QuotedData’s Real Estate Quarterly Review – Q2 2020

Real Estate Quarterly Roundup

Kindly sponsored by Aberdeen Standard Investments

A polarised lens

A polarised lens

The covid-19 pandemic continued to wreak havoc in the real estate in the second quarter, but a polarisation of sectors and funds has started to become apparent.

Companies focused on the retail, leisure and hospitality property sectors had already seen huge negative rating changes in the first quarter of the year, when the pandemic took hold. This quarter, it was the generalist companies that own a diverse portfolio of UK property that suffered. Most suffered double-digit falls in their share prices in the three months as valuations tumbled on poor rent collection figures.

Those companies with a specialist real estate focus, especially those in the industrial and logistics sector, witnessed big share price gains during the period, with most trading at or above pre-covid levels. A surge in online consumer spending during lockdown created an uptick in demand from occupiers for logistics space, while an acceleration in the long-term trend for ecommerce has put logistics-focused companies at an advantage.

The surge in demand for shares in these trusts saw a number successfully tap the market for equity, with a total of £1.67bn raised in placings.

Performance data

Share price data for the quarter shows that the property sector has been polarised during the covid-19 pandemic. Specialist focused companies in sectors that are set to thrive in a post-coronavirus world have been heavily backed, while the, mainly, generalist companies with diverse portfolios have been indiscriminately, and sometimes unfairly, sold off.

Best performing companies

Perhaps unsurprisingly, four of the 10 best performing companies in the second quarter own property in the industrial and logistics sector, which has seen an uplift in demand for space during the covid-19 pandemic as ecommerce has boomed. Tritax Big Box REIT led the way during the quarter, seeing its share price jump almost 30%. The group announced that it has secured online retail giant Amazon to a 2.3m sq ft pre-let at its development in east London.

Stenprop, which is in the process of transitioning its portfolio to become fully-focused on the UK multi-let industrial sector, saw its share price increase 24.5% in the quarter after publishing strong results in June. Both Warehouse REIT and LondonMetric conducted successful equity raises, of £153m and £120m respectively, as both look to take advantage of buying opportunities.

Sigma Capital Group, the specialist provider of family private rented sector housing, saw its share price rise 27.1% after announcing the appointment of former Countryside Properties chief executive Ian Sutcliffe as chairman.

The share price of RDI REIT, which owns a diverse portfolio of UK property, rose sharply in June after majority investor Redefine sold its near 30% stake to private equity group Starwood Capital – fuelling rumours of a takeover.

Worst performing companies

The worst performing property companies in the second quarter were predominantly made up of generalist companies that have a diverse portfolio, with six of the bottom 10 diversified property companies. Bottom of the pile with a 31.2% fall in its share price, however, was Town Centre Securities, which owns a portfolio of retail, leisure and car park assets. All of the group’s assets have, to some degree, been impacted by lockdown.

Secure Income REIT was majority affected by its largest tenant, Travelodge, implementing a company voluntary arrangement (CVA) in which Secure Income would receive a significant reduction in rental income from the budget hotel brand for the next 18 months. Its share price fell almost 16% in the quarter.

Omitted from the list was Intu Properties, which fell into administration at the end of June having breached several debt covenants. It was trading at 1.7p when its shares were suspended on 26 June. It is unclear whether shareholders will receive anything in the administration process.

Significant rating changes

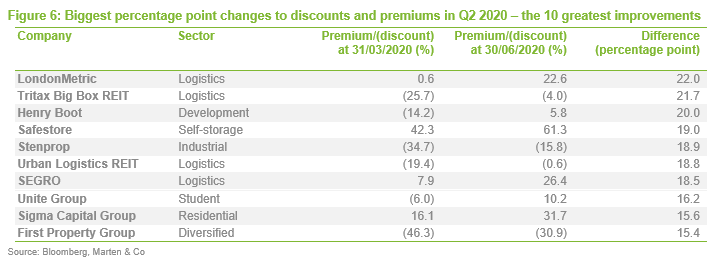

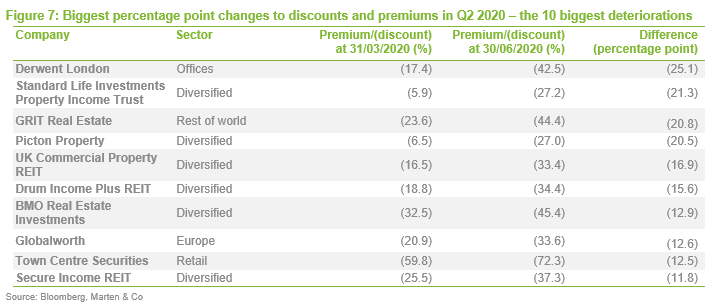

Figures 6 and 7 show how discounts and premiums moved over the course of the quarter.

Once again it was industrial and logistics focused companies that dominated the greatest rating increases during the month. LondonMetric’s went from a slight premium of 0.6% at the start of the quarter to a 22.6% premium as a results of a £120m equity raise at a premium to net asset value (NAV).

Significant equity raises at premium to NAV was also, in part, behind the significant rating changes of SEGRO and student accommodation specialist Unite Group, which raised £680m and £300m respectively.

Tritax Big Box REIT, Stenprop and Urban Logistics REIT all saw their wide discounts narrow substantially during the quarter as positive news flows around the future increased demand for industrial and logistics space caught the imagination of investors.

The biggest rating deteriorations during the quarter has a similar feel to it as the worst performing companies in price terms. However, central London office developer Derwent London saw its discount widen from around 17% at the start of the quarter to more than 40% at the end. Its share price fell 15% in the period as concerns over the future of the office grew.

Many of the other companies on the list reported falling NAVs in the period as property prices tumbled.

Major corporate activity

Fundraises

After a subdued first quarter for equity raises, there was eight separate placings by property companies during the second quarter totalling £1.67bn.

By far the biggest, logistics giant SEGRO raised £680m in June in a share placing “to take advantage of ecommerce trends that are accelerating as a result of the covid-19 pandemic”.

Also in June, student accommodation specialist Unite raised £300m in a placing. The proceeds will be used to “accelerate growth opportunities” in London and prime provincial markets where there is strong demand for the quality, affordable student accommodation.

Warehouse REIT raised £153m in a placing of new shares to fund an acquisition pipeline of logistics assets.

Fellow logistics landlord LondonMetric Property raised £120m in May in an oversubscribed placing. The company said the proceeds would be used to buy properties from an extensive pipeline of opportunities and expects to deploy a substantially amount of the proceeds within three months.

There were four fund raises in April, the largest of which was by Assura Group, which raised £185m. Most of the proceeds, it said, would finance developments. It had a £165m pipeline of projects ahead of the covid-19 pandemic.

Supermarket Income REIT almost doubled its original target of £75m to raise £139.8m in a heavily oversubscribed issue. The company said it had an identified pipeline of acquisitions worth almost £300m and has already invested a significant chunk of the capital.

Self-storage specialist Big Yellow Group raised £81.9m and will use the proceeds to fund the acquisition of land to grow its development pipeline.

Meanwhile, housebuilder Inland Homes raised £9.9m to strengthen its balance sheet amid disruption caused by covid-19. It said the proceeds would help enable an early resumption of its housebuilding programme once the covid-19 restrictions were lifted.

Major trades and appointments

At the end of May, Capital & Counties acquired a 26.3% shareholding in rival West End landlord Shaftesbury for £436m. The group paid 540p per share for 80.7 million shares owned by Hong Kong billionaire Samuel Tak Lee. It represented a discount of 13.9% to the closing Shaftesbury share price on 29 May 2020.

Redefine Properties sold its 29.42% stake in RDI REIT to affiliates controlled by Starwood Capital Group.

Alternative Income REIT appointed M7 Real Estate as its new investment adviser. The company made the appointment after the previous manager, AEW, departed in February. M7, which is a leading specialist in the pan-European, regional, multi-let real estate market, will undertake a review of each of the group’s assets and the company’s investment policy.

Liquidations, de-listings and trading cancellationss

Shopping centre owner Intu Properties called in administrators after last gasp rescue talks with creditors collapsed. The company was in dire straits even before the covid-19 lockdown having built up £4.5bn of debt. It was also facing rent reduction demands from dozens struggling retailers during the coronavirus crisis.

Major news stories

After Intu Properties, the biggest shopping centre owner in the UK, plunged into administration what does it mean for the wider property sector and will other companies follow suit?

• Tritax Big Box REIT pre-lets 2.3m sq ft to Amazon

Tritax Big Box REIT secured a deal with Amazon to pre-let 2.3m sq ft of logistics space at its Littlebrook development in Dartford, east London. The company had just received planning consent for the scheme at the former power station.

• SEGRO acquires urban logistics site for £202.5m

SEGRO bought a 34-acre urban logistics estate in Perivale, west London for £202.5m. The estate provides 590,000 sq ft of lettable space across 23 units as well as eight-acres of medium-term development land.

• LondonMetric splashes £73m with Waitrose store buy

LondonMetric Property acquired five Waitrose supermarkets and an urban logistics facility let to Ocado for a total of £72.9m. It purchased the supermarkets from Waitrose in a sale-and-leaseback deal for £62m and bought the urban logistics unit in Walthamstow for £10.9m.

• Is central London powerhouse REIT on the cards?

Capital & Counties’ acquisition of a huge shareholding in Shaftesbury could be the first steps in a long-mooted merger of the two groups. Combined, Capital & Counties and Shaftesbury own £6.6bn of property in London’s West End.

• Supermarket Income REIT buys stake in Sainsbury’s store portfolio

Supermarket Income REIT acquired a 25.5% stake in a portfolio of 26 Sainsbury’s supermarkets in a joint venture (JV) with British Airways Pension Fund from British Land for £102m.

• Great Portland Estates lands major West End office pre-let

Great Portland Estates secured a 40,000 sq ft pre-let at its office development at 1 Newman Street and 70/88 Oxford Street to Exane BNP Paribas. The deal was a significant boost to the central London office market as fears around a drop off in demand for office space mount amid the coronavirus crisis.

• Hammerson’s £400m sale of retail park portfolio falls out of bed

Hammerson’s £400m deal to sell a portfolio of seven retail parks to Orion European Real Estate Fund V failed to complete. Hammerson will access the £21m deposit, but the news was a hit to its efforts to fix its balance sheet.

• Urban Logistics REIT makes £103m of acquisitions

Urban Logistics REIT bought 17 assets for a total of £103m as it went about spending the proceeds of its £136.1m equity capital raise that completed in March. The company also confirmed that all its rents have been collected for the quarter.

• Helical sells London office at sub-4% yield

Helical sold 90 Bartholomew Close, Barts Square, EC1, for £48.5m and a net initial yield of 3.92%. The sale was a fillip for the property market during a period of few investment transactions due to the covid-19 pandemic.

Upcoming events

QuotedData’s Property Summer Conference, 22 July 2020

Publications

Aberdeen Standard European Logistics Income – Resilient to covid-19, published June 2020

Civitas Social Housing – Proved its mettle, published April 2020

The legal bit

This note was prepared by Marten & Co (which is authorised and regulated by the Financial Conduct Authority).

This note is for information purposes only and is not intended to encourage the reader to deal in the security or securities mentioned within it.

Marten & Co is not authorised to give advice to retail clients. The note does not have regard to the specific investment objectives, financial situation and needs of any specific person who may receive it.

This note has been compiled from publicly available information. This note is not directed at any person in any jurisdiction where (by reason of that person’s nationality, residence or otherwise) the publication or availability of this note is prohibited.

Accuracy of Content: Whilst Marten & Co uses reasonable efforts to obtain information from sources which we believe to be reliable and to ensure that the information in this note is up to date and accurate, we make no representation or warranty that the information contained in this note is accurate, reliable or complete. The information contained in this note is provided by Marten & Co for personal use and information purposes generally. You are solely liable for any use you may make of this information. The information is inherently subject to change without notice and may become outdated. You, therefore, should verify any information obtained from this note before you use it.

No Advice: Nothing contained in this note constitutes or should be construed to constitute investment, legal, tax or other advice.

No Representation or Warranty: No representation, warranty or guarantee of any kind, express or implied is given by Marten & Co in respect of any information contained on this note.

Exclusion of Liability: To the fullest extent allowed by law, Marten & Co shall not be liable for any direct or indirect losses, damages, costs or expenses incurred or suffered by you arising out or in connection with the access to, use of or reliance on any information contained on this note. In no circumstance shall Marten & Co and its employees have any liability for consequential or special damages.

Governing Law and Jurisdiction: These terms and conditions and all matters connected with them, are governed by the laws of England and Wales and shall be subject to the exclusive jurisdiction of the English courts. If you access this note from outside the UK, you are responsible for ensuring compliance with any local laws relating to access.

No information contained in this note shall form the basis of, or be relied upon in connection with, any offer or commitment whatsoever in any jurisdiction.

Investment Performance Information: Please remember that past performance is not necessarily a guide to the future and that the value of shares and the income from them can go down as well as up. Exchange rates may also cause the value of underlying overseas investments to go down as well as up. Marten & Co may write on companies that use gearing in a number of forms that can increase volatility and, in some cases, to a complete loss of an investment.