Boxing clever

The COVID-19 pandemic has accelerated trends in online retailing, to the benefit of the European logistics market, in which Tritax EuroBox (EBOX) is a leading player. Demand for logistics space is growing rapidly, while supply of existing and new property is dwindling. This supply-demand imbalance is even more acute in prime locations close to heavily populated areas, where sustained rental growth is forecast.

EBOX has amassed a portfolio of big box (very large warehouse) facilities located in major logistics hotspots across Europe. Numerous opportunities to add value also exist within the portfolio, including development and asset management projects. One of the key differentiators of EBOX to its peers is its exclusive relationships with established logistics developers. Through the tie ups, EBOX has access to and first right of refusal over a pipeline of development assets worth €2bn.

Big box logistics in Europe

EBOX invests in a portfolio of logistics assets in continental Europe, diversified by geography and tenant, targeting well-located assets in established distribution hubs, within or close to densely populated areas. The strategy aims to capture market rental value growth and deliver an attractive capital return and secure income. EBOX is targeting a total return of 9% per annum over the medium term.

| wdt_ID | Year ended | Share price total return (%) | NAV total return (%) | EPRA earnings per share (€ȼ) | Dividend per share (€ȼ) |

|---|---|---|---|---|---|

| 1 | 30 Sep 2019 | -6.50 | 2.80 | 2.96 | 3.40 |

| 2 | 30 Sep 2020 | -4.60 | 10.00 | - | 4.40 |

Fund profile

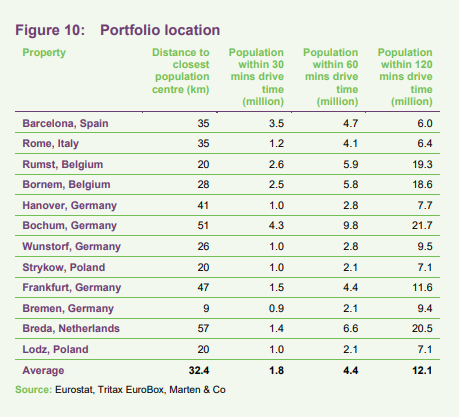

Tritax EuroBox (EBOX) was launched on 9 July 2018 after raising gross proceeds of €339.3m (£300m) in an initial public offering (IPO). Following full deployment of the capital from the IPO into a portfolio of nine continental European logistics real estate assets, the company successfully raised additional gross proceeds of €135m (£119.1m) in a placing on 21 May 2019. It now has a portfolio of 12 assets in six countries, with 21 tenants, worth £819.4m, at 31 March 2020.

EBOX invests in and manages a portfolio of logistics assets in continental Europe, diversified by geography and tenant, targeting well-located assets in established distribution hubs close to densely populated areas. The strategy aims to capture market rental value growth, which is becoming evident in the key distribution markets of continental Europe.

EBOX’s shares are traded on the premium segment of the London Stock Exchange, with both a sterling and euro quotation, and in June 2019 was included in the FTSE All Share Index. To enhance equity returns the company uses gearing (borrowing), with a medium-term target of 45% of gross assets and a maximum limit of 50%.

The manager – Tritax Management

The company’s manager is Tritax Management, part of the Tritax Group. Since 1995, the Tritax Group has acquired and developed around £6bn of commercial property assets across multiple sectors including big box logistics assets, industrial properties, office, retail and hotels.

Tritax Group manages just over £5bn of assets (including EBOX), consisting of more than 43m sq ft of assets. Tritax has a particular specialisation in the acquisition and management of logistics portfolios, most notably through Tritax Big Box REIT, a UK FTSE 250 real estate investment trust (REIT) launched in December 2013. Tritax is headquartered in London with over 30 professionals and is authorised and regulated by the FCA.

Key investment points

- EBOX’s investment proposition centres on the rental growth prospects in the prime European logistics markets in which it operates. Even before the COVID-19 pandemic, online retailing had been rapidly growing. This trend has been accelerated in 2020 and is expected to result in exponential growth in demand for logistics space from online retailers, and thus rental growth.

- The manager is keen to grow the portfolio through acquisitions and provide further diversification in geography and tenant. It has a pipeline worth around €2bn through exclusive relationships with two development partners.

- EBOX’s existing portfolio has several asset management opportunities, through development and new lettings, that would add significant value.

- The group has the potential to achieve an investment grade rating that would lower the cost of debt and give it access to the bond market.

European logistics – COVID accelerating trends

The COVID-19 pandemic saw many European countries respond with some form of lockdown to stem the spread of the virus. As has been the case in the UK, consumer spending on the continent moved from physical retail to online with all but essential retail closed. The momentum to online spending had been building over many years, especially among younger people, but was forced upon a new cohort of the population. These new spending habits are expected to stick, with real estate consultant Savills and the Centre for Retail Research (CRR) predicting that the ‘COVID-19 impact’ will accelerate the online retail sales growth trajectory in Europe by one year.

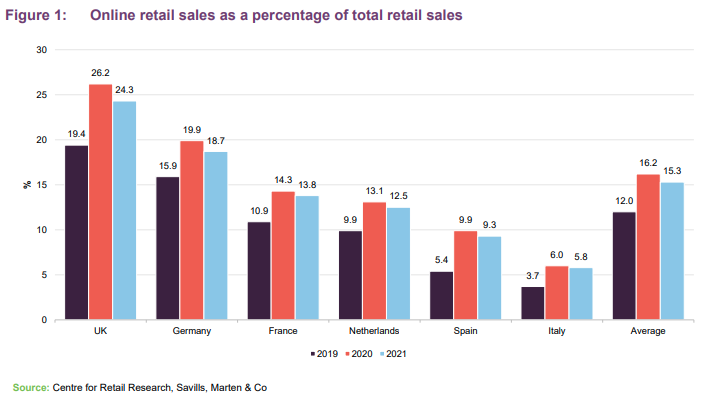

Prior to COVID-19, average online retail sales as a percentage of total retail sales in Western Europe was forecast to reach 15.3% by 2022. However, the CRR now forecasts that this level will now be reached by 2021.

Figure 1 shows that online retail sales as a percentage of total sales are forecast to rise from 12% in 2019 to 16.2% this year, and ease back to 15.3% during 2021 when shops reopen, and consumers return to the high street.

Spain and Italy are expected to see the biggest rise. Both countries had a lower base of online sales, but are expected to increase to 9.3% and 5.8% respectively in 2021. Previous Savills research has found that an online penetration rate of 10.7% in the UK market saw a marked increase in logistics demand, and this is expected to be the case in other European markets too.

Aside from ecommerce, another source of demand has come from occupiers looking to strengthen their supply chain resilience in the wake of the COVID-19 pandemic. Travel restrictions meant supply chains from the Far East were cut off almost overnight. The delays in getting goods to Europe meant production was seriously hampered. A re-think of supply chains has seen an uptick in ‘reshoring’ production facilities to Europe and increasing inventory capacity to deal with shocks.

Europe vs UK

The continental European logistics market has many different characteristics to the UK market. Many European markets are not as mature as the UK, with the explosion in online retail sales yet to fully take place in most markets. Even the mature markets like Germany, France and the Netherlands are some way behind what has been witnessed in the UK.

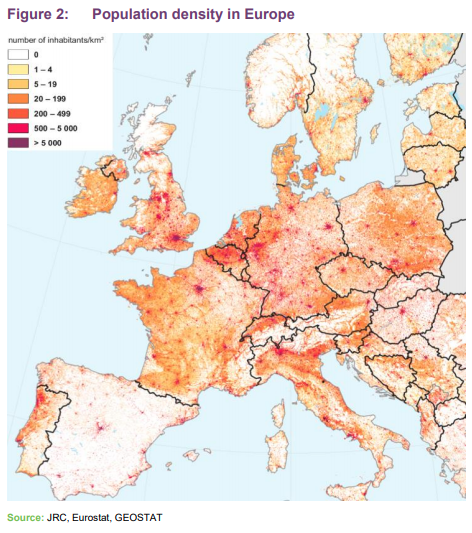

The manager says that asset location is an even more critical element of the investment strategy in continental Europe than in the UK due to the geography of the continent. Whereas in the UK, logistics assets located in the Midlands can reach a significant population of the country in the permitted drive time, in Europe this is not feasible. Large population clusters, as shown in Figure 2, need to be serviced by logistics warehouses on the outskirts of the conurbation, within a 30-minute drive time of the city centre.

The manager says that London and Paris are the only markets in Europe that require true ‘last-mile’ logistics properties (smaller hubs that serve the final stage of delivery) due to their size and infrastructure. For other cities across Europe, large, sophisticated logistics units located on the edge of cities can act as the final touch point for goods on the way to their destination.

Unlike in the UK, leasing contracts on commercial real estate in Europe include annual indexation as standard. This gives property owners protection against inflation. The indexation is sometimes agreed with a cap and collar in place – an upper and lower limit on the rental uplift.

Financing costs in Europe are significantly cheaper than in the UK, meaning the yield spread (the difference between the investment yield and the financing cost) can be much more favourable in Europe.

Demand and supply

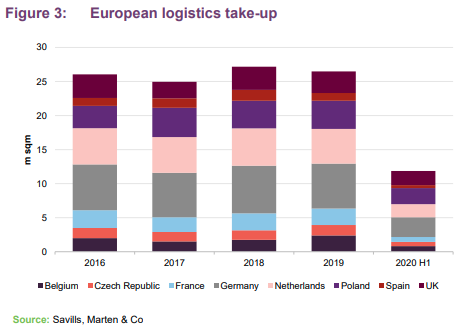

Take-up of logistics space in Europe reached 12.2m sqm in the first half of 2020, according to Savills, which is slightly below the five-year, half-year average. This was largely due to the inability to conduct viewings and sign leases during the second quarter because of government lockdowns.

The UK has seen a big rise in take-up in the first half of the year, the majority of which is attributed to online retailers, with Amazon alone accounting for 36% of the total. This trend is expected to follow in European markets in the second half of 2020, as restrictions are eased, and into 2021.

On the supply side, average European vacancy rates stood at 5.8% at the halfway point of 2020, according to Savills, which is low by historical standards and well below the 12% level that has been observed to have resulted in stable rental growth in the UK. Prime locations near to big cities have the tightest level of supply. The most undersupplied market is Barcelona with a 4.0% vacancy rate.

This shortage of available space is expected to continue for a number of years, with the level of new speculative developments (developments with no tenant signed up) limited. Developer caution is likely to hold back the start of any speculative projects until there is more visibility on the economic impact of COVID-19.

From a development point of view, it is particularly hard to gain planning permission for new projects in Germany and the Netherlands. EBOX’s manager says that strict controls are in place across parts of Germany and the Netherlands that limit new development of logistics property.

Upward pressure on rents

The holy grail for property investors is increased demand and depressed supply. This tension leads to rental growth. That is revealing itself across many European markets, EBOX’s manager says. In the six-month period from October 2019 to March 2020, the estimated rent value (ERV – the estimated annual market rental value of lettable space as determined by a property valuer) of EBOX’s portfolio increased by 3%.

According to Savills, the European markets that saw the greatest rental growth in the first half of this year were Hamburg (+7%) and Frankfurt (+3%). As mentioned earlier, logistics assets that are located close to big urban areas and can fulfil the ‘last-mile’ part of the delivery have seen and are anticipated to continue to see positive rental growth. Demand and supply dynamics are particularly acute in these locations.

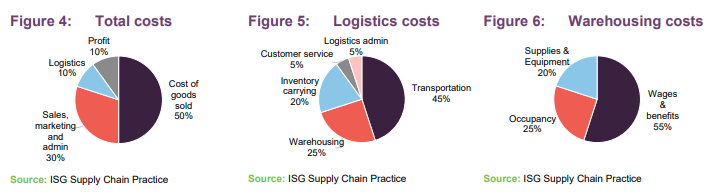

The cost of logistics real estate is a small component of total business costs for the occupier, representing just 0.625% of total costs on average, as shown in Figures 4, 5 and 6 (25% of warehousing costs, which in turn are 25% of logistics costs, which are 10% of total costs). What is far more critical to the business in its logistics costs is transportation. Transportation costs exponentially increase the further occupiers are from the final delivery point. EBOX’s manager says that occupiers – especially retailers – run complicated algorithms to try to optimise the location of their logistics facilities to be as close as possible to cities and infrastructure. They are, therefore, willing to pay more on rent to be in the prime location.

The numbers shown in Figures 4, 5 and 6 are industry standard metrics and it should be noted that different types of occupiers will have different cost pressures.

Investment market

Investment transactions totalled €13.3bn in Europe in the first half of the year, which is 8% down on the same period in 2019, according to Savills. This was mainly due to a lack of investment stock in the market constraining investment volumes, as well as travel restrictions limiting viewings.

Germany was the most active market, with more than €3bn transacted – 12% ahead of the same period in 2019, followed by the UK (€2.8bn) and France (€2.1bn). Poland and the Netherlands recorded particularly strong increases year-on-year at 171% and 23% respectively.

Valuable relationships with developers

EBOX has exclusive partnerships with two specialist logistics developers and asset managers – Dietz AG and Logistics Capital Partners (LCP) – that offer it asset management expertise on its current portfolio and access to their respective development pipelines. EBOX has first right of refusal over the two developers’ pipelines, providing it with acquisition opportunities approaching €2bn across continental Europe.

Not only do these partnerships provide EBOX with access to a significant quantum of the best quality assets in Europe, but they can also purchase them at competitive prices.

Developers are risk-averse and like to sell assets before construction has started, rather than taking them to market, because it provides them with certainty of transaction, allowing them to recycle capital into other projects.

Three of EBOX’s 12 assets have been acquired from the two developers, with a further two purchases introduced to EBOX by the companies.

Both Dietz and LCP also provide asset management services on all EBOX’s portfolio. The companies have substantial teams in all of the countries that EBOX operates, with a fundamental understanding of the local markets, knowledge of occupier requirements and relationships with local municipalities. The scale and quality of the two developers are explained below.

Dietz AG

Dietz is focused on the German logistics market and is one of the biggest developers in Germany. It has more than 40 years of experience covering a wide range of services including development and asset management.

Germany has historically been the most difficult market for overseas investors to penetrate. Partnering with Dietz allows EBOX to grow in the highly sought-after and competitive German logistics market.

Dietz has assets under management of around €1.3bn, comprising 81 properties across Germany totalling a rental area of 1.9m sqm. Tenant relationships include Daimler AG, Deutsche Post Immobilien, Hermes, FedEx, DHL, VolkswagenLogistics, BMW, Kuehne & Nagel, Siemens and REWE.

Under the terms of the agreement, Dietz retains a 10% non-controlling, dormant investment in the assets that it sells to EBOX.

Logistics Capital Partners

LCP is an established pan-European provider of project development and asset management services for logistics real estate, with offices in the UK, the Netherlands, France, Belgium, Italy, Spain and Luxembourg, employing 18 staff.

LCP’s partnership team has extensive experience in the investment, development and occupier sectors of the logistics market. LCP exclusively controls around 60 hectares of land in Europe with 55,000 sqm currently under construction and an active pipeline of standing investment opportunities totalling several hundred million euros in asset value.

Investment process

EBOX focuses on investment in properties fulfilling a key part of the logistics and distribution supply chain for occupiers including retailers, manufacturers and third-party logistics operators (3PLs). Its portfolio is predominantly made up of large, modern distribution warehouses, with some exposure to urban distribution hubs, which help occupiers fulfil the ‘last mile’ part of the distribution chain.

EBOX has a ‘bottom-up’ approach to investment, focusing on good real estate in good locations with limited supply and strong occupational demand. The company targets and maintains a weighted average unexpired lease term (WAULT) of more than five years across the portfolio.

The majority of the company’s portfolio is currently invested in completed, let investments and pre-let income-producing forward funded developments; however, a proportion of the portfolio may be invested in land zoned for logistics use (and options over such land). These types of acquisition allow the group to source higher-quality, lower-priced assets than could be found in the investment market. It allows the company to enter into earlier stage discussions with developers and prospective occupiers, thereby minimising competition with other investment buyers.

EBOX categorises its investments into four investment pillars:

- Foundation Assets are core low-risk income assets. They typically benefit from long leases to institutional grade covenants in prime locations with index-linked rents, providing the foundation to the portfolio.

- Value Add Assets provide asset management opportunities. These assets are fundamentally strong assets let on shorter leases to financially strong tenants allowing implementation of asset management initiatives to drive value, for example by lease renegotiation or building extension.

- Growth Covenant Assets are fundamentally strong assets in good locations but let to tenants with improving financial covenants. These assets offer the opportunity to add value as the tenant’s financial standing improves and hence improving income security.

- Strategic Land assets are investments in land zoned for logistics use in strong locations and include options over land. These assets offer the opportunity to add value as they are positioned at an earlier stage of the development cycle and so have the potential to become Foundation Assets for the future.

On a long-term fully-invested and geared basis, the company expects:

- approximately 50% of its gross assets to be invested in Foundation Assets;

- 20% of gross assets to be invested in Value-Add Assets;

- 20% of gross assets to be invested in Growth Covenant Assets; and

- 10% of gross assets to be invested in Strategic Land (including options over land and assets benefitting from rental guarantees).

Sustainability

EBOX’s environmental, social and governance (ESG) policy sets out the group’s approach to managing sustainability from acquisition, development and asset management. The group has recruited a sustainability lead to develop a long-term strategy, which will be published shortly, and improve sustainability performance.

The large, modern warehouses that EBOX invests in are designed to mitigate their impact on the environment, and, unlike other property classes, such as offices, have lower obsolescence and running costs. EBOX works closely with its tenants to undertake environmental initiatives that improve the efficiency of the buildings. Examples include the generation of renewable energy through photovoltaic panels at four of the group’s assets; LED lighting at 80% of the portfolio; electric car charging stations; solar carport for power generation, and energy controlling.

EBOX’s social approach focuses on positive relationships with occupiers and providing an environment that encourages employee wellbeing, including introducing nature and wellbeing measures at 64% of sites. The group’s local community investment fund supports its tenants’ community engagement initiatives.

Internally, the manager has policies covering equal opportunities, disability discrimination, health and safety, data-protection and whistle-blowing.

Asset allocation

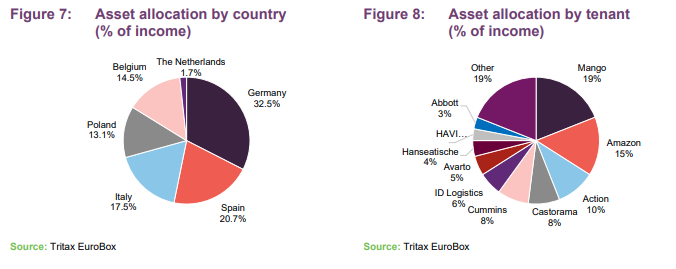

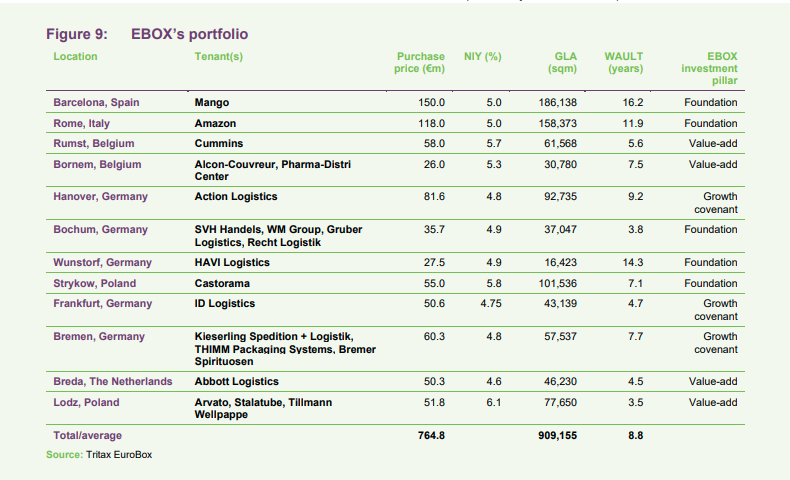

EBOX has a portfolio of 12 assets worth €819.4m located across six European countries. The portfolio has a WAULT of 8.8 years, with a spread of short- and long-term leases, let to 21 tenants. The majority of leases are inflation-linked (71%), with a further 23% with fixed annual uplifts and just 6% with no uplifts.

The assets are all located close to major conurbations across Europe. Figure 10 shows the distance to the closest cities and the population reach of each asset.

Many of the assets have expansion and development opportunities, as well as leasing potential, details of which are listed below.

Barcelona

Purpose-built in 2016, the property is the global distribution centre for fashion retailer Mango. It is located 25km north of Barcelona and is directly accessible from the motorway network, with Barcelona’s port and airport within a 25-minute drive.

It was acquired in September 2018 for €150m and is the biggest asset in EBOX’s portfolio. The high-specification logistics facility has a gross internal area of 186,138 sqm, a maximum eaves height of 40 metres and multi-level mezzanines. It is let on a 30-year full repairing and insuring (FRI) lease (responsibility for repairing and insuring the property is on the tenant) that commenced on 20 December 2016, with a tenant break option in 2036, 2039 and 2042. The rent is subject to annual upward-only indexation.

EBOX will fund an 88,000 sqm extension on the adjacent plot of land, at a cost of €30.5m. Construction is anticipated to start by June 2021, and on practical completion, targeted for Spring 2023, the extension will be incorporated into Mango’s existing FRI lease. On completion of the extension, the building will total 274,000 sqm, including mezzanine space.

Why does the manager like it? It is located in one of the most supply-constrained logistics markets in Europe, with strong occupier demand. There are no sites available in the greater Barcelona area, due to the landscape, for large-scale logistics development and the manager says there is downside protection in that similar adjacent buildings are leased at higher rents. In the extreme event of the tenant going bust, the property can be sub-divided into up to four units and re-let.

The covenant

Mango accounts for 19% of EBOX’s rental income, as at 31 March 2020, which will grow once the extension has been built. The manager says it has access to Mango’s financial statements and that it has performed strongly during the COVID-19 pandemic, with a 30% growth in online sales offsetting lost sales through enforced store closures.

Two months of rent is held in deposit and EBOX has a bank guarantee for 10 months’ rent, that extends to 24 months if certain covenants are not met.

Rome

Acquired from SEGRO for €118m in October 2018, the 158,000 sqm regional fulfilment centre forms a key part of Amazon’s pan-European network and is strategically located in a prime logistics location 35km north east of Rome, with good rail and airport connectivity.

The high-specification logistics facility was purpose-built in August 2017 and has three levels with a maximum eaves height of 14 metres and a site cover of 35%. The building has benefited from significant capital investment from the tenant.

The property, which is currently Amazon’s only regional fulfilment centre in southern Italy, is let on a 15-year FRI lease that commenced on 7 August 2017, reflecting an unexpired lease term of just under 12 years. At the end of the 15-year lease there are two six-year extension options in favour of the tenant. The majority of the rent is subject to annual indexation.

Why does the manager like it? The location, on the outskirts of Rome, is ideal for parcel delivery into the city centre and an important site for Amazon as it grows its presence in Italy. The manager says Amazon’s operations from the facility have grown 40% per annum. The country has relatively low e-commerce rates and is predicted to be among the fastest-growing online retail penetration rates in Europe.

Rumst

Located in the Brussels/Antwerp corridor in Belgium, the site comprises two modern warehouses with a total gross internal area of 59,000 sqm and an office building of 2,500 sqm. Both buildings are fully let to Cummins NV, part of Cummins Inc., a Fortune 500 corporation, listed on the New York Stock Exchange with a market capitalisation of $32.6bn. Cummins designs, manufactures, distributes and services a broad portfolio of power solutions globally. Together, these buildings represent a principal distribution hub for Cummins in the EMEA region.

There are also two unutilised plots of land, totalling 3.4 hectares that offer attractive development potential for buildings totalling around 16,000 sqm.

Why does the manager like it? The development land is a big value kicker for EBOX, which is in discussions with Cummins about expanding its presence on the site.

Bornem

Comprising two warehouses, the asset has a combined gross internal area of 31,000 sqm. The first building is a multi-let warehouse with two interconnected units let to Alcon-Couvreur NV (a world leader in eye care). A new single lease for the two units expires in nine years.

The second building was vacant on acquisition in 2018, but within four months was let to Belgische Distributiedienst NV, part of the BD myShopi NV group, which acts as guarantor to the lease. The lease was agreed for a nine-year term from 1 July 2019, and the rent compounds annually at 100% of the Belgian Health Index.

There were two plots of land at the Bornem site, totalling 4.5 hectares. EBOX sold the smallest plot, which was too thin for a logistics development, 53% ahead of book value. The other plot, located between the two buildings, is in the process of being developed out by EBOX.

Why does the manager like it? The asset was acquired with significant value-add opportunity, with some of that already realised. The development land could return 7% on construction costs.

Hanover, Peine

The brand new, purpose-built asset was acquired in October 2018 for €81.6m and was the first for EBOX arising from its relationship with Dietz. It is located in an established logistics area close to Hanover and Brunswick, on the A2 motorway, which crosses Germany, linking Berlin to the Rhine/Ruhr region.

The 90,000 sqm property is let to Action Logistics (the logistics arm of discount retailer Action, which is backed by 3i Group) and is classified as a Growth Covenant asset by EBOX. Action has more than 1,500 stores in seven European countries, with sales of over €5.1bn in 2019. The success of the retailer is underpinned by its logistics network.

Why does the manager like it? The area benefits from excellent logistics links and continues to see high occupier demand, a low vacancy rate and limited availability both of logistics buildings and land for development.

Bochum

Acquired in November 2018 for €35.7m, the 37,000 sqm, four-unit asset is strategically located in an established logistics location near Bochum, in the Rhine-Ruhr region of Germany. The area continues to see high occupier demand, a low vacancy rate and limited availability both of logistics buildings and land for development.

The multi-let property was acquired with two of the four units, totalling 17,664 sqm, vacant. Within three months of acquisition EBOX let 9,337 sqm of space to Gruber Logistics (a transportation and logistics service provider in Germany) on a five-year term. The lease is subject to annual consumer price index (CPI) uplifts reflecting 100% of the German Consumer Price Index with a floor of 2%.

The second vacant unit, of 8,335 sqm, was let to Recht Logistik (a German logistics and transportation company) in January 2020 on a five-year term at a rent 7% ahead of previous levels. The rent will be subject to full annual indexation reflecting 100% of the German Consumer Price Index.

The two original tenants are SVH Handels GmbH (a subsidiary of the Würth Group, a worldwide wholesaler to the trade and craft industry, with annual turnover of over €12bn), which has 4.4 years unexpired on its lease, and logistics provider WM Group, which has 2.6 years left on the lease.

Why does the manager like it? The asset could be classified as ‘final mile’ due to its central location. The letting to Recht Logistik demonstrated the rental growth potential of the asset.

Wunstorf

EBOX forward funded the development of this 16,000 sqm urban logistic asset that completed in December 2019. The cold store facility is located 20km from the centre of Hanover and let to HAVI Logistics (a food distributor that supplies fast-food chains across Germany), with security from the parent company, on a 15-year lease.

The asset has a low site coverage of 25%, giving EBOX the opportunity to extend the building by around 10,000 sqm.

Why does the manager like it? The manager expects the development land to come with a yield on cost (return on investment) of 7%. The tenant, HAVI, has expressed an interest in expanding its presence at the site in two to five years’ time.

Skrykow

Located in central Poland and let to Castorama (one of Europe’s leading DIY retailers and part of Kingfisher), this asset was originally constructed in 2017 and expanded to 101,555 sqm in 2019. It is entirely let to Castorama, with an unexpired lease term of eight years, subject to annual upward-only indexation.

Central Poland is an established logistics location that has seen rapid take-up by numerous blue-chip tenants in the last five years, with continuing high tenant demand and a low vacancy rate. The site is strategically located in Strykow, 15km north-east of Lodz, Poland’s third-largest city, which benefits from excellent infrastructure and connectivity to the country’s road, motorway and rail networks.

Why does the manager like it? With strong and growing tenant demand and a constrained supply of available logistics buildings, the asset provides good income growth potential, especially given its current low rental level.

Frankfurt, Hammersbach

Bought for €50.6m in June 2019, the 43,000 sqm property is let to ID Logistics on a 10-year lease term, with breaks at the end of years five and six. The lease is subject to annual upward-only indexation of 100% of German CPI, after year three.

ID Logistics is servicing an Amazon contract from the facility and the asset is classified as a Growth Covenant asset by EBOX by virtue of the fact that Amazon has the option to take over the lease at the fifth year.

The asset is situated in the prime logistics location at Hammersbach, near Frankfurt, which has high occupier demand, a low vacancy rate and limited availability both of logistics buildings and land for development.

Why does the manager like it? With Amazon potentially taking over the lease in 2024, the value of the asset is likely to rise based on improved covenant strength.

Bremen

Located in the prime logistics hub of Bremen, the second-largest metropolitan city in north-west Germany and the largest freight area in the country, the asset comprises two facilities built in 2013 and 2019.

One property is single-let to logistics operator Kieserling Spedition + Logistik on a 10-year lease from February 2019. The second property is multi-let to Kieserling Spedition + Logistik, THIMM Packaging Systems, a leading packaging and logistics company, and Bremer Spirituosen on shorter leases. The WAULT of both properties is 7.7 years, with rent subject to annual indexation of 85% of the German CPI.

The area benefits from excellent road infrastructure as well as national and international transport connections via Bremen International Airport and the high-speed railway network.

Why does the manager like it? The location is severely supply constrained, with no parcels of land left for development nor plans to zone land for logistics development. This has driven recent rental growth. The shorter leases on the second unit give EBOX the opportunity to capture this rental growth.

Breda

Purpose built in November 2019, the 46,185 sqm property is divided into four units and is half let to Abbott Logistics (part of Abbott Laboratories, a medical devices and healthcare company listed on the New York Stock Exchange with a market capitalisation of $150bn) on a 10-year lease term subject to annual indexation of 2.0% per annum. The other two units are vacant, with rental guarantees for 12 months ending December 2020.

It is located in an established logistics location along the main east-west logistics corridor in southern Netherlands.

Why does the manager like it? The asset offers attractive scope for value and income enhancing opportunities, with the company in discussions with two interested parties to let the vacant space.

Lodz, Strykow

The asset, acquired in February 2020, comprises two logistics properties and development land. The first building, of 43,218 sqm, is let to Arvato Polska until January 2025, with a tenant break option in January 2024. Arvato is an international logistics service company and provides international, third-party logistics services for retailer H&M from this building.

The second building is multi-let with 8,942 sqm let until July 2029 to Stalatube (a leading provider of stainless-steel solutions) and 3,287 sqm let to the Polish operations of German packaging company Tillmann Wellpappe until July 2029, with a parent company guarantee. Around 22,000 sqm remains vacant, but benefits from a two-year vendor’s rental guarantee. This reflects a WAULT of five years to expiry (4.5 years to break). All rents are subject to annual upwards only indexation to 100% of local CPI.

An adjacent plot of land capable of accommodating a building of 22,400 sqm exists, with EBOX entered into a funding agreement with the vendor to bring forward development on letting, increasing its investment in the asset by around €15m (at a predetermined yield on cost of 6%).

Why does the manager like it? The asset offers scope for income growth off a low base and value enhancement through identified asset management opportunities, as well as the potential to add value through the development of the land.

COVID impact on rent collection

The COVID-19 pandemic affected the ability of a small number of tenants to pay rent on time. For the April to June 2020 quarter, rent deferments until 2021 had been agreed with four tenants, representing €1.6m, or 15.7% of the quarter’s rent. The amount deferred beyond EBOX’s 2020 financial year end of 30 September 2020 represents 3.9% of its annualised rental income, whilst short-term deferrals represent 2.9% all of which have been repaid. There have been no further requests to defer or waive rent and all previously agreed arrangements have been honoured in full.

Full deployment of available funds – the next steps

EBOX is on the verge of completing a deal to acquire its 13th asset, at which point it would have deployed all available funds. The manager is keen to grow the company, especially given the positive dynamics at play in the logistics sector, and is exploring a number of options. With its share price currently trading at a discount to net asset value (see page 22), an equity raise seems out of the question for now.

One option could be to sell stakes in assets to free capital to buy more properties. This option would not improve its NAV, but would allow it to diversify its portfolio in both country and tenant. As mentioned earlier, EBOX has access to a vast pipeline of assets through its exclusive developer relationships and would be able to deploy capital rapidly.

Performance

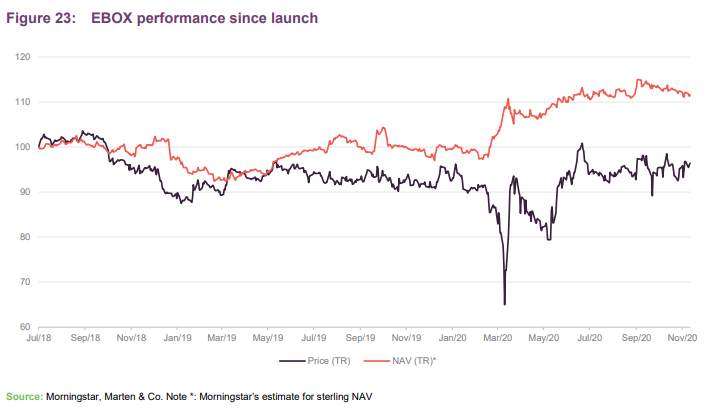

EBOX’s NAV made steady progress from launch as it pieced its portfolio together. Its NAV grew progressively as it deployed the proceeds of an equity raise in May 2019. EBOX’s NAV is quoted in euro, and the NAV in Figure 23 is Morningstar’s estimate for sterling NAV based on the daily exchange rate.

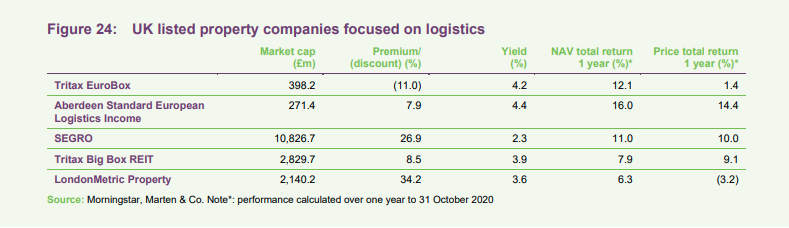

Most property companies investing in European logistics are unlisted funds or subsidiaries of larger groups. The listed peer group we have assembled consists of EBOX’s closest competitor Aberdeen Standard European Logistics Income (ASLI), SEGRO, which owns a mixture of ‘big box’, urban and industrial space, about a third of which is located in continental Europe, Tritax Big Box and LondonMetric Property. The latter two are UK-focused.

EBOX is larger than ASLI, has a similar yield profile, and delivered double-digit NAV total return in the past year. It is trading at a large discount, despite the quality nature of the portfolio and significant growth prospects.

NAV and portfolio valuation

EBOX publishes its NAV twice a year, based on portfolio valuations, which are approved by the board prior to publication.

Independent international real estate consulting firm JLL performs the valuation, in accordance with RICS guidance. Each property is unique, and the fair value includes subjective selection of assumptions, most significantly the estimated rental value and the yield. These key assumptions are impacted by a number of factors including location, quality and condition of the building, tenant credit rating and lease length. Whilst comparable market transactions can provide valuation evidence, the unique nature of each property means that a key factor in the property valuations are the assumptions made by the valuer.

Dividend

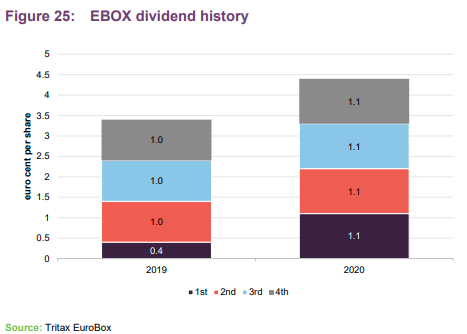

EBOX is one of only a handful of property companies not to cut their dividend during the COVID-19 pandemic, as shown in Figure 25.

EBOX’s quarterly dividend is declared in euros and paid, by default, in sterling (although shareholders can elect to receive dividends in euros). The euro/sterling exchange rate is determined following the dividend declaration. It paid 3.4 euro cents per share in the period from launch to 30 September 2019, equating to 2.986 pence per share. In 2020 financial year, EBOX paid 4.4 euro cents per share in dividends, equating to 3.9256 pence per share, a 31.5% increase year on year.

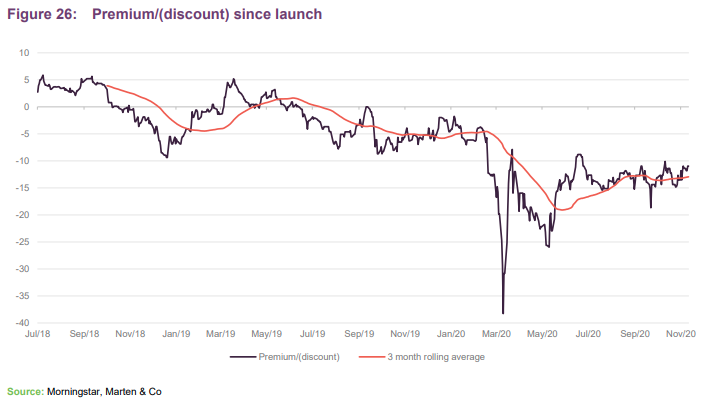

Premium/(discount)

EBOX’s rating had fluctuated between a 5% premium and a 10% discount to NAV for the first 18 months from launch, as it grew its portfolio. When the COVID-19 pandemic hit markets in early March 2020, EBOX’s discount widened to as low as 38% before narrowing considerably. Since April 2020 it has traded at an average discount of 15%, and on 19 November 2020 it was trading at a 11.0% discount.

EBOX has the authority to buy back or issue ordinary shares to address anomalies in the share price performance, if necessary.

In the event that the ordinary shares trade at a discount, EBOX has authority to repurchase up to 10% of its issued share capital. Similarly, should the shares trade at a premium, EBOX has the authority to issue new shares that could be used to satisfy any excess market demand.

Fees and costs

EBOX’s management fees are charged according to the following structure: 1.3% of basic net asset value up to €1bn; 1.15% of basic net asset value between €1bn and €2bn; and 1% of basic net asset value above €2bn. EBOX does not pay a performance fee. In the six months to 31 March 2020, the manager was paid €2.07m (from launch to 30 September 2019: €3.28m).

All costs in relation to core asset management services (which includes fees paid to LCP and Dietz) and property management services are paid by the manager from the management fee.

Administration, secretarial and registrar services

Administrative and accounting services are provided by CBRE. EBOX consolidated both the administration and property management services to CBRE in 2019 on the premise that one supplier using the same software and systems would deliver better operational efficiencies.

Company secretarial services are provided by the manager. The registrar is Computershare Investor Services.

Portfolio valuation services

The portfolio valuation services provided by JLL incurred a fee of €130,400 in the period from launch to 30 September 2019.

Cost ratio

EBOX’s EPRA cost ratio (property and administration costs divided by gross rental income) is currently 30.2%, higher than the typical 15% cost ratio you would expect to see at a REIT operating in one country. EBOX’s multi-country investment strategy means that it has to deal with different legal and tax regimes in different countries – increasing costs.

The EPRA cost ratio is calculated using the IFRS cost ratio, which does not include rental guarantees and licence fees in determining income. Given the nature of EBOX’s portfolio, with predominantly newly-developed assets, some rental guarantees and licence fees are inevitable. With these included the cost ratio falls to 27.5%.

The company’s long-term expectation is that the EPRA cost ratio will fall to the low-20% level. This will be driven by entering into tax-efficient REIT structures such as the one it owns in Italy, on which it pays no tax on income and capital gains. The cost of running the REIT, of around €400,000 per annum, is more than covered by tax savings on the one asset in it (the Amazon-let asset in Rome). As EBOX grows its Italian portfolio, the cost margin will fall further.

Longer-term, EBOX’s EPRA cost ratio will come down as it grows its asset base through the tiered management fee structure.

Capital structure and life

EBOX has a simple capital structure with a single class of ordinary shares in issue and trades on the main market of the London Stock Exchange. As at 19 November 2020, there were 422,727,273 ordinary shares in issue and no shares in treasury.

Gearing

EBOX has an unsecured €425m revolving credit facility (RCF) provided by a group of five lenders (HSBC, BNP Paribas, Bank of America Merrill Lynch, Bank of China and Banco de Sabadell), with a cost of debt of 2.3%. In November 2019, four of the five banks agreed to extend the RCF by one year, resulting in an average maturity of 3.8 years (€100m matures in 2023 and €325m in 2024).

The company has drawn €356.5m against the RCF, resulting in a loan to value (LTV) ratio of 41.8%. This compares with the medium-term target of 45% and the maximum permitted by the company’s investment policy of 50%.

As at 31 March 2020, the company had €37.07m of cash and €68.5m undrawn against the RCF. EBOX’s primary debt covenants relate to LTV (maximum of 65%), interest cover (minimum of 1.5 times) and gearing ratio (maximum of 150%). Interest cover as at 31 March 2020 was 4.95 times (3.45 times as per debt agreement definition) and gearing ratio was 72.5%.

EBOX uses a hedging strategy that includes using interest rate caps to benefit from current low interest rates, while minimising the effect of a significant rise in underlying interest rates. It holds three interest rate caps which hedge €300m of its borrowing, resulting in 84% of debt being subject to interest cap, with a total weighted average interest cap of 0.67%.

Targeting investment grade rating

EBOX aims to achieve an investment grade rating, which would automatically result in the interest rate on its RCF dropping by 30 basis points. Investment grade status would also give it access to the bond market and the US privately placed debt market. Achieving an investment grade rating is mainly driven by size, and the company believes it would match the criteria when it gets to between €1.2bn to €1.3bn gross asset value.

Financial calendar

EBOX’s year-end is 30 September. The annual results are usually released in December (interims in May) and its AGMs are usually held in February of each year. EBOX pays quarterly dividends in March, June, September, and January.

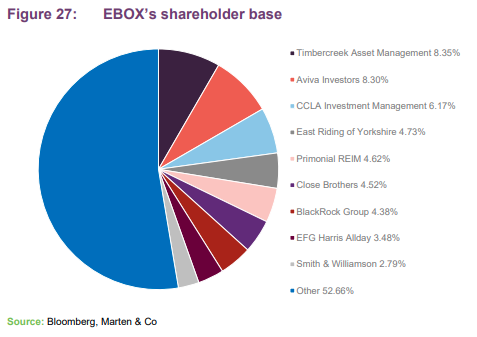

Major shareholders

Management team

The manager has in place an experienced team of investment and asset management specialists. The team has the ability to access off-market transactions in the logistics real estate sector through an extensive and established network across the UK and continental Europe. Key senior personal include:

Nick Preston – fund manager

Nick is the fund manager for the company, with overall responsibility for the provision of investment management and advisory services. He has extensive experience at managing portfolios of commercial real estate across the UK and continental Europe. Before joining Tritax Group in September 2017, Nick worked for Grosvenor Europe in the positions of managing director (Europe) and head of portfolio, responsible for the management of €3.5bn of pan-European assets. Prior to this, he held the position of senior director at CBRE Global Investors, with responsibility for the management of a wide range of portfolios, including separate accounts, pooled funds and fund of funds. Nick also acted on behalf of a major US public pension scheme on a pan-European mandate to invest in logistics assets.

Mehdi Bourassi – finance director

Mehdi joined Tritax Group in May 2019. He is responsible for historical and strategic financial matters in relation to the company, including half-year and year-end reporting, transaction structuring, corporate compliance, budgeting/forecasting, treasury management, monitoring of internal financial controls and the company’s wider capital market activities. Mehdi has 10 years’ experience in pan-European real estate finance roles, most recently at Savills Investment Management as finance manager, focusing on executing real estate transactions across Europe. Previously, he worked as financial controller in real estate at Abu Dhabi Investment Authority (ADIA). He began his career at PricewaterhouseCoopers (PwC) in Luxembourg, conducting audit engagements mainly for real estate and private equity clients. Mehdi holds an MSc in Management from IESEG School of Management and an MBA from London Business School.

James Dunlop

James has overall responsibility for identifying, sourcing and structuring investment assets for the company. He is one of the founding partners of the manager, and became a partner at Tritax Group in 2005. He is responsible for identifying sectors and specific properties, negotiating on approved opportunities and handling the disposal of assets in due course. James read Property Valuation and Finance at City University and qualified as a chartered surveyor in 1991.

Henry Franklin

Henry is responsible for the structuring of the Tritax Group funds, providing general legal counsel and overseeing compliance activities. He is a qualified solicitor who completed his articles with Ashurst in 2001, specialising in taxation and mergers and acquisitions. He also qualified as a chartered tax adviser in 2004 before moving to Fladgate in 2005, where he became a partner in 2007. At Fladgate, Henry specialised in the structuring of commercial property funds. He joined Tritax Group in 2008.

Board

EBOX’s board is comprised of four directors, all of whom are non-executive and considered to be independent of the investment manager. All directors stand for re-election on an annual basis.

Robert Orr (chairman)

Robert is chairman of the group and chairman of the nomination committee. He has extensive board experience at a strategic and operational level in the real estate industry, most significantly as JLL’s European chief executive and currently as a non-executive director of M&G European Property Fund SICAV. He is a qualified chartered surveyor and has an in-depth knowledge of the real estate industry, in particular the European real estate markets. He founded the International Capital Group for JLL in 2005, establishing strong relationships with international investors seeking real estate investment opportunities. Robert is also appointed to the board of APCOA Parking Holdings GmbH, and is a member of the investment advisory committee of EQT Real Estate and a senior adviser to Blue Coast Capital (Lewis Trust Group).

Keith Mansfield

Keith is chairman of the audit committee. He is a chartered accountant with extensive experience of leading significant international transactions. He spent 22 years as partner at PwC, where he developed a specialisation in the real estate industry. He served as regional chairman of PwC in London for seven years. He has previously been a board member of Tarsus Group plc, where he was also chairman of the audit committee, and chairman of Albemarle Fairoaks Airport Limited. Keith is currently a director at Real Time Sports Bingo Limited and Motorpoint Group plc.

Taco de Groot

Taco is chairman of the management engagement committee. He is a chartered surveyor with significant experience in the real estate and investment funds markets. He was a founding partner of M7 Real Estate in the UK, as well as at GPT/Halverton, Heston Real Estate B.V. and Rubens Capital Partners. Taco has also been chief executive of Cortona Holdings BV, based in Amsterdam. He is currently chief executive of Vastned Retail NV, a European retail property company listed on Euronext Amsterdam, but will step down from the role on 1 December 2020. He is also currently a non-executive director of EPP NV, a real estate investment company that operates throughout Poland.

Eva-Lotta Sjöstedt

Eva-Lotta has extensive experience in global retail, supply chain and digital transformation strategy. She has been chief executive of Georg Jensen, a Scandinavian luxury jewellery and home design brand, and Karstadt, a German premium luxury department store chain. She has also held several senior roles over a 10-year period at IKEA including deputy global retail manager, responsible for the development and implementation of IKEA’s global omnichannel strategy, chief executive of IKEA Holland, and deputy retail manager at IKEA Japan. Eva-Lotta is currently a supervisory board member at METRO AG, a leading international wholesale and food service company, and non-executive director of Elisa Corporation, a telecommunications company registered on the Nasdaq Helsinki.

Legal

Marten & Co (which is authorised and regulated by the Financial Conduct Authority) was paid to produce this note on Tritax EuroBox Plc.

This note is for information purposes only and is not intended to encourage the reader to deal in the security or securities mentioned within it.

Marten & Co is not authorised to give advice to retail clients. The research does not have regard to the specific investment objectives financial situation and needs of any specific person who may receive it.

The analysts who prepared this note are not constrained from dealing ahead of it but, in practice, and in accordance with our internal code of good conduct, will refrain from doing so for the period from which they first obtained the information necessary to prepare the note until one month after the note’s publication. Nevertheless, they may have an interest in any of the securities mentioned within this note.

This note has been compiled from publicly available information. This note is not directed at any person in any jurisdiction where (by reason of that person’s nationality, residence or otherwise) the publication or availability of this note is prohibited.

Accuracy of Content: Whilst Marten & Co uses reasonable efforts to obtain information from sources which we believe to be reliable and to ensure that the information in this note is up to date and accurate, we make no representation or warranty that the information contained in this note is accurate, reliable or complete. The information contained in this note is provided by Marten & Co for personal use and information purposes generally. You are solely liable for any use you may make of this information. The information is inherently subject to change without notice and may become outdated. You, therefore, should verify any information obtained from this note before you use it.

No Advice: Nothing contained in this note constitutes or should be construed to constitute investment, legal, tax or other advice.

No Representation or Warranty: No representation, warranty or guarantee of any kind, express or implied is given by Marten & Co in respect of any information contained in this note.

Exclusion of Liability: To the fullest extent allowed by law, Marten & Co shall not be liable for any direct or indirect losses, damages, costs or expenses incurred or suffered by you arising out or in connection with the access to, use of or reliance on any information contained in this note. In no circumstance shall Marten & Co and its employees have any liability for consequential or special damages.

Governing Law and Jurisdiction: These terms and conditions and all matters connected with them, are governed by the laws of England and Wales and shall be subject to the exclusive jurisdiction of the English courts. If you access this note from outside the UK, you are responsible for ensuring compliance with any local laws relating to access.

No information contained in this note shall form the basis of, or be relied upon in connection with, any offer or commitment whatsoever in any jurisdiction.

Investment Performance Information: Please remember that past performance is not necessarily a guide to the future and that the value of shares and the income from them can go down as well as up. Exchange rates may also cause the value of underlying overseas investments to go down as well as up. Marten & Co may write on companies that use gearing in a number of forms that can increase volatility and, in some cases, to a complete loss of an investment.