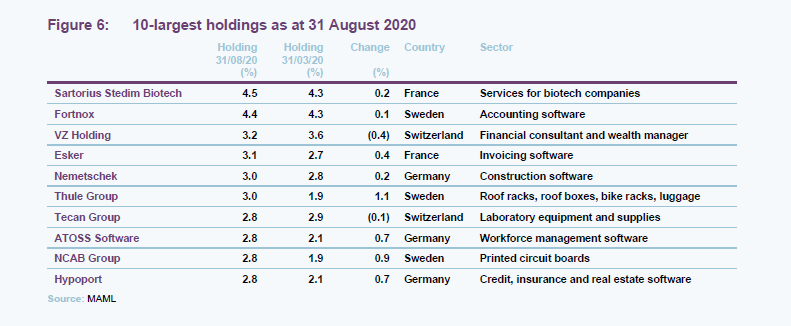

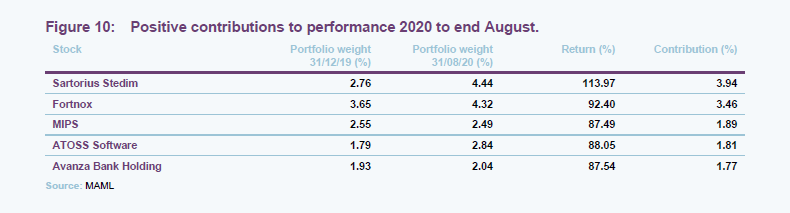

There were 55 holdings in the portfolio at the end of August 2020.

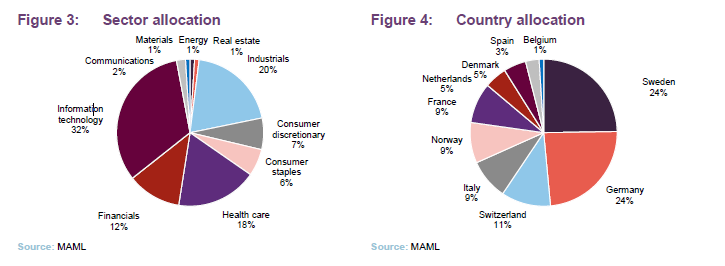

Geographic and sector allocations are determined by stock selection, but MTE has had a long-term overweight exposure to healthcare and technology companies relative to its benchmark.

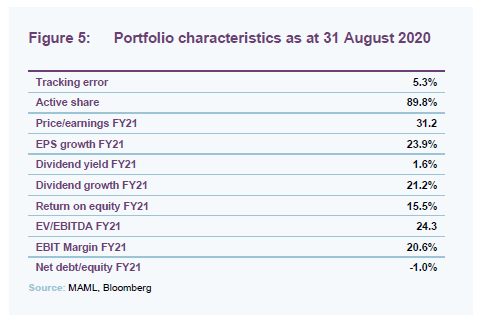

As one might expect, MTE’s portfolio is quite different to that of its benchmark, as evidenced by a high active share of 89.8% at the end of August 2020.

Companies tend to trade on relatively high valuation multiples, but offer much higher rates of earnings growth than the average European company, higher returns on equity (helped by the portfolio’s bias away from highly capital intensive businesses), higher margins and lower levels of indebtedness.

The 10-largest holdings are not much changed from five months ago, reflecting the manager’s long-term approach. George says that the emphasis on investing in companies with robust balance sheets meant that there was not any major fundraising activity within the portfolio. He did not trade much more than usual during the period of extreme market volatility in March and April.

Since we last published a note on MTE, IMA (an Italian manufacturer of machines used in packaging) was the subject of a takeover bid at a reasonable premium to the prevailing share price.

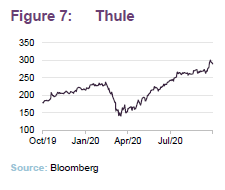

Thule

Thule (thulegroup.com/en) has moved up into the top 10 list. It is a Swedish manufacturer of products that support an active life, including roof racks, roof boxes, bike racks and trailers for cars, camera bags, sports- and duffel bags, luggage and strollers. The company’s performance since the outbreak has been mixed. Total lockdowns restricted sales in some of their key areas, but as these were eased, sales began to recover again. Cash flow was fairly strong, helped by a reduction in inventory. The company thinks that the ‘staycation’ trend is a positive for its business.

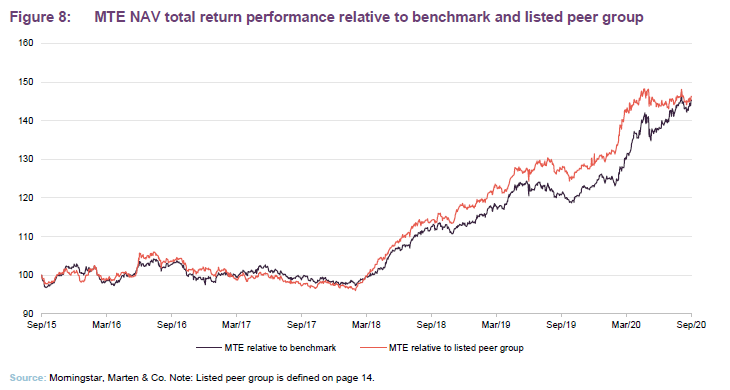

Performance

MTE’s strong relative performance is evident in Figure 8. The trust held its own against the benchmark until 2018, but accelerated away once concerns started to build about the pace of economic growth in Q1 2018. MTE did particularly well when panic set into markets in March 2020. The portfolio’s bias to financially strong, high quality stocks was prized in that situation. Recently, more speculative stocks have seen some price recovery and, relative to the listed peer group at least, MTE has tracked sideways.

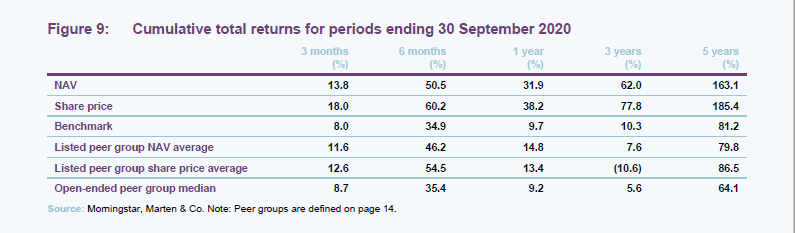

As Figure 9 shows, in absolute terms, MTE’s performance has been particularly impressive. Over the past five years, it is more than 80 percentage points ahead of both the listed peer group average (see page 14) and its benchmark.

MTE’s geographic asset allocation had only a modest impact on returns. An overweight exposure to Sweden was positive but this was offset by an underweight exposure to Switzerland (where the managers struggle to find attractively valued stocks).

The trust’s natural bias to sectors such as technology and healthcare and away from energy and real estate meant that it was well-positioned to cope with the impact of COVID.

The real kick to returns came from stock selection, however. Even in sectors such as financials, where the sector underperformed the wider market, MTE added considerable value.

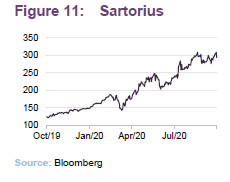

Sartorius

Sartorius (www.sartorius.com/en), is a longstanding holding. The company makes equipment needed to produce biologics and biosimilars, such as vaccines and monoclonal antibodies. Unsurprisingly, perhaps, it has been a beneficiary of the ongoing effort to tackle the COVID-19 outbreak. The company says that it works with the majority of the 180+ companies working on corona vaccines.

Sales grew by 22.5% year-on-year over the first half of 2020 and underlying earnings per share were 27.7% higher. Sales growth was highest in Asia, where Sartorius aims to grow its business significantly over the next five years, with a focus on China.

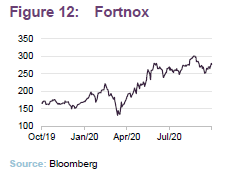

Fortnox

Fortnox (www.fortnox.se/investors/) provides cloud-based accounting software and a range of other administration tools for over 300,000 small businesses. The shift to home-working, in the wake of the pandemic, has provided a boost to growth. Sales in the second quarter were 32% ahead of the prior year and quarterly operating profit hit a new high. For the manager, a large part of the attraction is the predictable recurring revenue that the business generates. While some businesses may be experiencing a temporary fillip to sales as a result of COVID-19, the manager thinks that Fortnox will hang onto the new business that it is winning.

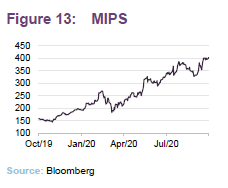

MIPS

MIPS (www.mipsprotection.com) makes inserts for helmets that help absorb some of the impact of accidents on the brain (helping to reduce the transmission of rotational motion to the brain). The inserts are used in a wide range of helmets but the boom in cycling over the past few months, associated with a reduction in the use of public transport and the growth of ‘staycationing’, have driven a big spike in sales. The managers have elected to book some profits on this position, reasoning that sales may be being pulled forward for this company.

ATOSS Software

ATOSS Software (www.atoss.com/en-gb/investor-relations) makes HR and workforce management software. This is a stock that has been in the portfolio for a couple of years. As with Fortnox, the shift to home working and the increase in flexible time working has required companies to invest in cloud-based software solutions. For H1 2020, a 20% increase in sales growth drove a 40% uplift in profit and earnings per share.

Avanza

Avanza (investors.avanza.se/en/about/about-avanza/) operates a platform for savings and investments in Sweden. A lack of legacy infrastructure helps boost margins. High penetration into the 20–39 age-group creates an expectation of organic growth as investors save more as they age. Customer growth is 114% higher in 2020 than 2019. Operating profit for H1 2020 was 184% higher than for H1 2019 and earnings per share 173% higher.

Others

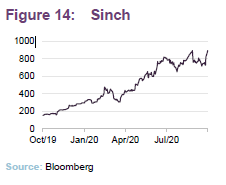

The manager also notes the strong performance delivered by Sinch, which was up 184% over the eight months ending 31 August 2020 and the best performing stock in the portfolio. Sinch offers a cloud-based platform that lets businesses engage with their customers through mobile messaging, voice and video and is a beneficiary of the switch to home working. He also highlighted ChemoMetec, which was a small position in the portfolio, reflecting the risks attached to a young business in a new field. It makes cell counters which are used in cell-based immunotherapy, cancer and stem cell research, drug development and production.

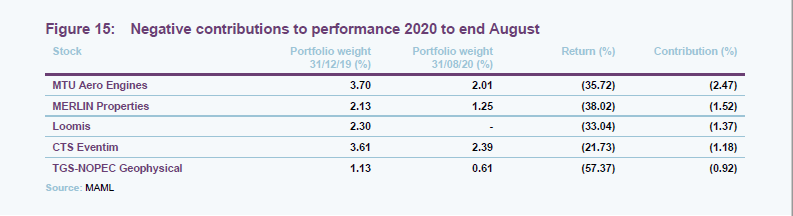

MTU Aero Engines

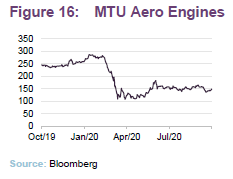

MTU Aero Engines (www.mtu.de/investor-relations/) was the largest position in the portfolio when we wrote our last note and perhaps still would be if it were not for COVID-19. This German-based business makes components and undertakes maintenance work for a range of aircraft manufacturers. Demand for innovative products such as those used in the engine for the A320 neo was high ahead of the pandemic, but now the airline industry faces an uncertain future. The company says that air traffic demand may not reach 2019 levels until 2024. Revenue for H1 2020 was down 9% and net income fell by 38%. The manager has faith in the stock and believes it has the balance sheet strength to weather the downturn. The company is generating cash and placed a €500m bond earlier this year. The managers plan to stick with the position.

MERLIN Properties

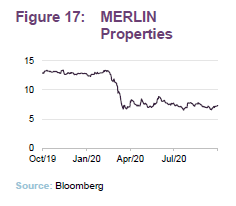

MERLIN Properties (www.merlinproperties.com/en/investors/) is a Spanish/ Portuguese real estate company, structured as a SOCIMI (the Spanish equivalent of a REIT) and with a diversified portfolio including offices, shopping centres, logistics and other types of property. Lockdown restrictions have put pressure on occupiers, especially with respect to footfall in shopping centres. The retail assets have been marked down in value. The company’s LTV was 40.1% at 30 June 2020 but, with an average maturity of 6.5 years and no repayment due until May 2022, the company is in a reasonably good position.

Loomis

Loomis (www.loomis.com/en/investors) is Europe’s largest handler of physical cash and the business has economies of scale that the managers thought made it attractive. However, the COVID outbreak has dramatically accelerated the shift to a cashless society and, in light of that, the decision was taken to exit this holding.

CTS Eventim

CTS Eventim (corporate.eventim.de/en/investor-relations/) is an events ticketing business. Social distancing measures have hit the live events business hard – revenue for H1 2020 was 71.5% lower than for the equivalent period in 2019. Cost cutting protected the company from the worst of this and it is exploring ways of restoring live entertainment.

TGS NOPEC Geophysical

TGS-NOPEC Geophysical (tgs.com/investor-center) is a casualty of the collapse in the oil price. It provides subsurface data to the oil & gas E&P industry. Revenue halved in the first six months of 2020.

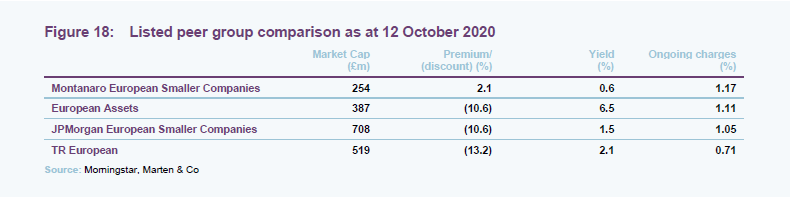

Peer groups

For the purposes of this note, we have compared MTE with the other trusts in the AIC’s European smaller companies sector. Although a respectable size, MTE is the smallest of these. It also has the lowest yield, reflecting the focus on growth companies (NB: European Asset’s yield is artificially inflated by payments from capital). MTE’s ongoing charges ratio is in line with funds of an equivalent size. MTE is the only trust to trade at a premium, reflecting we think its superior performance record.

In Figure 19 below, we have also included data from MTE’s open-ended peers – a group of 56 funds available for sale in the UK and European Union. MTE beats the peer group averages over every time period and, if we combine both peer groups, MTE is the best-performing fund over three years.

Dividend

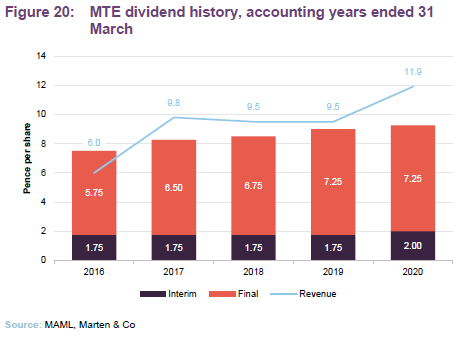

MTE’s primary aim is to deliver capital growth to its shareholders, and its dividend yield is modest, 0.6% as at 12 October 2020. However, over the long term, growth in dividends of the companies in which it invests has allowed MTE to grow its dividend while also building a substantial revenue reserve. This reserve stood at £4.3m at the end of March 2020 (equivalent to 25.5p per share).

In the face of widespread dividend cuts across Europe, a consequence of the pandemic, the board has indicated that MTE’s revenue for the year ended 31 March 2021 may fall. Nevertheless, with more than a year’s dividend in reserve, it seems unlikely that the board will cut the dividend.

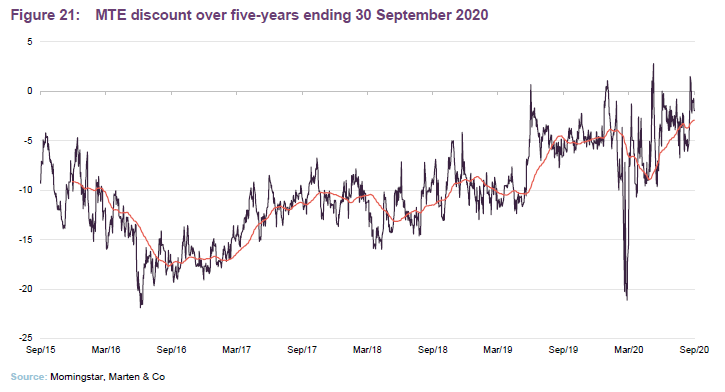

Discount

Over the year to the end of September 2020, MTE’s shares traded within a range of a 21.1% discount to a 2.8% premium and an average discount of 5.1%. At 12 October 2020, the shares were trading at a premium of 2.1%.

MTE has powers to issue and buyback shares, which it renews regularly at the AGM. Shares repurchased can be held in treasury and may be reissued. The board has said that these would only be reissued at a higher absolute price than the weighted average purchase price of the shares in treasury, and at a premium to NAV at the time of reissue or at a discount, provided this discount was lower than the weighted average discount at the time the shares were repurchased.

The net effect of this should be that purchasing the shares and reissuing them again is profitable for ongoing shareholders.

The board has stated that it will consider a buyback of shares where the discount of the share price to the NAV per share is greater than 10% for a sustained period of time and is significantly wider than the average for similar trusts. The board will take into consideration the effect of the buyback on the liquidity of the company’s shares.

In addition, the board encourages the manager to market the company to new investors.

Fees and costs

MAML is the company’s investment manager and AIFM. It is entitled to receive a management fee of 0.9% of MTE’s market capitalisation, payable monthly in arrears. Such a fee structure incentivises the manager to keep the company’s discount narrow. MAML is also entitled to a fee of £50,000 a year for acting as the AIFM. There is no performance fee. The management contract can be terminated by either side on six months’ notice. MTE charges 35% of the management fee against revenue and the balance against capital. The same methodology is applied to the accounting treatment for interest on MTE’s borrowings.

Link Company Matters Limited provides company secretarial services and Link Alternative Fund Administrators provides general administrative services. Equiniti Limited acts as Registrar and The Bank of New York Mellon (International) Limited as the company’s Depositary and Custodian. The company’s auditor is Ernst & Young. The company’s ongoing charges ratio for the year ended 31 March 2020 was 1.2%, unchanged from the previous year.

Capital structure and life

MTE has 16,733,260 ordinary shares in issue and no other classes of share capital. In addition, 715,000 shares are held in treasury. The company has an unlimited life.

MTE’s accounting year end is 31 March. Annual accounts are published around the end of June/beginning of July and the AGM is usually held in August or September.

Gearing

The board has set a maximum limit on borrowing, net of cash, of 30% of shareholders’ funds at the time of borrowing. The board, in discussion with the manager, regularly reviews the company’s gearing strategy and approves the arrangement of any gearing facility. The board believes that the ability to use gearing offers a strong competitive advantage over alternative open-ended investment funds. Therefore, it strongly encourages the active use of gearing by the manager.

MTE has a €10m secured loan maturing on 13 September 2023 that carries a fixed rate of interest of 1.33%, and a €15m revolving credit facility until 13 September 2023, both provided by ING Bank NV. Drawdowns from the revolving credit facility are charged at a margin over the relevant EURIBOR rate.

At the end of September 2020, MTE had net gearing of 0.6%.

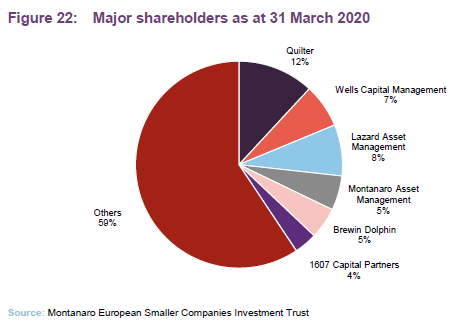

Major shareholders

Management team

Charles Montanaro

Charles’s investment career began in 1980 with a spell as a private client broker at Merrill Lynch. He joined Dean Witter Reynolds in 1984 and Drexel Burnham Lambert in 1987. At both firms he was their top institutional broker in the UK. He joined Drexel’s high yield bond team in 1989 and moved to MMG Patricof (now Apax Partners) in 1990 before founding MAML in August 1991.

Cédric Durant des Aulnois

Cédric joined MAML in 2007 as an analyst and became responsible for business development in 2011. He was appointed CEO on 1 January 2016. His earlier career got under way in 2000 when, having graduated from the LSE, he joined IDEA Global as a UK equity analyst. He later joined Fox-Pitt Kelton as a banking analyst and then moved to Lehman Brothers, where he spent three years analysing the French and Benelux banking markets.

Mark Rogers

Mark joined MAML in 2014 and is both head of investments and the co-manager of the Better World Fund. His previous experience includes four years at Bankers Trust Asset Management (as a UK portfolio manager), 17 years at Nomura Asset Management (as a European equities investment manager and later as head of research), and seven years as director of European equity research for Fidelity Worldwide Investments in London.

George Cooke

George joined MAML in July 2010. He graduated from the University of Nottingham in 2005 with an undergraduate degree in Management Studies. He spent a further year of study there, at the end of which he was awarded a Masters (with Distinction) in Corporate Strategy & Governance. Immediately following this, he joined the graduate scheme at Aon Benfield (formerly Aon Re). Having completed this scheme, George settled as an analyst within the ReSolutions department where he specialised in assisting with the capital and runoff issues of insurance and reinsurance companies. During his time at the company, George received a Diploma in Insurance. He is also a CFA Charterholder.

Stefan Fischerfeier

Stefan joined MAML in 2007. He holds a B.A. in Business Administration from the University of Cooperative Education in Mannheim (1995) as well as a Diplom-Kaufmann (MBA equivalent) from the University of Mainz (1998). He graduated from the London Business School with an MSc in Finance (2006). After graduating from University of Mainz he spent more than six years at Accenture in Germany, Switzerland, France, and the UK as a management consultant for European banks and asset managers. Stefan then worked as an analyst at Nordwind Capital, a Munich based private equity company, analysing the automotive industry, and as an investment consultant for a property fund in Romania assessing real estate investment opportunities in Eastern Europe.

Board

Following the recent recruitment of Gordon Neilly, the board consists of four directors, all of whom are independent of the manager and who do not sit together on other boards. Each director offers himself or herself up for re-election at each AGM.

Richard Curling

Richard was appointed to the board in 2015 and became chairman in 2018. He has over 30 years’ experience as a fund manager and is currently an investment director at Jupiter Fund Management Plc. He also has extensive experience of investment trusts. Richard is also chairman of the nominations committee.

Gordon Neilly

Gordon was, until the end of August 2020, chief of staff at Standard Life Aberdeen, prior to which he was global head of strategy at Aberdeen Standard Investments and was responsible for developing the group’s strategy and overseeing its implementation as well as overseeing all corporate activity for the Group and its closed end fund business. He joined Aberdeen in 2016 from Cantor Fitzgerald, where he held the position of joint CEO. Gordon is currently a non-executive director of Personal Assets Trust Plc.

Caroline Roxburgh

Caroline is a Chartered Accountant with over 30 years’ experience in finance and audit and was formerly a partner at PricewaterhouseCoopers LLP until her retirement in 2016. She chairs the audit committee. Caroline also holds a number of other board positions, including a non-executive directorship of the Edinburgh Worldwide Investment Trust Plc.

Merryn Somerset Webb

Merryn was appointed in 2011. She is the editor-in-chief of UK personal finance magazine MoneyWeek, writes for the Financial Times and is a radio and television commentator on financial matters. She is also a director of Baillie Gifford Shin Nippon Plc, Murray Income Trust Plc and Netwealth Investment Limited. She is chairman of the remuneration committee.

Previous notes

Readers interested in further information about MTE may wish to read our other notes.

The legal bit

This marketing communication has been prepared for Montanaro European Smaller Companies Investment Trust Plc by Marten & Co (which is authorised and regulated by the Financial Conduct Authority) and is non-independent research as defined under Article 36 of the Commission Delegated Regulation (EU) 2017/565 of 25 April 2016 supplementing the Markets in Financial Instruments Directive (MIFID). It is intended for use by investment professionals as defined in article 19 (5) of the Financial Services Act 2000 (Financial Promotion) Order 2005. Marten & Co is not authorised to give advice to retail clients and, if you are not a professional investor, or in any other way are prohibited or restricted from receiving this information, you should disregard it. The note does not have regard to the specific investment objectives, financial situation and needs of any specific person who may receive it.

The note has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. The analysts who prepared this note are not constrained from dealing ahead of it but, in practice, and in accordance with our internal code of good conduct, will refrain from doing so for the period from which they first obtained the information necessary to prepare the note until one month after the note’s publication. Nevertheless, they may have an interest in any of the securities mentioned within this note.

This note has been compiled from publicly available information. This note is not directed at any person in any jurisdiction where (by reason of that person’s nationality, residence or otherwise) the publication or availability of this note is prohibited.

Accuracy of Content: Whilst Marten & Co uses reasonable efforts to obtain information from sources which we believe to be reliable and to ensure that the information in this note is up to date and accurate, we make no representation or warranty that the information contained in this note is accurate, reliable or complete. The information contained in this note is provided by Marten & Co for personal use and information purposes generally. You are solely liable for any use you may make of this information. The information is inherently subject to change without notice and may become outdated. You, therefore, should verify any information obtained from this note before you use it.

No Advice: Nothing contained in this note constitutes or should be construed to constitute investment, legal, tax or other advice.

No Representation or Warranty: No representation, warranty or guarantee of any kind, express or implied is given by Marten & Co in respect of any information contained on this note.

Exclusion of Liability: To the fullest extent allowed by law, Marten & Co shall not be liable for any direct or indirect losses, damages, costs or expenses incurred or suffered by you arising out or in connection with the access to, use of or reliance on any information contained on this note. In no circumstance shall Marten & Co and its employees have any liability for consequential or special damages.

Governing Law and Jurisdiction: These terms and conditions and all matters connected with them, are governed by the laws of England and Wales and shall be subject to the exclusive jurisdiction of the English courts. If you access this note from outside the UK, you are responsible for ensuring compliance with any local laws relating to access.

No information contained in this note shall form the basis of, or be relied upon in connection with, any offer or commitment whatsoever in any jurisdiction.

Investment Performance Information: Please remember that past performance is not necessarily a guide to the future and that the value of shares and the income from them can go down as well as up. Exchange rates may also cause the value of underlying overseas investments to go down as well as up. Marten & Co may write on companies that use gearing in a number of forms that can increase volatility and, in some cases, to a complete loss of an investment.