Strategic Equity Capital – Discounted opportunity

Discounted opportunity

Discounted opportunity

Jeff Harris and Adam Khanbhai have been managing Strategic Equity Capital’s (SEC’s) portfolio jointly since February 2017. Since this time, NAV growth has been solid (a total return of 14.3%, which is broadly in line with the MSCI UK Small Cap Index’s return of 14.1%) but SEC has strongly outperformed during the last year, returning 2.3%, while the index fell 5.8%. Despite this, SEC’s discount to NAV has remained stubbornly wide.

The managers continue to follow their all-weather investment process, maintaining a concentrated portfolio of companies that they believe are high quality, economically resilient and will benefit from long-term structural growth. The managers use private equity-style valuation techniques to identify strategically valuable and covetable assets with undervalued cash flows. M&A has been a significant feature of SEC’s portfolio and, with private equity dry powder at record levels (see pages 5 and 6), the managers see strong potential for takeovers of portfolio companies at marked premiums to their current market values. Irrespective of this, they are confident and optimistic about the prospects for SEC’s underlying holdings and see the above-mentioned discount as a further opportunity for investors.

Focused UK small companies portfolio

SEC aims to achieve absolute returns over a medium-term period, principally through capital growth. SEC is managed with a focused portfolio of investments selected on the same basis that a private equity investor would use to appraise its investments.

| wdt_ID | Year ended | Share price total return (%) | NAV total return (%) | Peer group average NAV TR (%) | MSCI UK Small Cap TR (%) | MSCI UK total return (%) |

|---|---|---|---|---|---|---|

| 1 | 30 Jun 2015 | 48.3 | 25.9 | 14.2 | 15.4 | (0.2) |

| 2 | 30 Jun 2016 | (22.4) | (8.7) | (4.6) | (3.8) | 3.4 |

| 3 | 30 Jun 2017 | 26.1 | 29.7 | 34.9 | 23.5 | 16.7 |

| 4 | 30 Jun 2018 | (1.2) | 1.9 | 13.6 | 14.8 | 8.3 |

| 5 | 30 Jun 2019 | 4.8 | 2.3 | (4.2) | (5.8) | 1.7 |

Fund profile

Launched in 2005, Strategic Equity Capital (SEC) is a London listed investment trust that invests in a concentrated portfolio of predominantly UK-listed equities (typically 15–25 holdings), targeting an internal rate of return (IRR) of at least 15% per annum across the economic cycle.

SEC has been managed by GVQ Investment Management (GVQIM or the managers) and its predecessors since launch (GVQIM was formerly GVO Investment Management and SVG Investment Managers). As at 30 June 2019, GVQIM had assets under management of over £0.5bn. Please see page 21 for more information on the managers.

Private equity style valuation techniques in public markets

GVQIM applies private equity techniques towards evaluating listed companies and seeks to build a portfolio of stocks that it believes are undervalued and would benefit from strategic, operational or management initiatives. Jeff Harris has been the lead manager since 7 February 2017 (having been assistant manager since 2014); alongside Adam Khanbhai, who became the co-manager at this point. The investment process that the managers follow is more fully described on pages 8 to 11.

Before making any investment, GVQIM carries out significant in-house research, aided by a panel of advisers (the Industry Advisory Panel – see pages 23 and 24) and utilising the knowledge and expertise of an extensive network of industrialists and private equity investors.

Independent investment manager

GVQIM’s senior management bought out the business from RIT Capital Partners on 21 December 2017 and the business has been independent since then. RIT Capital Partners retains its stake in SEC and has expressed a desire to remain a long-term holder in the trust.

GVQIM employees own just over 4% of the trust, which helps align their interests with other shareholders. In addition, all five members of SEC’s board have personal investments in the trust (see page 22).

Small cap focused and benchmark agnostic

SEC is overwhelmingly focused on small cap stocks. The managers expect that the majority of its investments will be in the sub-£300m market-cap range at the time of investment, as they believe this under-researched segment (those which are too small for inclusion in the 250 Index) creates greater opportunities to identify mispriced securities. The managers believe that MiFID II has further reduced the availability of research on this part of the market.

The company can invest in companies listed on other recognised exchanges, but this is limited to 20% of gross assets, at the time of investment, and the managers do not expect this to be a significant element of the portfolio. The approach is not constrained by any benchmark, has an absolute return focus and does not employ leverage (debt or otherwise) at the investment trust level.

Manager’s view

As discussed in QuotedData’s previous notes, GVQIM’s outlook is informed by the companies it meets. As a house, it is cognisant of the macroeconomic environment but does not take large macro bets; instead preferring to invest in areas that it believes are positioned to benefit from long-term structural growth areas which can grow through the economic cycle. These include having exposure to the growth in regulation and compliance through Equiniti and Wilmington, diversified pharmaceutical assets such as Clinigen and Alliance Pharma and companies such as EMIS and Medica, which are benefiting from growth in technology in healthcare settings. The managers continue to apply a strong valuation discipline. They seek to avoid companies that are trading on peak multiples and above real-world transaction values.

Slowing global economy

GVQIM observes that the global economy is showing signs of strain: there is a weak macro outlook in major European geographies, particularly Italy and Germany; the US appears to be slowing, with the Fed taking a more dovish stance; Chinese growth is slowing and there are few bright spots in other emerging markets; the US Treasury yield curve has inverted (out to 10 years). A further potential complication is that, in the UK, Brexit compounds larger global macroeconomic and political concerns. However, despite the slowdown, the managers note that there are still many factors that are supportive; for example, historically low unemployment and historically low interest rates. Overall, the managers remain cautious.

Portfolio implications and themes

In this environment, the managers continue to focus on companies with a high degree of revenue visibility, which benefit from long-term structural growth drivers, with strong business models and self-help opportunities. They continue to favour ‘macro-resilient’ sectors and are avoiding cyclically exposed sectors (for example consumer discretionary and banks). Portfolio themes include:

- Diversified pharma – these benefit from demographic changes and a structural trend of increasing demand from healthcare. SEC’s holdings are not dependant on binary outcomes (e.g. Clinical trials results).

- Digital health – structural trend of replacing legacy systems and the provision of remote healthcare to reduce costs and improve outcomes.

- Regulation and compliance – structural trend of an increasing compliance and regulatory burden.

- Pensions and savings – growing complexity and the trend towards self-managed investments.

- Infrastructure and building – increasing demand for family housing as well as connected industrial and logistical space.

Strategically valuable assets

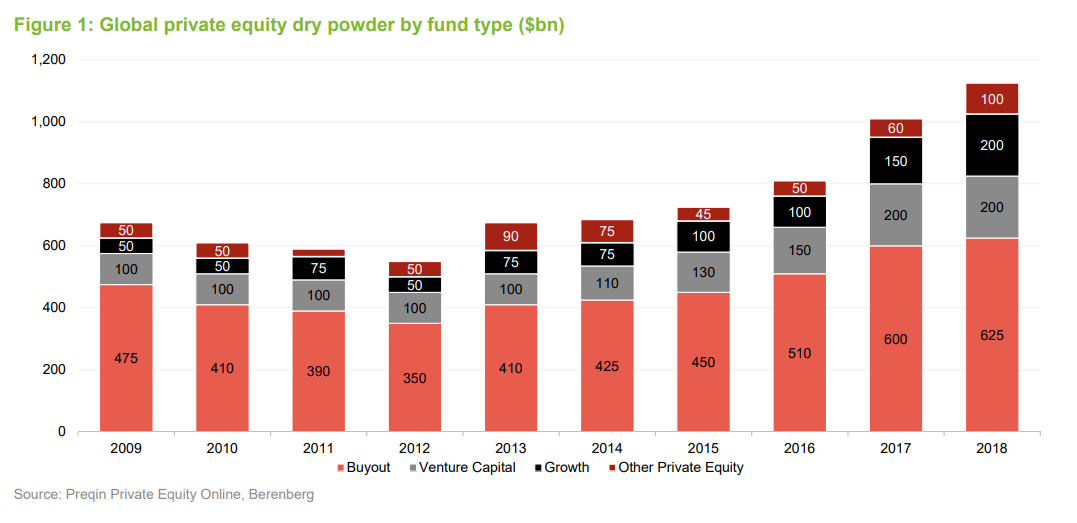

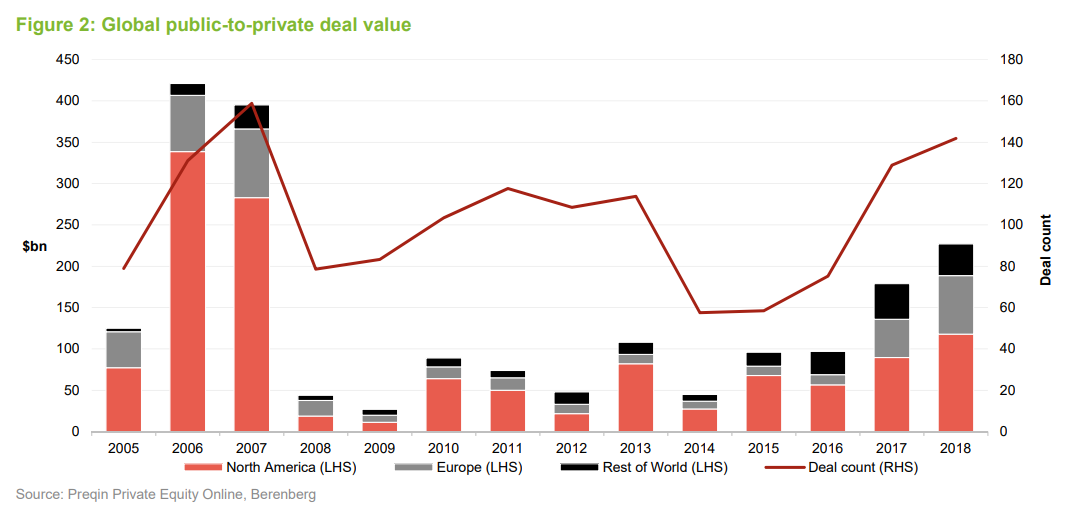

SEC’s managers seek to build a portfolio that consists of strategic and covetable assets with undervalued cash flows. Reflecting this, there is a history of significant M&A (mergers and acquisitions activity) in SEC’s portfolio. As illustrated in Figure 1, global private equity dry powder (cash reserves available for investment) is at its highest level since the global financial crisis and, as illustrated in Figure 2, there has been an upward trend in global private equity deal activity during the last three years that is still way off previous highs. This may suggest there could be still some way to go in the current cycle.

SEC’s managers say that the activity increase is also present in the UK. They say that deal activity has picked up in 2019 with, for example, approaches made for BCA Marketplace, Tarsus, RPC, PTSG, Inmarsat, KCom, Manx, Merlin Entertainment and IFG Group.

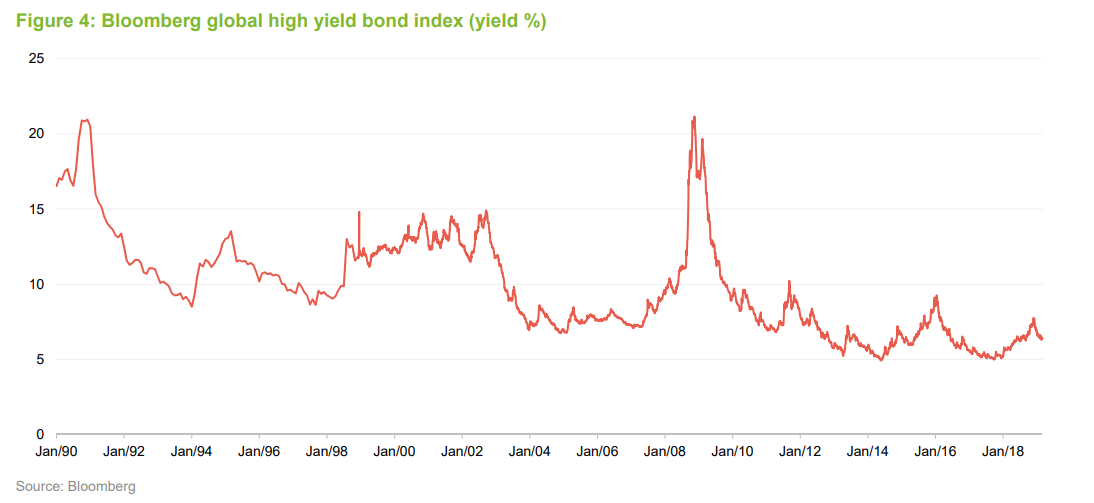

SEC’s managers say that they have long believed the UK is undervalued and alongside record fund raising levels in private equity and generationally cheap levels of debt (see Figure 4), they expect M&A activity to continue. They believe that SEC’s portfolio is well positioned to benefit from this. As illustrated in Figure 3, data from Prequin says that over 50% of investors surveyed view small to mid-market buyouts as presenting the best opportunities in private equity (potentially placing SEC’s portfolio in a sweet spot to receive bids for its holdings).

SEC’s managers say that, where public markets often mis-value companies (for example IFG Group – see page 13 for an illustration), this provides a significant opportunity for its investment process to ascribe ‘real-world’, or buy-out valuations to companies. They caution, however, that there is an ever-present risk of opportunistic M&A at levels below intrinsic value. Nonetheless, they are very confident and optimistic about the prospects for SEC’s underlying holdings.

Brexit

The managers say that whilst the environment is becoming more difficult, recent results and meetings have shown that their underlying holdings are proving resilient and continue to trade well. With regards to Brexit, they say that whilst this will have an impact, it is not a key risk for SEC’s holdings. They continue to hold high-quality differentiated assets on a medium-to-long-term view and are maintaining a balanced international exposure with around 40% of holdings underlying revenues coming from overseas.

Investment process

Summary: private equity style approach to investing

In common with all of its mandates, GVQIM uses a distinct approach to the management of SEC, applying private equity techniques to investing in publicly-traded companies. It operates with a mandate that is unconstrained by any benchmark and aims to deliver superior performance over the medium term.

Key features of the approach are:

- A strong focus on a company’s cash flows, post-maintenance capital expenditure, as the managers say that this gives a fairer indication of a company’s ongoing cash generation;

- Consideration of ‘real world’ multiples. The team (alongside the Industry Advisory Panel, who collectively have been involved in over 350 transactions) believe there is empirical evidence that transaction values provide a better gauge of a company’s fair value and use this in their analysis. This is supported through an in-house leveraged buyout model and forming an opinion of the potential value to a trade buyer (typically operating in the same or a similar industry) or private equity house; and

- Seeking to identify companies that are undervalued but might benefit from strategic, operational or management initiatives.

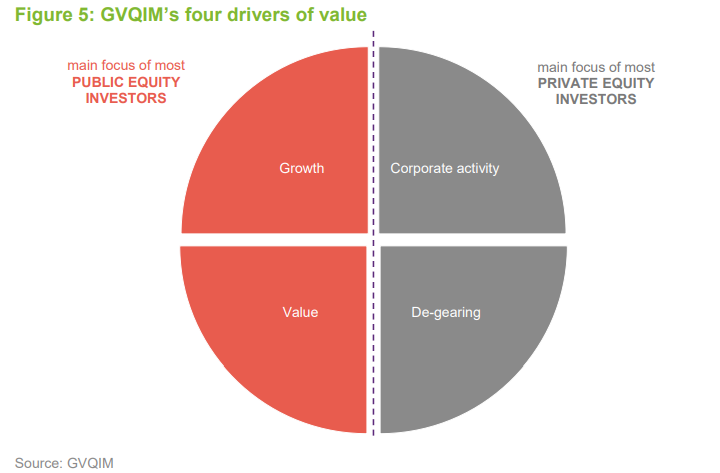

Four key drivers

The managers have a strictly defined process and screen all potential investments using their ‘four drivers’ of equity returns. GVQIM believes that focusing on four routes to creation rather than one in isolation (i.e. ‘growth’ or ‘value’), gives the best chance of achieving target returns over the long term.

GVQIM draws the distinction between the factors on the left-hand side of Figure 5, which reflect the typical focus of investors in listed companies, and the factors on the right-hand side, which are the factors that private equity investors would focus on.

- Growth. GVQIM considers the growth in operating cash flow and prefers structural to cyclical growth. GVQIM favours businesses with the ability to defend their profitability (intellectual property, high barriers to entry, etc.), even in down markets.

- Value. Returns are a function of choosing appropriate entry and exit points and, reflecting this, GVQIM says it maintains a strong pricing discipline based on the appropriateness of the valuation a company is trading at. GVQIM applies a target cash yield (cash on hand as a proportion of market capitalisation) to derive a fair value of a potential investment and the scope for a business to re-rate. It frequently identifies strong candidates for the portfolio but will wait until they’re trading at appropriate valuations before initiating positions. Similarly, whilst GVQIM is happy to run its winners where the target returns meet its hurdle, it will reduce and ultimately sell out of businesses where the shares have re-rated to GVQIM’s target exit level.

- Corporate activity. GVQIM assesses the potential of companies as an acquirer and a target. The team assesses precedent transactions to identify public companies trading at a discount. All portfolio candidates are valued using an in-house leveraged buyout model to form an opinion on the potential value to a trade or private equity buyer. GVQIM seeks to avoid investing in companies with an impediment to being acquired such as a blocking shareholder or a large pension scheme.

- De-gearing: As is common in private equity analysis, GVQIM favours cash-generative businesses. This may be a consequence of the company’s operating model, high margins, efficient working capital and/or low capex requirement. Such businesses can deliver investors returns from the transfer of value from debt to equity, either through de-gearing the balance sheet (reducing the proportion of debt held on the balance sheet), dividends or enhanced returns (buy-backs, special dividends etc.).

Concentrated portfolio

The portfolio is a highly concentrated one and the managers say they want to have the majority of value in 10 to 15 positions. There is a maximum of 15% in any one investment and holdings will typically have a market cap that is too small for inclusion in the FTSE 250 Index (at the time of investment). At any one time, the managers will have an active watchlist that they are considering for inclusion. The managers invest with a rolling three-year time horizon, targeting IRRs of 15% over the economic cycle, and turnover is typically 25-30%. GVQIM develops entry and exit strategies, and a clearly defined route to value creation, prior to initiating an investment and closely monitors its holdings on an ongoing basis.

Cash flow analysis

A key metric in this private equity style appraisal is an analysis of a company’s cash flows – post-maintenance capex (the money a company needs to invest to keep its existing operations ticking over). The managers highlight that, whilst earnings are important, they can be more readily manipulated and that a focus on understanding a company’s cash flow and its sources of cash leakage are key to evaluating its ongoing profitability. For example, they are cautious on companies with unquantified liabilities and significant commitments to defined benefit pension schemes. They also highlight that, whilst important, focusing purely on EBITDA (earnings before interest, tax, depreciation and amortisation) is problematic as this can be boosted in the short term by cutting back on investment, etc. This can not only undermine a company’s future profitability, but can lead to investments in companies that appear to be generating higher margins and trading at cheaper valuations than is actually the case. The managers say that by focusing on cash flows, post-maintenance capex gives a fairer indication of a company’s ongoing cash generation.

Focus on quality

GVQIM’s defines quality as companies with a high degree of intellectual property, high barriers to entry in structurally growing markets with good operating margins and strong cash flow. This has the effect of excluding investment in some areas of the market. The managers avoid businesses that are inherently low margin (e.g. retailers, construction, etc.), and businesses where the primary driver of profitability cannot be influenced by management (e.g. resource companies which are heavily influenced by commodity prices). They avoid businesses in structurally declining markets and those that are overly reliant on a single product, customer, supplier or distributor. Poor accounting systems and deteriorating governance standards are also significant red flags, as are weak cash flows and excessive levels of gearing (debt). GVQIM will not invest in companies that it does not have the expertise to analyse. As such, it will avoid blue sky investments, those that are at an early stage in their life and are yet to generate positive cash flows.

GVQIM considers IPOs but says it is not usually given sufficient notice to perform its lengthy due diligence process and so rarely invests in them (only two have been bought since SEC was launched).

Industry Advisory Panel

All investments are assessed by GVQIM’s Industry Advisory Panel (IAP). The IAP was formed in 2003 and meets monthly to discuss investment candidates in detail. It gives consideration to the quality of a business, its board and whether the members know any of the key individuals, its accounts, whether it is operating at full potential, the strategic and structural challenges it faces, as well as other risks to consider. The IAP is made up of a highly experienced team and the managers consider the IAP to be a very valuable resource that helps them to challenge and further develop investment rationales. They believe this ultimately contributes to superior performance. The composition of the panel is provided on pages 23 and 24.

Engagement

GVQIM believes in constructive engagement; shareholders should not be passive investors, but should engage with the management and directors of the companies that they invest in, on matters of corporate governance and corporate strategy. GVQIM takes a holistic approach to this and its focus is on creating shareholder value for all investors. GVQIM does not seek board representation and prefers to engage in private, after detailed and thoughtful analysis.

Before the managers make an investment, they think about any message they might want to convey to the company. They want to do that from a position of understanding, which is one reason why they put so much emphasis on in-depth research, including conversations with key stakeholders; management; chairmen; senior non-executive directors; brokers; other shareholders; and, sometimes, suppliers and customers. Before they make an investment, GVQIM thinks it is important to establish a good dialogue with the people running the company and other stakeholders to understand their views. One focus with companies in the portfolio has been to encourage them to be more pro-active in building their relationships with existing and potential investors.

Asset allocation

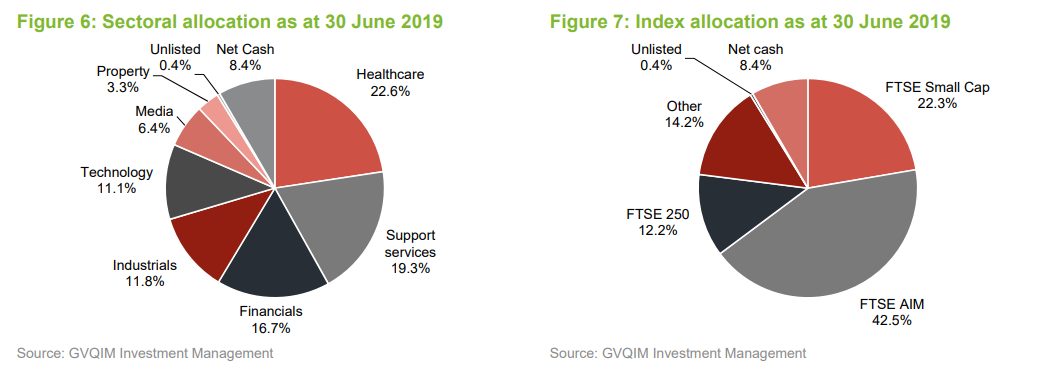

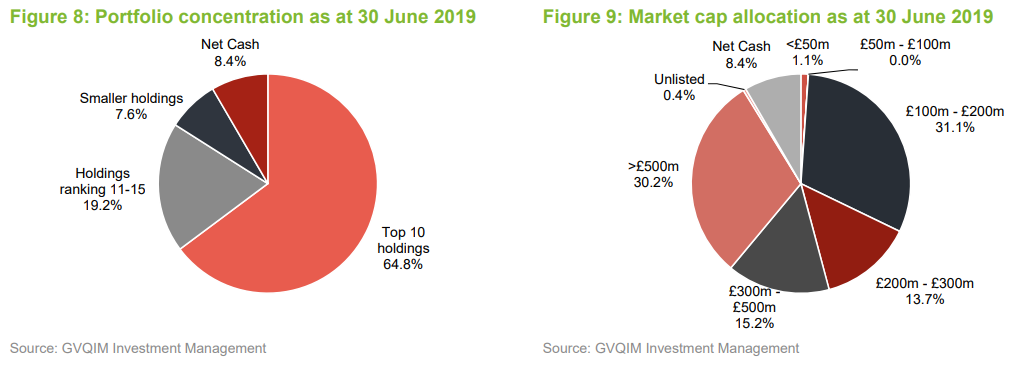

As is illustrated in Figures 8 and 9, SEC maintains a highly concentrated portfolio with a strong focus on smaller companies. This reflects the manager’s long-term strategic view that this part of the market remains under-researched, particularly following the advent of MiFID II, which creates good opportunities for active managers. As is apparent in all of the Figures 6 through 9, SEC maintains a minimal exposure to unquoted stocks as well as a modest cash balance (SEC tends to have a natural cash balance of around 5-15% of net assets).

Figures 6 and 7 show GVQIM’s analysis of the distribution of the portfolio by industry and by index membership. It is noticeable that the portfolio has no exposure to the FTSE 100 index and a modest exposure to the FTSE 250 index. The greatest change since QuotedData last wrote has been a reduction in the allocation to technology, with financials, support services and healthcare all seeing modest increases to compensate.

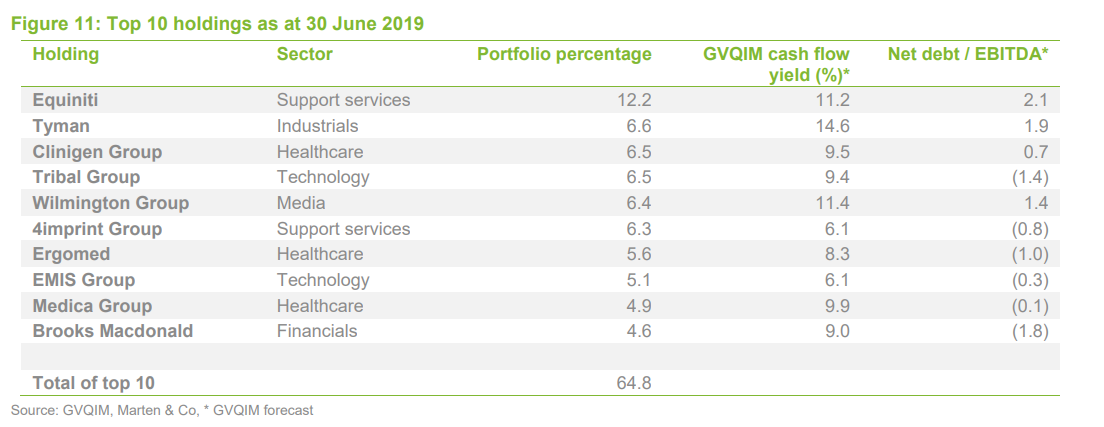

We have included a list of the top 10 holdings in Figure 11. A number of investments have substantial net cash positions. This equates to an aggregate net debt to EBITDA figure for the portfolio close to zero, which compares to about 1.9x for the market as a whole.

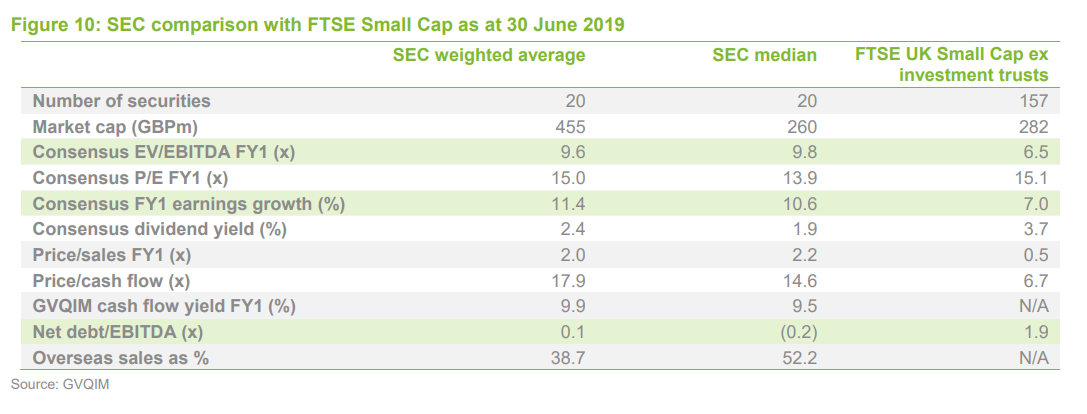

Figure 10, which is based on numbers supplied by GVQIM, shows how SEC’s portfolio compares to the FTSE Small Cap ex-Investment Trusts Index. At the end of June 2019, using a consensus EV/EBITDA multiple, SEC’s holdings were, on average, more expensive than the average company in the index (SEC does not invest in lower valued sectors such as construction, consumer or resource companies) but had significantly stronger balance sheets (lower net debt/EBITDA) and higher growth expectations. As illustrated in both Figures 8 and 11, 64.8% of NAV is in the top ten holdings.

As at 30 June 2019, SEC’s portfolio comprised 20 holdings. This includes a small investment in Vintage 1, an unlisted fund that is advised by GVQIM. SEC has an outstanding commitment of €1,560,000 in relation to the investment in Vintage 1, but the managers have indicated that they do not expect this to be called.

The managers say that SEC’s portfolio has limited exposure to traditional cyclical stocks. As illustrated in Figure 6, SEC’s portfolio has significant exposures to healthcare, services and technology, which do not track the normal economic cycle.

Portfolio activity

Since QuotedData last published, Alliance Pharma and Ergomed have moved up the rankings into the top 10 holdings, replacing Harworth (a real estate company) and IFG Group. Alliance Pharma was discussed in some detail in QuotedData’s August 2018 note (see page 6 of that note). The remaining eight names were all top 10 holdings when QuotedData last published, albeit their rankings have altered slightly. QuotedData’s August 2018 note also provides detailed commentary on IFG Group, Equiniti, Wilmington, 4Imprint, EMIS and Proactis Holdings (as well as commentary on former portfolio companies Goals Soccer and Servelec). Updates on IFG, Proactis, Medica, Ergomed and Dialight (which lay just outside the top 10 at the end of June) are provided below. These represent the more interesting portfolio developments.

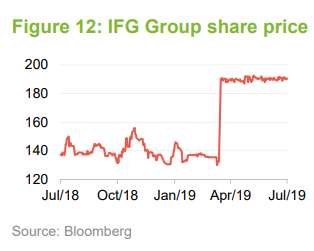

IFG Group – received cash offer from Epiris in March 2019

IFG (www.ifggroup.com) announced a recommended cash offer of £1.93 per share from Epiris on 25 March 2019. As illustrated in Figure 12, IFG’s share price responded very positively to the announcement (up 43.6% on the day). SEC’s managers say that this takeout reflects their strategy. IFG had been a constituent of SEC’s portfolio for four years when the offer was announced. SEC’s managers had a clear thesis for its inclusion. Specifically, they had identified that IFG had two good assets: James Hay and Saunderson House. The managers saw lots of opportunities in both markets, but felt that the assets were combined in an expensive group structure and that it made sense to separate the two businesses over time. However, having identified the strategic value inherent in the company, its realisation was pushed back because of Brexit and the Elysian fund.

Specifically, following the result of the EU referendum, the Bank of England cut interest to bolster the economy and stop it sliding into a downturn. This cut impacted James Hay’s business model and whilst it forced the company to reprice and become more resilient, it made extracting value harder in the short term.

Further to this, James Hay found itself under pressure following the failure of Elysian Fuels. Elysian Fuels was a specialist investment company that put money into biofuel refinery projects. When the fund was marketed, it suggested it could return up to 10 times the original investment over eight years but, in 2015, the value of the scheme was written down to zero and this caused HMRC to question the tax relief claimed by investors who had put Elysian Fuels into their SIPPs. At one point it was suggested that James Hay could have a liability of up to £20m (James Hay said that it had 500 clients who had invested around £55m in the Scheme). This was an impediment to the business being acquired.

There was a potential sale of Saunderson House early in 2018 but, in SEC’s managers’ view, this was announced before sufficient progress had been made and IFG suffered when the deal was aborted. GVQIM reviewed the business and concluded that both issues did not affect the long term quality of the business and its end markets. When new management joined in April 2018, GVQIM had frank discussions with IFG’s board and other shareholders with a view to maximising shareholder value.

A bid eventually came from Epiris (formerly the manager of Electra Private Equity). SEC’s managers say that Epiris made a decent offer (a 46% premium to the closing share price; a trailing PE valuation of 21.4x) and they expect that Epiris could make strong returns in breaking IFG up. However, SEC’s managers are content, particularly as they topped up their positions at far lower share prices in March 2017 and May 2018. IFG was undervalued as a mini-conglomerate but this was difficult to resolve in public markets, may have taken some time to resolve, and involved some execution risk.

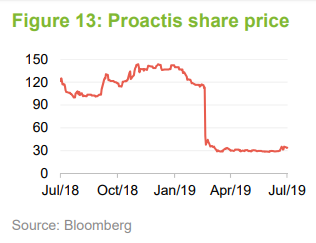

Proactis – profit warning has driven out two large institutional holders

Proactis (www.proactis.com) is a global provider of cloud-based e-procurement and spend control software. The company completed the acquisition of Perfect Commerce in July 2017 in what was supposed to be a large transformative deal. However, the quality of the asset has been significantly lower than was expected by both Proactis’s management and SEC’s managers. Customer retention has been significantly lower than expected and the conversion of pipeline opportunities was also low.

Ultimately, this led to the CEO’s departure in January 2019 and, following this, the company issued a profit warning on 12 February (profits down around 30%, to which the share price reacted very negatively – down 55.8% on the day). SEC’s managers say that this was amplified by liquidity and concerns regarding the strength of the company’s balance sheet (two large institutional holders sold out).

SEC’s managers say that, despite the issues with the acquisition, the original business continues to perform well and has good retention. However, there is still a question of how much value remains in the acquired business. SEC’s managers say that it was cheap (trading at around 5x F12m earnings) and while they think there is considerable upside potential, there is considerable risk and so they have not added materially to the position. However, they say that, once Proactis has stabilised the acquired business, it could become an M&A target.

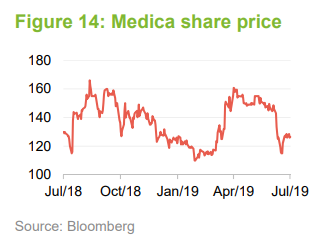

Medica – new CEO expected to grow the business through good strategic acquisitions

In QuotedData’s August 2017 annual overview note, it was highlighted that SEC had participated in the Medica IPO (this being the second time that SEC has participated in an IPO since its launch – see pages 10 and 11 of QuotedData’s August 2017 note). To recap, Medica (www.medicagroup.co.uk) is a leading UK provider of teleradiology services which is the remote interpretation of scans by NHS qualified radiologists. Scanning volumes are increasing by 8–10% per year in part thanks to an ageing population and changes to NICE guidelines that require more scans to be performed. Medica has some 350 radiologists working for them remotely.

In the UK, there is a shortage of radiologists and hospitals are underfunded. This creates a backlog in scan interpretation, which can be outsourced to Medica. Medica also provides an out-of-hours service, which saves NHS trusts money as they do not have to pay for radiologists to work through the night. SEC’s managers say that the business continues to grow very strongly and is highly cash-generative. It is expanding internationally (there is also a shortage of radiologists overseas), which it is able to achieve readily as its business has low capex requirements (server space can be easily expanded in the cloud and adding a new radiologist requires a new pc). According to SEC’s managers, Medica has now de-geared and most profits are going to cash. They think that Medica offers strategic optionality. It has net cash on its balance sheet and a new CEO, joining the company in September 2019, comes from a private equity background (Dr Stuart Quin). Medica is the market leader in the UK but SEC’s managers see strong opportunities in other geographies (for example Australia and New Zealand). They believe Medica is exposed to a structural growth trend; their service both reduces costs and improves patient safety.

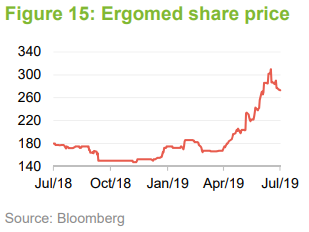

Ergomed – two quality business operating in very good market places

Ergomed (www.ergomedplc.com) describes itself as a mid-sized clinical development organisation. SEC initiated a position in early 2018 and has been topping up opportunistically since (SEC holds circa 7% of the company). Historically, there have been two sides to the business – products and services. The company focused heavily on the products side, in which it partnered with companies to undertake drug development in return for a share of future drug sales. However, SEC’s managers felt that Ergomed’s management should have been focusing on the services side of the business. In their view, products may have high potential upside but are high-risk and returns have proven to be low. In contrast, clinical trial services benefit from a number of structural growth drivers. For example, global pharma is increasingly outsourcing to clinical trial related services and there is considerable consolidation taking place in the CRO (clinical research organisation) space.

The catalyst to invest was the company embarking on a new strategy to focus more on the services side of the business and stop investing in co-development of products. SEC’s managers believe Ergomed has two structural growth businesses in pharmacovigilance and clinical trial services. These are benefitting from an increase in pharmaceutical companies outsourcing to specialists and growing regulatory requirements.

The share price was weaker over the summer last year as there were some delays in on-boarding clients. The managers felt this related to the larger size of these new clients and increased their position. SEC’s managers say that trading to date has been encouraging, with the company upgrading earnings in May. The executive chairman and new CFO purchased around £850k shares between them in June. SEC’s managers believe that while the company is attractive as a listed company, it could be involved in the increasing consolidation in the pharmaceuticals services industry.

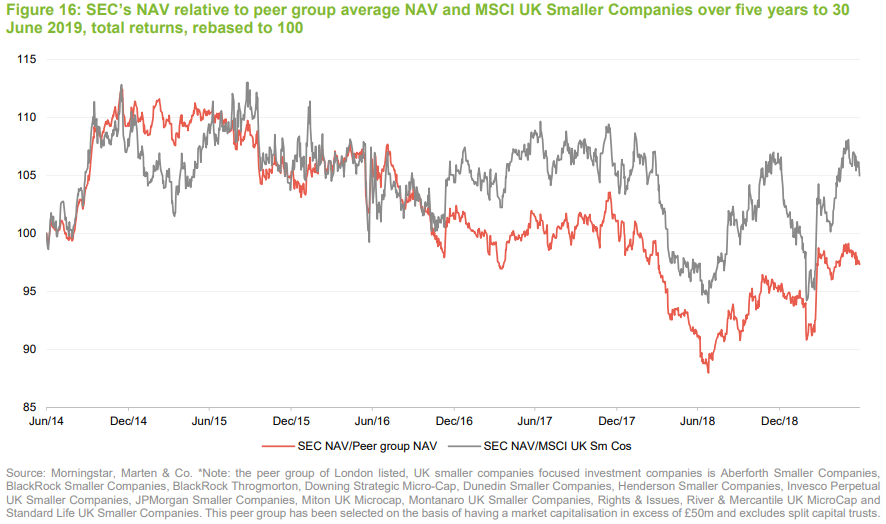

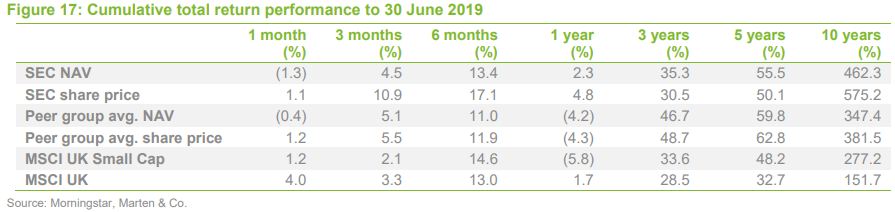

Performance

As illustrated in Figures 16 and 17, SEC has, over the five years to the end of May 2019, outperformed the MSCI UK Smaller Companies Index, the MSCI UK Index and both the peer group average NAV and share price. As discussed in QuotedData’s last note, the second quarter of 2018 was relatively weak, reflecting some of the stock specific issues (see pages 7 and 8 of that note) and the last quarter of 2018 was a difficult period for markets in general. However, year to date, SEC has benefitted as markets have rebounded strongly.

SEC’s ‘private equity’ approach results in it having a highly-concentrated portfolio focused on strategic assets at the smaller end of the market cap spectrum. This means that its performance can diverge markedly from other members of its UK smaller companies peer group. However, as illustrated in Figure 17, SEC has tended to outperform its peer group in both share price and NAV total return terms (three-year NAV performance being the only exception). It is noteworthy that SEC has markedly outperformed over the longer term horizons.

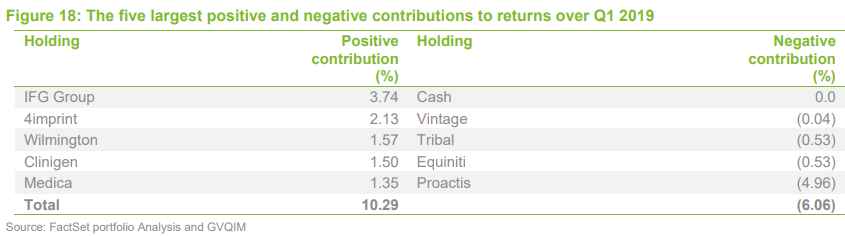

Attribution Q1 2019

IFG Group was the top positive contributor during the quarter. Its full year results were in line with expectations and, as discussed on page 13, it received a cash offer from Epiris at a 46% premium to the share price. 4imprint posted a strong set of full-year results. SEC’s managers say that it is making good progress in its new marketing strategy, which could increase the quality and value of the business over time. Wilmington posted results that were in line with expectations, as did Clinigen. In the case of the latter, SEC’s managers say that its accretive acquisition of Proleukin diversifies the portfolio and provides future growth opportunities. Medica (discussed on pages 14 and 15) posted full-year results that showed strong organic growth, strong cash flow and a fully de-geared balance sheet.

The top negative contributor, by some distance, was Proactis (discussed on page 14). SEC’s managers say that institutional selling has amplified the derating following a profits warning. Equiniti saw a modest fall during the quarter. SEC’s managers say that Equiniti’s full year results showed a strong cash performance, with 7% organic growth. However, its rating remains depressed due to ongoing concerns around the integration of its North American business and cash conversion. SEC’s managers believe it has significant re-rating potential.

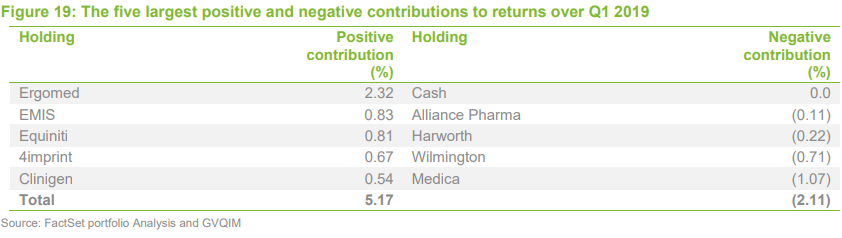

Attribution Q2 2019

Ergomed was the top positive contributor during Q2. It released a positive trading update with upgrades to full year expectations. SEC’s managers say that there has been a strong new CEO hire who, along with the executive chairman has purchased over £850k worth of shares. SEC’s managers say that EMIS and 4imprint delivered in line AGM statements, while Equiniti had a positive AGM statement coupled with the completion of the separation from Wells Fargo.

The top negative contributor was Medica, which SEC’s managers believe de-rated on concerns over the impact of AI on the company’s revenue. It is an area that the Medica is considering. SEC’s managers expect that the adoption of AI will be done over many years and to different extents by the 100+ NHS trusts. They believe that AI will primarily be adopted as a workflow management tool, used to drive efficiency and higher volumes. In the managers’ view, rather than being squeezed by AI, Medica may be uniquely placed to facilitate it.

Subsequent to the end of Q2 2019, Dialight (one of SEC’s holdings that was just outside the top 10 at the end of the quarter) issued a profits warning and the managers have exited the position.

Dividend

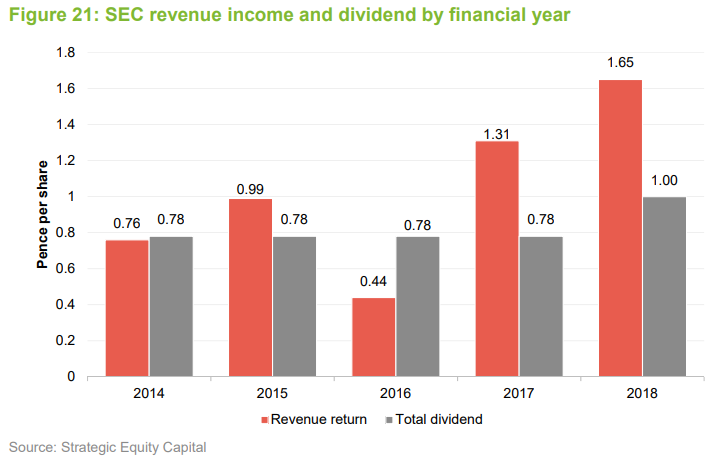

SEC’s investment strategy primarily focuses on generating capital growth for shareholders and dividends are paid to the extent that they are required to maintain SEC’s investment trust status (investment trusts are required to pay out a minimum of 85% of revenue earnings as income to avoid capital gains). As such, dividends are likely to form a small component of shareholders overall returns and SEC pays one dividend in November a year. This is paid as a final dividend, following shareholders’ approval at the AGM (also usually in November). For example, for the year ended 30 June 2018, SEC paid a final dividend of 1.00p per share. This is equivalent to a yield of 0.4% on the trust’s share price of 225.0p per share as at 11 July 2019.

Figure 21 illustrates SEC’s revenue income and total dividend for the last five financial years (ending 30 June). Reflecting strong distributions during the period, SEC’s revenue return saw a 26.0% increase, which the board attributes to the strongly growing profits of SEC’s underlying investments. This allowed for a 28.2% increase in the dividend for the year (from 0.78p per share to 1.00p per share). SEC’s revenue reserve at year end also increased by 51.7% (2.73p as at 30 June 2018 versus 1.80p as at 30 June 2017). After deducting the payment of the increased dividend, SEC had an opening revenue reserve for the current financial year of 1.73p per share, this being 1.73x the prior year dividend, suggesting that it has considerable capacity to smooth dividends in the event there is a revenue shortfall. The board has said that its dividend policy remains unchanged and so the dividend could fall for the current financial year, but it may also be worth noting that when there has been a shortfall in prior years, the board has elected to hold the dividend steady (see Figure 21).

Premium/discount

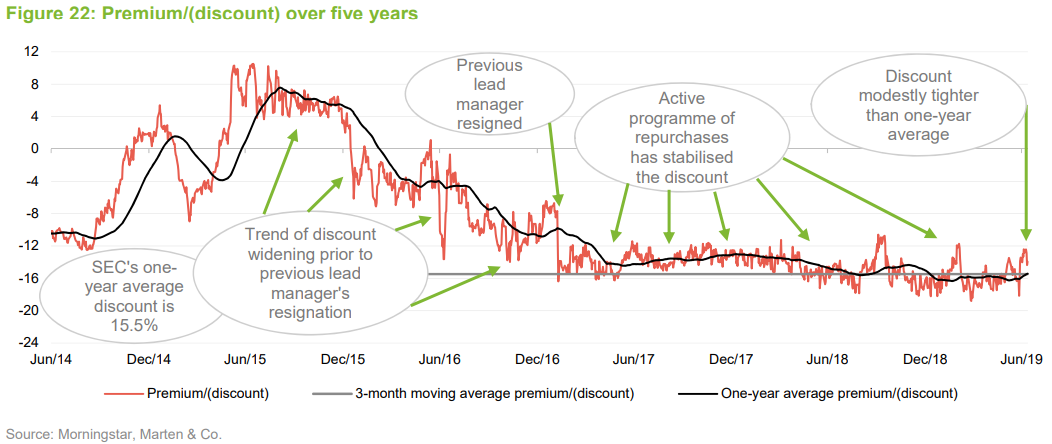

As discussed in QuotedData’s previous notes, SEC’s discount widened over the course of 2016. Having narrowed modestly during the first part of 2017, the resignation of Stuart Widdowson (a former lead manager who worked alongside Jeff Harris) created some uncertainty that saw SEC’s discount move from around 8% to 16.4% on the day of the announcement. However, in part reflecting an active programme of repurchases and investors becoming comfortable with the ongoing management team and investment performance, the discount has since stabilised and has traded in a range of between around 10% and 18% during the last two years. Furthermore, as noted on the front page of this note, despite SEC providing a decent performance under the current management team, the discount has remained stubbornly wide. If SEC’s strong relative performance is maintained, this could potentially drive a sustained narrowing of the discount.

Fees and costs

Under the terms of its investment management agreement with GVQ Investment Management, SEC pays a base annual management fee 0.75% of its net asset value.

GVQIM also gets a performance fee of 10% of the excess return generated where NAV performance is 2% per annum above the FTSE Small Cap ex Investment Companies Index over rolling three-year periods, provided that the index has generated a positive return (otherwise the hurdle is 2% per annum). The maximum payable in any one year, including both the management and performance fee, is 1.4% of the NAV – excess amounts are carried forward to future periods. There is a high watermark.

The management agreement was amended with effect of 1 January 2018 to lower both the base management fee and the performance fee. Previously the base management fee was charged at the lower of 1.0% of market capitalisation or net assets (now 0.75% of NAV), while the performance fee was charged at 15% of the excess return (now 10%).

The contract can be terminated with 12 months’ notice by either party but no notice need be given if the shareholders vote against the continuation of the company.

Company secretarial, administrative and AIFM services

Company secretarial and general administrative services are undertaken by PATAC Limited. Beginning the year ended 30 June 2018, the annual fee is £110,000 per annum and is subject to annual review based on the UK Retail Price Index. GVQIM acts as SEC’s AIFM. The cost of this service is included within the SEC’s base management fee.

Allocation of fees and costs; and ongoing charges

With the exception of the investment managers performance fee, which is charged wholly to capital, all other fees and expenses are charged wholly to revenue.

SEC’s annualised ongoing charges ratio was 1.14% for the year ended 30 June 2018 (2017: 1.25%). For the year ended 30 June 2018, SEC benefitted from having six-months of the management fee charged at the new lower rate. We would expect that, all things being equal, SEC should have a lower ongoing charges ratio for the year ending 30 June 2019, as this will have the full 12 months of management fee charged at the lower rate.

Capital structure and life

Simple capital structure without the use of borrowings

SEC has a simple capital structure with one class of ordinary share in issue. Its ordinary shares have a premium main market listing on the London Stock Exchange and, as at 11 July 2019, there were 69,858,891 in issue with 6,139,302 held in treasury. SEC’s articles permit it to borrow up to 25% of the NAV but GVQIM says it has no intention of gearing the fund and SEC hasn’t had a borrowing facility since July 2012.

Major shareholders

SEC has a simple capital structure with one class of ordinary share in issue. Its ordinary shares have a premium main market listing on the London Stock Exchange and, as at 11 July 2019, there were 69,858,891 in issue with 6,139,302 held in treasury. SEC’s articles permit it to borrow up to 25% of the NAV but GVQIM says it has no intention of gearing the fund and SEC hasn’t had a borrowing facility since July 2012.

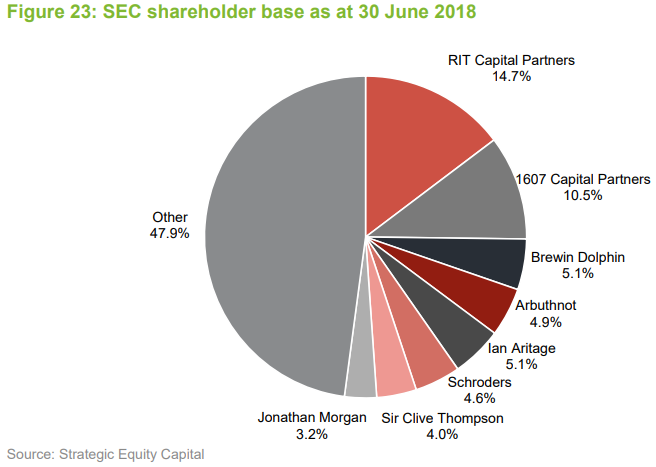

As illustrated in Figure 23, which provides an illustration of SEC’s shareholder base and its largest investors, SEC’s share register has a strong institutional presence, but also has an array of private wealth managers and retail holders. The top 10 largest investors accounted for 63.2% of SEC’s issued share capital as at 30 June 2019.

Financial calendar

SEC’s year-end is 30 June. Its annual results are usually released in October (interims in February) and its AGMs are usually held in November of each year. As discussed on page 18, SEC pays one final dividend in November each year, following shareholder approval at the trust’s AGM.

Management team

GVQIM was founded in 2002. It specialises in using the techniques employed by the private equity industry to invest in quoted companies, and they believe they are one of the leading firms doing this in Europe. The management team does the bulk of its own research, aided by an extensive network of industrialists and private equity professionals. The fund managers have extensive private and public equity experience, and invest in GVQIM’s products. It has been growing in assets under management in recent years (currently in excess of £0.5bn) but the team has ambitions to expand this. In addition to SEC, GVQIM manages the GVQ UK Focus Fund and the GVQ Opportunities Fund.

The team members are:

- Jeff Harris ACA is the lead portfolio manager of SEC. He joined GVQIM in 2012 as a senior analyst. Before that, he was a European banks analyst at Macquarie and performed due diligence on private equity and corporate transactions as a member of the transactions services team at PricewaterhouseCoopers.

- Adam Khanbhai CFA is a fund manager of SEC. He joined GVQIM in 2014 as a senior analyst. Prior to this, he was a consultant at OC&C Strategy Consultants, working on commercial due diligence and strategy products for private equity and corporate clients.

- Oliver Bazin ACA, CFA is a deputy fund manager within GVQIM’s team. He joined in 2016 from Rothschild where he worked in their M&A practice with a focus on financial companies. Previously, he worked in KPMG’s audit practice.

- Rob Ward is a senior analyst within GVQIM’s team. Rob joined GVQIM from Rothschilds, where he worked in corporate finance. Prior to this he worked for Gleacher Shacklock.

- Jamie Seaton and Jonathan Morgan make up the research committee. They vet all new research ideas as well as reviewing existing investments. Jamie is GVQIM’s CEO. Jonathan rejoined GVQIM in October 2016 (having worked at the firm previously, between 2009 and 2014). He was chairman of SVG Capital’s investment committee and worked both at 3i and Prudential’s private equity business for a number of years. He has over 30 years’ experience in private equity.

The Board

SEC’s board is composed of five members (details of their individual experience are provided below and overleaf); all members are non-executive and considered to be independent of the investment manager. It is board policy that all board members retire and offer themselves annually for re-election, and that no Director shall serve beyond the 12th AGM following his or her appointment.

Since QuotedData last published in August 2018, long-standing director and member of GVQIM’s Industry Advisory Panel, Sir Clive Thompson, has retired from the board following the company’s AGM on 7 November 2018. Richard Locke was appointed deputy chairman in his place. David Morrison was appointed to the board with effect of 1 February 2019, maintaining the number of directors at five.

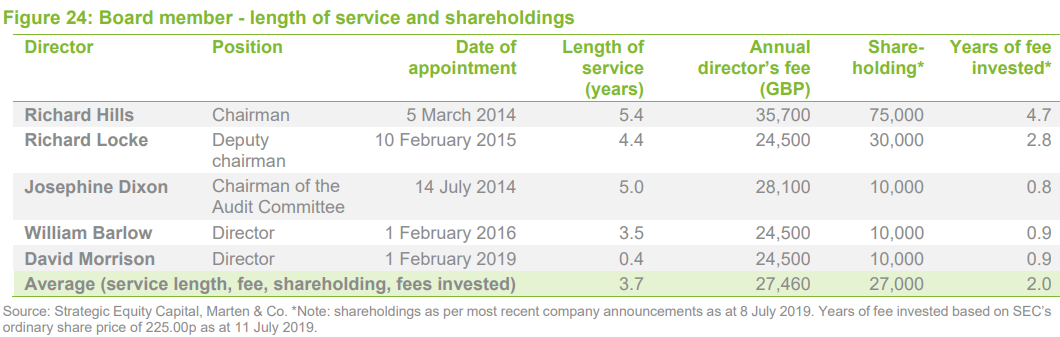

SEC’s directors do not have any other shared directorships and, as illustrated in

Figure 24, the board is relatively young with an average length of service of 3.7 years. All of the directors have made personal investments in the trust and have an average of 2.0 years of fees invested in the trust. This is generally considered to be positive as it shows commitment to the trust and helps to align directors’ interests with those of other shareholders.

Richard Hills (chairman)

Richard has substantial investment company board experience. He is chairman of SQN Structured Finance and is currently on the boards of two other investment companies: JP Morgan Income & Capital and Henderson International Income.

Richard Locke (deputy chairman)

Richard is vice chairman of Fenchurch Partners Limited, an independent corporate finance advisory firm that specialises in the financial services sector. He has been with Fenchurch Partners since 2007, having previously been a partner of Cazenove & Co. and then a director at its successor firm, JPMorgan Cazenove, where he spent 19 years in total.

Josephine Dixon (chairman of the audit committee)

Josephine is a chartered accountant with a career that spans a number of financial and commercial roles in a variety of sectors. She was finance director of Newcastle United between 1995 and 1998 and thereafter served as commercial director, Europe and the Middle East at Serco Group until 2003.

Josephine has substantial investment trust board experience and is currently on the boards of BB Healthcare Trust Plc, F&C Global Smaller Companies Plc, Standard Life Equity Income Trust Plc, JPMorgan European Investment Trust Plc and Ventus VCT Plc.

William Barlow (director)

William is chief executive officer of Majedie Investments, having been a director since 1999. He is a director of Majedie Asset Management and was previously chief operating officer at Javelin Capital. Previously he was an equity portfolio manager at Skandia Asset Management and managing director of DNB Nor Asset Management (UK).

David Morrison (director)

David started his career in investment management at the Industrial Commercial and Finance Corporation (now 3i), before joining Abingworth Management, where he was actively involved in venture capital investment both in the UK and United States. He subsequently spent time at Botts & Co and Blakeney Management, before founding Prospect Investment Management in 1999.

David is currently chairman of Be Heard Group Plc, a marketing services company, and Maris Africa Group, a privately-owned industrial holding company active predominantly in East Africa. He has previously served on the boards of several private and public companies, including PayPoint Plc, Record Plc and Snoozebox Holdings Plc.

Industry Advisory Panel

GVQIM uses an Industry Advisory Panel to inform its research process. GVQIM considers that the panel, which has a broad range of industrial experience, plays a valuable role in that process. All of the current members have been part of the panel since 2014.

Sir Clive Thompson

Sir Clive Thompson is a former director and chairman of SEC (having served as a director between July 2005 and November 2018). Prior to joining the board of SEC, Sir Clive served as Chairman of Rentokil Initial Plc between 2002 and 2004, having been Chief Executive for 20 years to 2002. He is a former President of the CBI, member of the Committee on Corporate Governance and Deputy Chairman of the Financial Reporting Council. He is also a former Director of J Sainsbury Plc, Wellcome Plc, Seeboard Plc, Caradon Plc and BAT Industries Plc. For SEC’s Industry Advisory Panel, Sir Clive advises on business services, consumer services and fast-moving consumer goods companies.

Stewart Binnie

Stewart is formerly Chairman of Aurora Fashions. He is a member of the Investment Committee of the Schroder Private Equity Fund of Funds business, a member of the board of Schroder Ventures Asia Pacific Fund; and has advised Schroders Plc on private equity related issues since 2005. Stewart is also a Former Partner of Permira (formerly Schroder Ventures) and Schroder Finance Partners. He advises on retail, media and technology stocks.

Chris Rickard

Chris is a former CFO of Taylor Wimpey Plc, Whatman Plc, VT Group Plc, Weir Group Plc and Meggitt Plc. Previously he was Head of Corporate Development at Morgan Crucible. He has led numerous successful financial and operational restructurings, as well as executing more than 100 acquisitions, mergers or disposals. Chris advises on industrials, business services and healthcare products.

Peter Williams

Peter was the finance director of Daily Mail and General Trust Plc (DMGT) between 1991 to 2011. DMGT is a worldwide media business, spanning newspapers, online consumer businesses, business information and exhibitions, with a current market capitalisation of around £2.6 billion. Peter is currently a Senior Independent Director of Perform Group Plc, a FTSE 250 digital sports media business. He is also a director of Ibis Media VCT Plc, a small listed VCT that specialises in early stage media investments. Peter specialises in the media sector.

Previous publications

Readers interested in further information about SEC may wish to read our previous notes. You can read the notes by clicking on the links below:

- Different, in a good way – Initiation – 27 January 2015

- Measured expansion on strong performance – Update – 16 July 2015

- Cashing up! – Update – 10 May 2016

- Business as usual – Update – 22 March 2017

- Quality small cap focus – Annual overview – 30 August 2017

- Confident, despite short-term setback – Update – 7 August 2018

The legal bit

Marten & Co (which is authorised and regulated by the Financial Conduct Authority) was paid to produce this note on Strategic Equity Capital Plc.

This note is for information purposes only and is not intended to encourage the reader to deal in the security or securities mentioned within it.

Marten & Co is not authorised to give advice to retail clients. The research does not have regard to the specific investment objectives financial situation and needs of any specific person who may receive it.

The analysts who prepared this note are not constrained from dealing ahead of it but, in practice, and in accordance with our internal code of good conduct, will refrain from doing so for the period from which they first obtained the information necessary to prepare the note until one month after the note’s publication. Nevertheless, they may have an interest in any of the securities mentioned within this note.

This note has been compiled from publicly available information. This note is not directed at any person in any jurisdiction where (by reason of that person’s nationality, residence or otherwise) the publication or availability of this note is prohibited.

Accuracy of Content: Whilst Marten & Co uses reasonable efforts to obtain information from sources which we believe to be reliable and to ensure that the information in this note is up to date and accurate, we make no representation or warranty that the information contained in this note is accurate, reliable or complete. The information contained in this note is provided by Marten & Co for personal use and information purposes generally. You are solely liable for any use you may make of this information. The information is inherently subject to change without notice and may become outdated. You, therefore, should verify any information obtained from this note before you use it.

No Advice: Nothing contained in this note constitutes or should be construed to constitute investment, legal, tax or other advice.

No Representation or Warranty: No representation, warranty or guarantee of any kind, express or implied is given by Marten & Co in respect of any information contained on this note.

Exclusion of Liability: To the fullest extent allowed by law, Marten & Co shall not be liable for any direct or indirect losses, damages, costs or expenses incurred or suffered by you arising out or in connection with the access to, use of or reliance on any information contained on this note. In no circumstance shall Marten & Co and its employees have any liability for consequential or special damages.

Governing Law and Jurisdiction: These terms and conditions and all matters connected with them, are governed by the laws of England and Wales and shall be subject to the exclusive jurisdiction of the English courts. If you access this note from outside the UK, you are responsible for ensuring compliance with any local laws relating to access.

No information contained in this note shall form the basis of, or be relied upon in connection with, any offer or commitment whatsoever in any jurisdiction.

Investment Performance Information: Please remember that past performance is not necessarily a guide to the future and that the value of shares and the income from them can go down as well as up. Exchange rates may also cause the value of underlying overseas investments to go down as well as up. Marten & Co may write on companies that use gearing in a number of forms that can increase volatility and, in some cases, to a complete loss of an investment.