Strategic Equity Capital – Back to its roots

Back to its roots

Since May 2020, Strategic Equity Capital (SEC) has been managed by the public equity team at Gresham House Asset Management. The head of that team, Ken Wotton, became lead-manager of the trust in September, working alongside Adam Khanbhai. The chair of SEC’s investment committee is now Tony Dalwood, SEC’s lead manager when it was launched in 2005 and Gresham House Plc’s CEO.

Under its new leadership, SEC is gradually refocusing its portfolio on smaller companies where it can take more material stakes and exercise a greater degree of influence. Whilst the core investment strategy is unchanged, we think that this reflects a return to the original ethos of the trust. Over Q4 2020, three full exits were achieved, two new investments made and five of the stocks in the portfolio are ones where the manager has a significant stake. The manager believes that there is now a clear path towards improved performance and a narrowing of the discount.

Focused UK small companies portfolio

SEC aims to achieve absolute returns over a medium-term period, principally through capital growth. SEC is managed with a focused portfolio of investments selected on the same basis that a private equity investor would use to appraise its investments.

|

|

Fund profile

Launched in 2005, Strategic Equity Capital (SEC) is a London listed investment trust that invests in a concentrated portfolio of predominantly UK-listed equities (with the majority of the portfolio invested in 10–15 holdings).

SEC aims to achieve absolute returns over a medium-term period (targeting 15% IRR), principally through capital growth. SEC is managed with a focused portfolio of investments selected on the same basis that a private equity investor would use to appraise its investments. The investment manager looks for securities that it believes are undervalued and could benefit from strategic, operational or management initiatives. The approach is not constrained by any benchmark and does not currently employ leverage at the investment trust level.

The mandate permits investment in unquoted securities (up to 20% of gross assets at the time of investment) but this is not utilised currently.

The manager also has the flexibility to invest up to 20% in assets quoted on exchanges that are not operated by the London Stock Exchange but the manager does not expect this to be a significant element of the portfolio.

Investment manager

On 21 May 2020, following a review by the board of the company’s management arrangements, Gresham House Asset Management Limited (GHAM) became SEC’s investment manager. The investment team moved across from GVQ Investment Management.

Then, on 29 September 2020, Ken Wotton became lead manager, working alongside Adam Khanbhai, who has been working on the fund since 2014 and co-manager since 2017. Jeff Harris left the team at this time. Ken has considerable experience of working on public equity portfolios within a private equity environment. He leads a much better-resourced team than was available to SEC under its previous manager. More information on this team is provided on page 19.

GHAM is a specialist alternative asset management group, dedicated to sustainable investments across a range of strategies, with expertise across forestry, housing, infrastructure, renewable energy and battery storage, public and private equity. The latter speciality provides an additional source of knowledge, expertise and synergy for SEC’s team.

The parent company, Gresham House Plc, is quoted on the London Stock Exchange (GHE:LN). Its CEO is Anthony (Tony) Dalwood, who was SEC’s lead manager when it was launched in 2005. He now heads up the investment committee that oversees the management team’s investment decisions (see page 20).

The recent announcement of the acquisition of Appian Asset Management Limited (which has a range of funds that invest globally across traditional and alternative asset classes including equities, property, infrastructure, and forestry) added about £300m to Gresham House Plc’s AUM, which stood at £3.9bn at the end of 2020.

GHAM offers a much better-resourced investment and marketing team than was available at the previous manager. In addition to GHAM’s own in-house marketing resources, SEC benefits from a distribution and marketing agreement that GHAM has with Aberdeen Standard Investments (ASI).

Exerting greater influence

Following a review of the investment process, the manager has resolved to refocus the portfolio over time towards companies with a smaller average market cap than the portfolio that GHAM inherited (companies with markets caps below £300m at the time of investment).

This shift in focus will allow SEC to have a higher average stake in each portfolio company, which in turn should give it greater influence over the strategic direction of those companies. The manager is keen that SEC undertakes more proactive constructive engagement with portfolio companies, a change that we think has been welcomed by SEC’s shareholders.

The portfolio is evolving gradually as cash is freed up from successful past investments. Three have been sold in recent months: Ergomed, Numis and 4Imprint (see page 9). The manager did not see the need for an immediate wholesale turnover of the portfolio. At the end of December 2020, SEC was invested in five companies where funds managed or advised by GHAM have more than a 10% stake.

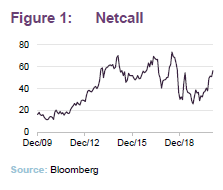

Netcall

We asked Ken for a practical example of the investment approach within other funds that he has managed. He cited Netcall, a customer engagement software business that the team backed in 2010 and is still held within other portfolios that the team manage, but not within SEC’s portfolio.

Funds managed by Ken provided funding for a transformational acquisition in 2010. The position size was increased over subsequent years, taking advantage of forced sellers, to about 20% of its outstanding shares. Engagement activity included helping to recruit a new chairman in 2011 and the provision of funding for a series of enhancing acquisitions to help broaden the product set and achieve critical mass. The funds defended the company when it was the subject of an opportunistic takeover approach in 2015 and supported a shift to an enhanced distribution policy. They supported a second transformational acquisition in 2018, providing assistance with due diligence and introducing a new non-executive director.

Manager’s view

The financial strength of the companies that SEC holds worked in its favour when the pandemic struck. In addition, many of the stocks in the portfolio were operating in sectors that were less affected by or even benefitted from the crisis.

International investors have been looking warily at Brexit and the UK’s poor handling of the coronavirus. The UK market’s relative underweight exposure to higher-growth sectors such as technology has also been unhelpful. The UK market has been lagging its peers since the run-up to the Brexit referendum in 2016. The degree of its underperformance intensified over 2020, despite a modest bounce when the good news on vaccine trials was published in November 2020. That news triggered a significant rotation in markets as investors took profits on ‘growth’ stocks and upped exposure to cyclicals.

Relative to larger companies, UK smaller companies have recovered a little from the multi-year lows that they hit in the Spring. However, on an absolute basis, the manager believes that valuations are still very attractive and this is particularly true for the smaller of small companies.

This presents an opportunity to lay the groundwork for outperformance of the strategy over coming years. The manager sees a good pipeline of opportunities, but as always, they will be selective and proceed only after their extensive due diligence is complete.

The recent emergence of new strains of the virus illustrates that we are not out of the woods yet, and the manager expects to see second-order effects as the economy emerges from the current period of significant State interference.

Nevertheless, on a medium-term view, the manager is optimistic about the prospects for the portfolio. It says that it has a well-developed pipeline of new opportunities and a number of engagement initiatives are underway.

Investment process – applying a private equity approach to public companies

The investment strategy seeks to apply private equity investment techniques to investing in public companies. The manager invests with a long-term investment horizon. Central to the approach is constructive engagement with investee companies, with the aim of driving strategic, operational or management initiatives.

As described on page 4, GHAM believes that SEC should be taking influential minority stakes in companies, and has resolved to focus the portfolio on smaller companies where a fund of SEC’s size can exert influence.

Target companies will be, or have the potential to be, fundamentally strong, high-quality, cash generative businesses. These companies should be capable of generating positive and growing free cash flow after maintenance capital expenditure. They should be in control of their own destiny (i.e. investment case should not be reliant on cyclical growth). They should also be trading at a discount to their intrinsic value sufficient to offer potential returns of at least 15% per annum over the life of the investment.

The manager believes that a dearth of high-quality independent analysis of smaller companies has allowed the market to become inefficient and some companies to become mispriced. GHAM undertakes proprietary research to identify potential candidates for inclusion within the portfolio. It is aided in this by a widespread network of industry and market experts.

The portfolio is highly concentrated, with a target of 15–25 positions, of which the majority of value should be in 10–15 positions; there are about 20 positions currently. There is a maximum of 15% in any one investment.

Extensive due diligence

The team will first seek an initial meeting with the company’s management. The team will then prepare a one-page document covering an overview of the company and the investment thesis. These ideas are discussed by the investment team and, if the idea is judged to have merit, the next step is to prepare a preliminary investment report.

At this stage, the team will undertake site visits, build a comprehensive financial model, perform a stakeholder analysis and consult members of the investment committee and the manager’s wider advisory network. Potential exit valuations will be assessed based on comparable M&A and average ratings through an economic cycle.

The report will be placed before the investment committee, who will challenge assumptions and offer advice. If the committee agrees, the manager will then deepen the due diligence further, modelling downsides to the investment thesis, commissioning external reports and soliciting references from key stakeholders.

Investment committee approval is required before the manager is permitted to build a material stake in any investment.

Desired characteristics

- Portfolio companies should be operating in a sector that offers structural growth and a competitive landscape that affords attractive levels of long-term growth and rational competition.

- Quality is indicated by the presence of sustainable competitive advantages such as strong, defensible IP. Companies should have a strategic value, such as a desirable market position.

- Financially, companies should demonstrate attractive returns on capital and operating margins. Cash generation is prized over accounting profits, which can be more easily manipulated.

- SEC will not invest in extractive sectors (oil and gas, mining), nor ‘balance sheet’ financials (banks, insurers), as the manager believes that success in these businesses is more driven by macro factors like resource prices rather than operational aspects under the control of management.

- High-quality management is desirable, although SEC’s manager may seek to strengthen this as part of its engagement process.

- The investment case should not be compromised on ESG grounds.

- The shareholder register should be aligned with SEC’s objectives.

SEC will not back companies on the basis of speculative growth projections or those reliant on binary outcomes (such as biotech/tech companies reliant on the success of new products, for example). It will not invest in distressed businesses, companies operating in commoditised industries and those with intrinsically low operating margins, companies with controlling shareholders, and those with poor governance and/or weak financial systems and oversight.

Encouraging improvement in aspects of ESG may form part of the investment thesis. Once an investment is made, stewardship is central to the investment approach.

ESG

Sustainable investing is a strategic focus for all Gresham House funds, including SEC. Whilst SEC is not considered to be an ‘ESG fund’, ESG considerations are taken into account at every stage of the investment process. Due to the nature of the small cap companies in which SEC invests, governance is the most important factor in the manager’s approach to sustainable investment. An assessment of factors such as board composition, governance, control, company culture, alignment of interests, shareholder ownership structure and remuneration policy is incorporated within the investment process. Efforts to rectify perceived failings in these and other areas of ESG may form part of the engagement process (see below).

In addition, the manager believes that problems relating environmental and social issues represent risk factors that could compromise their investment thesis. Consequently, the investment process seeks to eliminate companies that face environmental and social risks that cannot be mitigated through engagement and governance changes.

Gresham House Plc is a signatory to the UN-supported Principles for Responsible Investment as well as the FRC’s UK Stewardship Code, UKSIF (UK Sustainable Investment and Finance Association) and Pensions for Purpose. It has also received the Green Economy Mark from the LSE.

The manager uses an in-house ‘ESG Decision Tool’ to assess and monitor ESG factors through the life of an investment.

Engagement

There is, we feel, a greater emphasis on engagement at GHAM than there was previously.

As far as possible, SEC’s aim is to build consensus with other stakeholders. It wants to unlock value for shareholders, but also build stronger businesses over the long term. The aim is to build a dialogue with management so that the GHAM team and its network are seen as trusted advisors.

Operating with a highly-focused portfolio, SEC’s management team can build and maintain a deep understanding of its portfolio companies and their potential. The team engages with company’s management and boards on areas such as capital allocation, remuneration policy and investor relations. It also offers its views on strategy. Engagement is undertaken privately as far as possible. The team will also seek to leverage its extensive network to the benefit of portfolio companies.

For the companies, a further benefit is that SEC’s manager has historically supported investee companies with capital to strengthen their financial position or undertake M&A where this is aligned with strategy and long term value creation.

Asset allocation

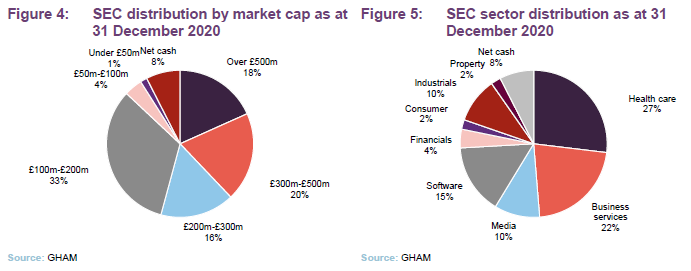

SEC has much more of its portfolio in stocks with market caps less than £300m than it did when we last published (62.1% versus 53.7%), evidence of the increased focus on smaller companies, where SEC can have greater influence.

Between 31 March (the data we used in our last note) and 31 December, the exposure to financials fell by about 8pps and exposure to business services and media both rose by about 5pps. These weightings are driven by the manager’s stock selection decisions, but reflect the emphasis within the investment approach on businesses operating within areas of secular growth. The cash position decreased by 2.1pps.

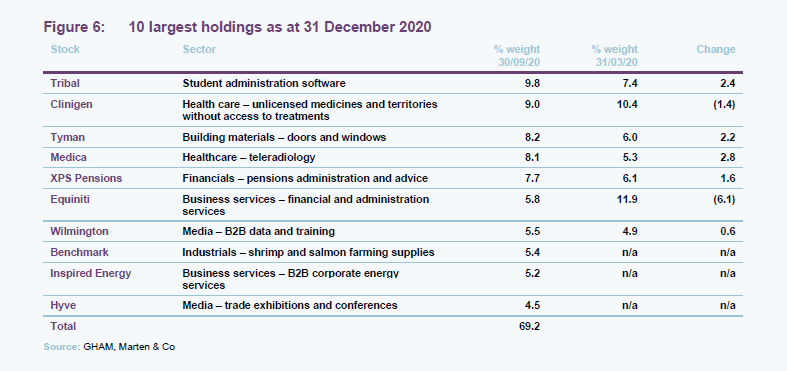

Top 10 holdings

The list of the 10-largest holdings at the end of December 2020 shows three changes to the line-up since we last wrote. Benchmark, Inspired Energy and Hyve had moved into the list to replace Ergomed, which is no longer held within the portfolio, see below, Alliance Pharma and Brooks Macdonald. Elsewhere in the portfolio, the trust’s longstanding holding in 4Imprint has also been sold, crystallising an IRR of 21.8% over the life of that investment, and complete disposals were also made of Eckoh (47% IRR) and EMIS (15% IRR). The manager also decided to sell SEC’s holding in Numis, which made a smaller but still positive contribution to returns.

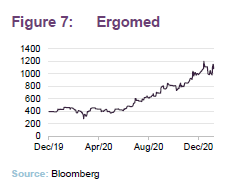

Ergomed

We discussed clinical outsourcing company Ergomed (ergomedplc.com) and many other holdings in our last note (see the link on page 23). The position has been exited following strong share price performance. As we show on page 14, it was the largest positive contributor to SEC’s NAV returns over Q3. SEC realised a 72%% IRR on this investment.

Its interim results, covering the six months ended 30 June, showed a 22% increase in its order book and an 18% increase in earnings per share. Services provided to companies developing vaccines and therapies for COVID-19 offset business lost as other clinical trials were postponed.

The proceeds were recycled into positions such as Medica, XPS and Inspired Energy as well as some new investments.

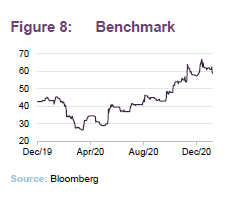

Benchmark Holdings

Benchmark (benchmarkplc.com) provides specialist products to the shrimp and salmon farming industry. Its provisional results for the year ended 30 September 2020 show falls in revenue and EBITDA, but a reduced loss per share. Whilst its genetics division did well, weaker shrimp markets (which they are attributing to COVID-19), heightened price competition in Artemia (the live food that it supplies to the industry) and lower revenues from its sea lice treatment all weighed on the company.

In our April note, we noted that SEC’s manager felt that Benchmark should exit its loss-making vaccine business. The company sold this division in July and the manager thinks that this will improve the long-term profitability of the company. They say that Benchmark has leading IP and there are high barriers to entry which supports material strategic value. The manager feels that significant strategic progress has been made this year at Benchmark; they have divested or closed multiple non-core activities (including the vaccine activities), strengthening the balance sheet and improving financial profile.

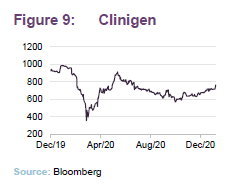

Clinigen

Speciality pharmaceutical services company Clinigen (clinigengroup.com) has become one of the largest positions in the portfolio. When we last published, the manager had been adding to the position following a period of price weakness. The shares then recovered strongly in Q2 but fell back again in the second half of 2020, in part as Iovance Biotherapeutics delayed its filing its melanoma treatment with the FDA until 2021. Clinigen owns the rights to a product called Proleukin, which is a mature medicine that is used alongside Iovance’s novel TIL (tumor infiltrating lymphocyte) treatment. Therefore, Cilnigen will benefit in increased sales of Proleukin if Iovance’s treatment is approved.

Clinigen’s results for the year ended 30 June demonstrated organic revenue and profit growth, dispelling fears of a significant COVID-19-related impact on its business (there was some disruption to clinical trials). New business wins helped drive growth but the company expected that the pace of recovery in clinical trial activity would be slow in 2021, and guided investors towards growth at the lower end of expectations. This guidance was unchanged at the AGM update in November.

The company anticipates an acceleration in its growth in 2022, helped by new business wins. In April, it agreed a global licensing and distribution agreement with Porton Biopharma to commercialise Erwinase, a therapy for patients with Acute Lymphoblastic Leukaemia who have developed hypersensitivity to E. coli-derived asparaginase.

Other purchases that have been made include Inspired Energy, Hyve Group, Ten Entertainment, SimplyBiz and Hostelworld (discussed in our last note), where SEC backed a fundraise.

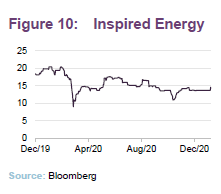

Inspired Energy

Other new holdings include Inspired Energy (inspiredplc.co.uk), a B2B corporate energy procurement and consultancy business. This is a stock that other Gresham funds have been investing in since 2011. SEC supported a fundraise aimed at strengthening the company‘s balance sheet and providing it with the firepower to continue to consolidate its sector. Inspired Energy helps businesses manage their energy requirements, offering advice on areas such as procurement and sustainability, often dealing with complex businesses operating from multiple sites.

On 11 December, the company announced that it had completed the disposal of its SME division to an MBO for up to £10.5m. While energy consumption has dropped across the board as a result of the lockdowns, the SME division had been most impacted by COVID-19 and is currently loss-making. The board estimates that there has been a £1.2m hit to forecast EBITDA. This COVID-19-related phenomenon should prove temporary.

In a trading update published on 29 January 2021, the company said that its performance through the end of Q4 remained resilient, despite the ongoing disruption from COVID-19, and the board expects that the corporate division, and consequently the group’s continuing operations, to report FY2020 underlying EBITDA in line with market consensus.

The manager says that trading remains subdued as lockdowns reduce business activity, but the company is well positioned and well financed.

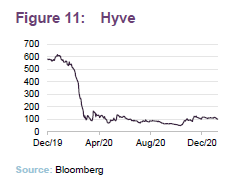

Hyve Group

Hyve (hyve.group) is an events business that stages a range of exhibitions and conferences. It has been improving profitability by focusing on larger events and shedding non-core business.

COVID-19 hit the company hard, triggering impairment charges of about £167m and threatening its debt covenants. £47m of insurance proceeds and a £127m, nine-for-four rights issue in May/June helped put the business on a surer footing. It was at this point that SEC first invested in the company. The manager had undertaken extensive due diligence on Hyve ahead of the rights issue but only decided to make an investment once there was more certainty around the balance sheet strength of the company.

Results for the year ended 30 September emphasised measures taken to cut costs. 67 of 127 events were cancelled during the period; others went ahead in regions where COVID-19 was under control and/or where it was possible to implement appropriate social distancing measures. The company also delivered around 100 webinars. Management believe that a swift return to profitability is possible once restrictions are lifted.

From a low base, the shares rose by 75% in Q4 2020 in response to the good news on vaccines. The rights issue gave Hyve the balance sheet strength to buy a digital event platform, Retail Meetup, for £19m and the manager says that the company has sufficient cash to trade into at least Q4 2021, even if no events take place before then.

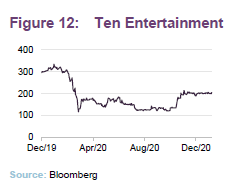

Ten Entertainment

Ten Entertainment (tegplc.co.uk) is a business that the Gresham House team knows well and other of the manager’s funds were invested in. Ten Entertainment is probably best known as a leading operator of ten-pin bowling centres. It operates 46 entertainment centres across the UK. Unsurprisingly, it has been hit hard by social distancing restrictions. All their centres were closed between 20 March and early August and are shut again now.

Ahead of the lockdown, trading for the 11 weeks to 15 March was running at 9.6% ahead of the previous year. However, for the six months ended 30 June as a whole, sales fell by 46% and the business was loss-making.

A £4.9m placing helped provide some liquidity and overheads were cut to conserve cash within the business. A new CEO started in September.

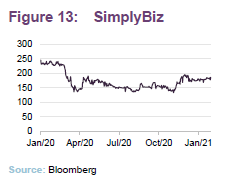

SimplyBiz

SimplyBiz (www.simplybizgroup.co.uk) is the UK’s leading provider of compliance and business support for financial services, legal and workplace benefits professionals. The company acquired the ratings business Defaqto in March 2019.

SEC has made an initial stake in the business. The manager feels that the company is trading on a low rating because of its high leverage and the impact of COVID-19. It sees the potential for margin recovery as well as continued revenue growth. A gradual shift to a SaaS model will help in that regard as it seeks to migrate clients to its digital platform. SimplyBiz is targeting revenue growth of 5–7% a year over the next two to three years and EBITDA margins of 35–40%.

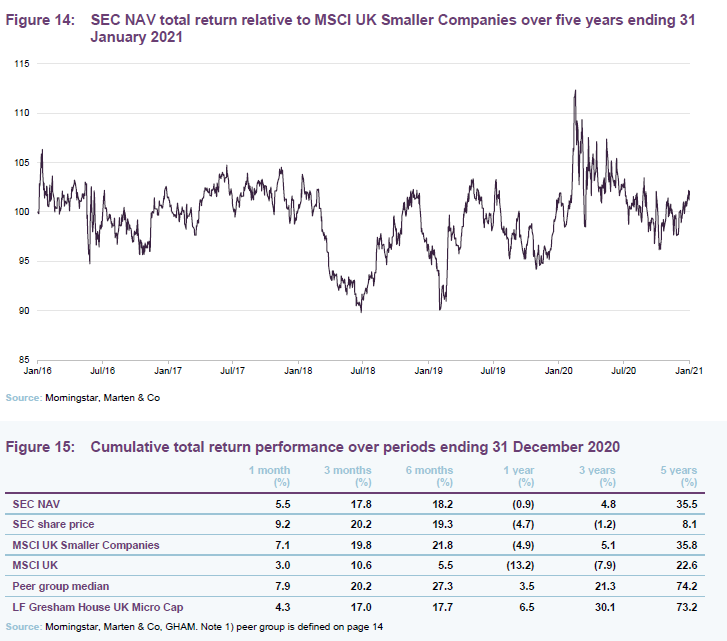

Performance

The relative resilience of SEC’s portfolio is evident in its strong outperformance during March this year, when COVID-19-related panic set into markets. As the market began to regain its confidence, there was less of a focus on indications of quality such as balance sheet strength and SEC gave up some of its relative outperformance.

The manager is optimistic that the refinements that have been made to the investment approach and the outlook for the portfolio present an opportunity for SEC to improve its long-term record both relative to indices and its peers. As an indicator of what might have been achieved had the new investment approach been in place for the past five years, we have included the returns of the LF Gresham House UK Micro Cap Fund within Figure 15. This is a fund that has been managed by Ken since it was launched.

Performance attribution

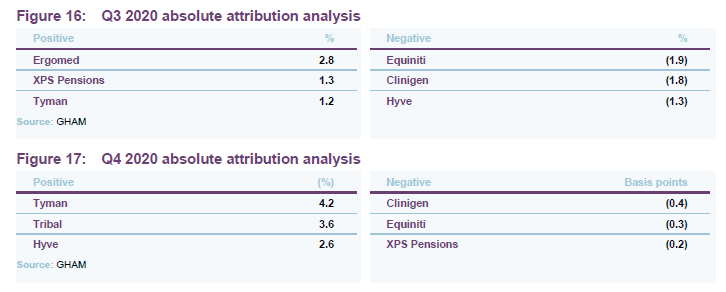

Our last note showed quarterly performance attribution data up to the end of Q1 2020. Figures 16 and 17 show the positive and negative contributions made to SEC’s performance over Q3 and Q4, respectively.

Tyman

After some initial disruption to its business, Tyman is recovering, helped by resurgent housebuilding in the US. After a 17% hit to sales in H1 2020, Q3 saw 3% revenue growth and that momentum was maintained over October and November. The company felt able to repay the £2.3m it received under the job retention scheme, and has indicated that it may be able to pay a final dividend. A new chairman, Nicky Hartery, has been appointed and directors were buying shares during Q4.

Tribal

Tribal has won a number of contracts including an eight-year deal worth £16.9m with Nanyang Technological University in Singapore and a £3.1m five-year contract with Kings College London. The manager believes that this illustrates customer buy-in to the company’s next generation of product; the Tribal Edge cloud product platform.

Equiniti

Equiniti’s half-year results showed falling revenue and EBITDA, and wiped-out profits. It lost revenue as dividend payments were suspended (it makes money from processing these), COVID-19 affected share trading volumes and the value of assets under administration fell. Lower interest rates also weighed on the group’s income. The manager continues to engage with the board and other shareholders and, in January 2021, a new CEO, Paul Lynam, has been appointed. Paul joins after 10 years as CEO of Secure Trust Bank.

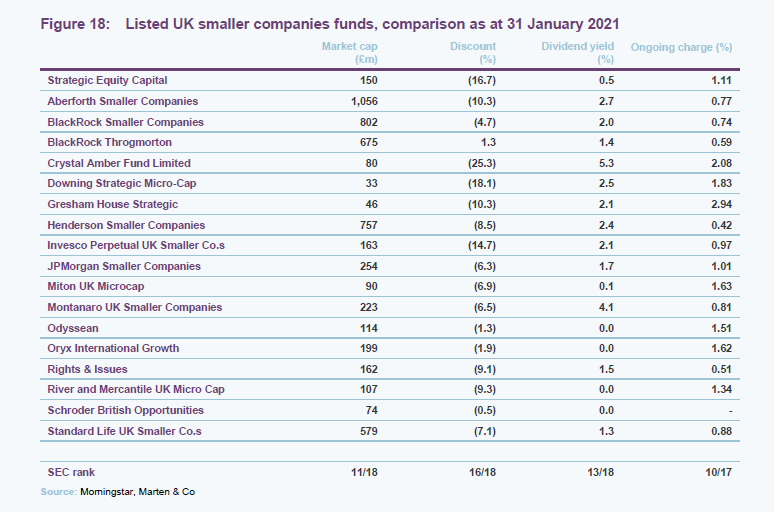

Peer group

The peer group that we have used for the purposes of this note is comprised of the constituents of the AIC’s UK smaller companies sector, excluding funds focused on generating income, those with split capital structures and very small funds. We have also excluded Marwyn Value Investors, which has a very different investment approach to the rest of the peer group.

When compared to this peer group, SEC is a reasonable size, although we think that there is scope for it to expand if it can eliminate its discount. The discount is currently one of the widest in the sector but we believe it will narrow if SEC’s relative performance improves. Notably, the discount on Gresham House Strategic, a trust managed by GHAM with a similar investment approach to that of SEC, is considerably narrower. The portfolio is not managed to produce a yield. The trust’s ongoing charges ratio is competitive for a fund of its size.

Dividend

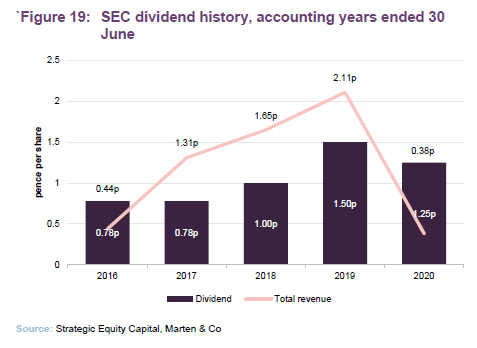

SEC’s investment strategy primarily focuses on generating capital growth for shareholders and dividends are paid to the extent that they are required to maintain SEC’s investment trust status. As such, dividends are likely to form a small component of shareholders overall returns and SEC pays one dividend in November a year. This is paid as a final dividend, following shareholders’ approval at the AGM (also usually in November).

COVID-19 triggered widespread dividend cuts, postponements and omissions and this had a significant impact on SEC’s revenue earnings. For the financial year that ended 30 June 2020, the board resolved to pay a dividend equivalent to the average for the previous two accounting years, using revenue reserves to make up the shortfall. Following this payment, SEC had revenue reserves of £1,042,789 (equivalent to 1.65p per share).

Premium/discount

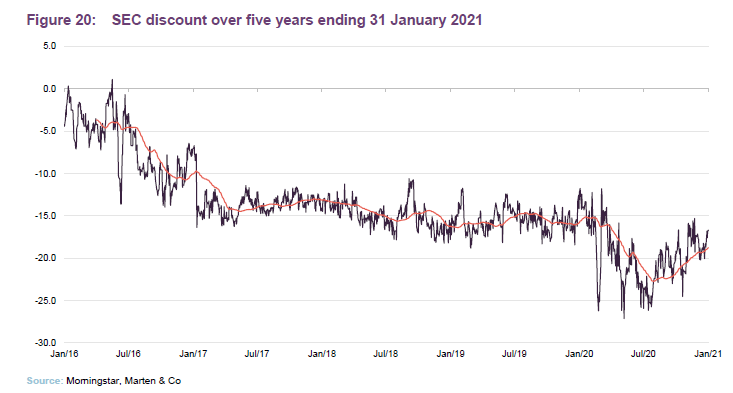

At 31 January 2021, SEC was trading at a discount of 16.7%. Over the year ended 31 January 2021, SEC’s shares traded within a range of a 27.1% discount (at the height of the market’s panic about COVID-19) to a low of 11.8%. The average discount was 19.6%. This is clearly too wide. It reflects the unpopularity of the UK and UK smaller companies in particular and the company’s performance track record over recent years.

The board believes, and we agree, that improved absolute and relative performance would lead to a narrowing of the discount. The additional marketing support provided by GHAM’s arrangement with Aberdeen Standard Investments should also help. If the changes that have been made to the investment approach translate into improved returns, investors could see a material uplift in the value of their investment as the discount narrows.

The manager points to the success that GHAM has had with narrowing the discount on Gresham House Strategic, from 29.2% when it assumed management of that trust in August 2015 to 10.3% at the time of publication.

Fees and costs

Under the terms of its investment management agreement with GHAM, SEC pays a base annual management fee 0.75% of its net asset value, payable quarterly in arrears.

GHAM can also earn a performance fee which is calculated as 10% of the excess return generated where NAV performance is 2% per annum above the FTSE Small Cap ex Investment Companies Index over rolling three-year periods ended 30 June each year, provided that the index has generated a positive return (otherwise the hurdle is 2% per annum). The maximum payable in any one year, including both the management and performance fee, is 1.4% of the NAV – excess amounts are carried forward to future periods. There is a high watermark.

For the year ended 30 June 2020, other expenses included £148,000 for secretarial services, the directors’ fees (detailed on page 22), and other expenses of £611,000, which included £359,000 of costs related to the change in manager.

With the exception of the investment manager’s performance fee, which is charged wholly to capital, all other fees and expenses are charged wholly to revenue.

SEC’s annualised ongoing charges ratio was 1.11% for the year ended 30 June 2020, very marginally higher than the figure for the year ended 30 June 2019 (1.10%).

Capital structure and life

SEC has a simple capital structure with one class of ordinary share in issue. Its ordinary shares have a premium main market listing on the London Stock Exchange and, as at 31 January 2021, SEC had 63,296,844 ordinary shares in issue and admitted to trading and a further 6,562,047 ordinary shares held in treasury.

SEC’s articles permit it to borrow up to 25% of the NAV, but in practice SEC’s portfolio has not been geared and SEC has not had a borrowing facility since July 2012.

SEC does not have a fixed life, but each year shareholders are asked whether they want the trust to continue. At the AGM held on 11 November 2020, 74% of shares voting were cast in favour of continuation. The board has met with several of the company’s major shareholders and says that it will continue to engage with shareholders to seek to address any concerns that have been raised.

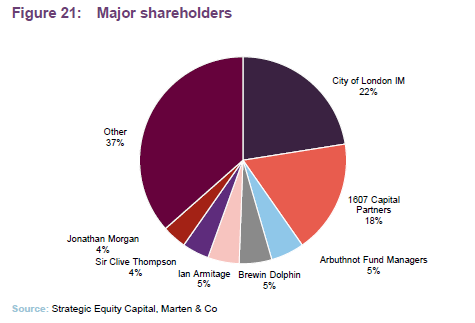

Major shareholders

Recently, RIT Capital Partners sold its stake in the company to City of London Investment Management.

Financial calendar

SEC’s year-end is 30 June. Its annual results are usually released in October (interims in February) and its AGMs are usually held in November of each year.

SEC pays one final dividend in November each year, following shareholder approval at the trust’s AGM.

Management team

In addition to the core team listed below, GHAM has a further seven investment professionals working within its strategic equity team.

Ken Wotton – managing director, Public Equity, lead manager for SEC

Ken is managing director, Public Equity, and leads the investment team managing public equity investments. He is lead manager for LF Gresham House UK Micro Cap Fund, LF Gresham House UK Multi Cap Income Fund and SEC, and manages AIM listed portfolios on behalf of the Baronsmead VCTs. Ken graduated from Brasenose College, Oxford, before qualifying as a Chartered Accountant with KPMG. He was an equity research analyst with Commerzbank and then Evolution Securities prior to spending the past 12 years as a fund manager at Livingbridge and now Gresham House, specialising in smaller companies.

Adam Khanbhai – investment director, fund manager for SEC

Adam joined Gresham House in May 2020, following GHAM’s mandate win of SEC. He has 10 years of relevant financial experience, previously working for GVQIM as a senior analyst and fund manager providing analysis and due diligence on existing and potential investee companies. Prior to this, he worked at OC&C Strategy Consultants for six years as a consultant working on commercial due diligence and strategy projects for corporate and private equity clients.

Adam was a Girdlers’ Scholar at the University of Cambridge and is a CFA charterholder.

Brendan Gulston – investment director, equity funds

Brendan joined Gresham House in November 2018, having previously been at Livingbridge. He studied commerce with a focus on finance at Melbourne University and subsequently spent four and a half years in technology investment banking at Canaccord Genuity.

Richard Staveley – managing director, Strategic Public Equity

Richard entered fund management 20 years ago and is a chartered accountant. After initially starting at a hedge fund, he moved to Société Générale Asset Management where he was made head of UK small companies after becoming a CFA charterholder in 2002.

Richard then became a founding partner of River and Mercantile Asset Management in 2006, responsible for the top quartile performing UK small company and UK income funds and helping grow the business to over £2bn AUM. In 2013 he joined Majedie Asset Management to initially co-manage and then solely run the small companies investments within the flagship UK Equity Service. These investments peaked at over £900m, while overall firm AUM doubled to £15bn during his tenure.

Laurence Hulse – investment manager

Laurence works alongside Richard Staveley in the Strategic Equity team, looking at both public and private equity transactions across a range of sectors for Gresham House Strategic. He also supports fundraising and investment activities for the firm’s real assets division.

Laurence has a Bachelor’s Degree in Politics with Economics from the University of Warwick. During his studies, Laurence interned at Rothschild & Co, working on the Mergers and Acquisitions Team in the industrial sector, and at Barclays Capital on the equities trading floor

Paul Dudley – corporate finance

Paul is responsible for corporate finance in the Strategic Public Equity team at Gresham House and joined in 2020. He was previously at HD Capital Partners (Founder), WH Ireland, Sigma Capital plc and PwC. Paul has over 24 years’ corporate finance experience and holds a BSc in Geography from Durham University.

The investment committee

Anthony (Tony) Dalwood (chair)

Tony has been chief executive officer of Gresham House Plc since December 2014. He chairs the investment committees of Gresham House Plc and Gresham House Strategic Plc. He led the management buy-in and established a new management team that transformed the firm from an investment trust into the AIM listed specialist asset manager it is today.

Tony has a long track record of investing and advising numerous public and private equity businesses. From 2002 to 2011, he established and grew SVG Investment Managers before being asked to lead SVG Advisors (formerly Schroder Ventures, London), the global private equity arm of Schroders, as CEO. He was part of the team managing SEC when it was launched in 2005.

He started his career at Phillips & Drew Fund Management (later UBS Global Asset Management), one of the UK’s most prominent value investment firms with £60bn in AUM at its peak. He was also a member of the UK equity investment committee with responsibility for managing over £1.5bn of UK equities.

Tony has over 25 years of experience and holds a Master of Arts in Management Studies from the University of Cambridge (where he was also a junior rugby international and Blue).

Ken Wotton (see above)

Graham Bird

Graham Bird was one of the founding employees of Gresham House Plc. He left GHAM in December 2019, but remains a member of the investment committee and is a consultant to the strategic public equity team. Graham joined Escape Hunt Group Ltd as its CFO on 6 January 2020 and became a non-executive director of SpaceandPeople Plc around the same time.

Graham is a chartered accountant, having qualified with Deloitte in London, and has worked in advisory, investment, commercial and financial roles. Prior to joining Gresham House, Graham spent six years in senior executive roles at PayPoint Plc, including as director of strategic planning and corporate development and executive chairman and president of PayByPhone. Before joining PayPoint Plc, he was head of strategic investment at SVG Investment Managers, having previously been at JPMorgan Cazenove, where he served as a director in the corporate finance department. Graham holds an MA in Economics from the University of Cambridge.

Bruce Carnegie Brown

Bruce was appointed chairman of Lloyd’s of London, in June 2017 and is also chairman of Moneysupermarket Group and a vice chairman of Banco Santander. He was a non-executive director of JLT Group Plc from 2016 to 2017, prior to which he was non-executive chairman of Aon UK Ltd from 2012 to 2015, senior independent director of Catlin Group Ltd from 2010 to 2014 and chief executive for Marsh UK and Europe from 2003 to 2006.

Bruce was also senior independent director of Close Brothers Group Plc from 2006 to 2014. He previously worked at JP Morgan for 18 years in a number of senior roles and was managing partner of 3i Group Plc’s Quoted Private Equity Division from 2007 to 2009. He is President of the Chartered Management Institute.

Richard Staveley (see above)

Thomas (Tom) Teichman

Thomas has 30 years’ VC & banking experience. He founded Spark in 1995 and was a former investment committee member at Brandt’s, Credit Suisse, Bank of Montreal and Mitsubishi Finance London. He was a start-up investor/director of lastminute.com, mergermarket.com, notonthehighstreet.com, Kobalt Music (chairman), ARC and MAID, amongst others.

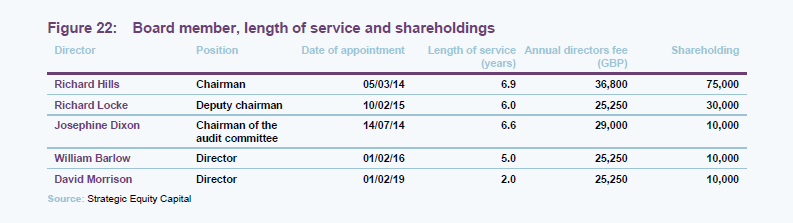

Board

SEC’s board is composed of five members (details of their individual experience are provided below and overleaf); all members are non-executive and considered to be independent of the investment manager. SEC’s directors do not have any other shared directorships.

It is board policy that all board members retire and offer themselves annually for re-election, and that no Director shall serve beyond the 12th AGM following his or her appointment. The board has been refreshed relatively recently, as is clear from Figure 22.

Richard Hills (chairman)

Richard has substantial experience of the investment management industry and has held senior executive and non-executive positions within the fields of both conventional and alternative assets. He is currently a board member of Henderson International Income Trust Plc and EQT Services (UK) Limited.

Richard Locke (deputy chairman)

Richard is vice chairman of Fenchurch Advisory Partners LLP, an independent corporate finance advisory firm that specialises in the financial services sector. Previously he was a partner of Cazenove & Co. and then a director at its successor firm, JPMorgan Cazenove.

Josephine Dixon (chairman of the audit committee)

Josephine is a chartered accountant with a career that spans a number of financial and commercial roles in a variety of sectors, from financial services to football. She has substantial investment trust board experience and is currently on the boards of BB Healthcare Trust Plc, BMO Global Smaller Companies Plc, Alliance Trust Plc, JPMorgan European Investment Trust Plc and Ventus VCT Plc.

William Barlow (director)

William is currently chief executive officer of Majedie Investments Plc, having been a director since 1999. He is a non-executive director of Majedie Asset Management Limited and was previously chief operating officer at Javelin Capital LLP.

William joined Skandia Asset Management Limited as an equity portfolio manager in 1991 and was managing director of DNB Nor Asset Management (UK) Limited. He is also the chairman of Racing Welfare.

David Morrison (director)

David is chairman of Maris Limited, a privately-owned industrial holding company active predominately in East Africa, and was non-executive chairman of Be Heard Group Plc until the beginning of September 2020. Having spent the majority of his career in venture capital, he has been an investor and director of several private and public companies including Record Plc, PayPoint Plc and CPP Group Plc.

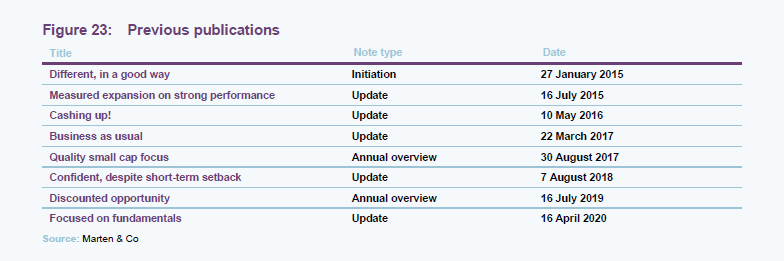

Previous publications

Readers interested in further information about SEC, such as investment process, fees, capital structure, trust life and the board, may wish to read our previous notes (details are provided in Figure 23 below). You can read the notes by clicking on the links in Figure 23 or by visiting our website.

The legal bit

This marketing communication has been prepared for Strategic Equity Capital Trust Plc by Marten & Co (which is authorised and regulated by the Financial Conduct Authority) and is non-independent research as defined under Article 36 of the Commission Delegated Regulation (EU) 2017/565 of 25 April 2016 supplementing the Markets in Financial Instruments Directive (MIFID). It is intended for use by investment professionals as defined in article 19 (5) of the Financial Services Act 2000 (Financial Promotion) Order 2005. Marten & Co is not authorised to give advice to retail clients and, if you are not a professional investor, or in any other way are prohibited or restricted from receiving this information, you should disregard it. The note does not have regard to the specific investment objectives, financial situation and needs of any specific person who may receive it.

The note has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. The analysts who prepared this note are not constrained from dealing ahead of it but, in practice, and in accordance with our internal code of good conduct, will refrain from doing so for the period from which they first obtained the information necessary to prepare the note until one month after the note’s publication. Nevertheless, they may have an interest in any of the securities mentioned within this note.

This note has been compiled from publicly available information. This note is not directed at any person in any jurisdiction where (by reason of that person’s nationality, residence or otherwise) the publication or availability of this note is prohibited.

Accuracy of Content: Whilst Marten & Co uses reasonable efforts to obtain information from sources which we believe to be reliable and to ensure that the information in this note is up to date and accurate, we make no representation or warranty that the information contained in this note is accurate, reliable or complete. The information contained in this note is provided by Marten & Co for personal use and information purposes generally. You are solely liable for any use you may make of this information. The information is inherently subject to change without notice and may become outdated. You, therefore, should verify any information obtained from this note before you use it.

No Advice: Nothing contained in this note constitutes or should be construed to constitute investment, legal, tax or other advice.

No Representation or Warranty: No representation, warranty or guarantee of any kind, express or implied is given by Marten & Co in respect of any information contained on this note.

Exclusion of Liability: To the fullest extent allowed by law, Marten & Co shall not be liable for any direct or indirect losses, damages, costs or expenses incurred or suffered by you arising out or in connection with the access to, use of or reliance on any information contained on this note. In no circumstance shall Marten & Co and its employees have any liability for consequential or special damages.

Governing Law and Jurisdiction: These terms and conditions and all matters connected with them, are governed by the laws of England and Wales and shall be subject to the exclusive jurisdiction of the English courts. If you access this note from outside the UK, you are responsible for ensuring compliance with any local laws relating to access.

No information contained in this note shall form the basis of, or be relied upon in connection with, any offer or commitment whatsoever in any jurisdiction.

Investment Performance Information: Please remember that past performance is not necessarily a guide to the future and that the value of shares and the income from them can go down as well as up. Exchange rates may also cause the value of underlying overseas investments to go down as well as up. Marten & Co may write on companies that use gearing in a number of forms that can increase volatility and, in some cases, to a complete loss of an investment.